Bottom Line:

The April CPI report does little to relieve the concern that inflation is under control. Headline inflation rose 0.6% m/m as energy prices continued to climb. And core inflation jumped to 0.4% m/m, driven by housing. Yes, the spike in housing was mechanical, resulting from the government shutdown. But stripping out shelter from core services, we still see sticky inflation that showed signs of continued acceleration. The sticky inflation issue is not just a tariff and energy story – those pressures will make it more challenging to get inflation back to 2.0%. The more immediate problem is how consumers deal with multiple price shocks. Consumer staples including gas, food at home, clothing, and personal care products all rose this month. And we have seen affordability concerns show up in the consumer confidence data, which sit near record lows. The problem is a more meaningful pullback in demand is unlikely without more job losses – put another way, if consumers have jobs they will continue to spend. For now, we will wait for a cleaner report next month. So too will the Fed, who we expect will remain on pause following the strong employment report and this unpersuasive inflation report in April.

There are three core themes that stood out in the April report:

1) As expected, the housing measure popped – this is alarming but entirely mechanical

-

We previously flagged that methodological quirks surrounding the missing data during the US government shutdown could lead to a spike in housing inflation during the April release. Indeed, housing (OER and rent both +0.5% m/m) reported notably higher in April.

-

We expect the spike in housing is a one-off because the methodological quirk will no longer affect the data moving forward. We will get a cleaner read on housing inflation in the May report.

-

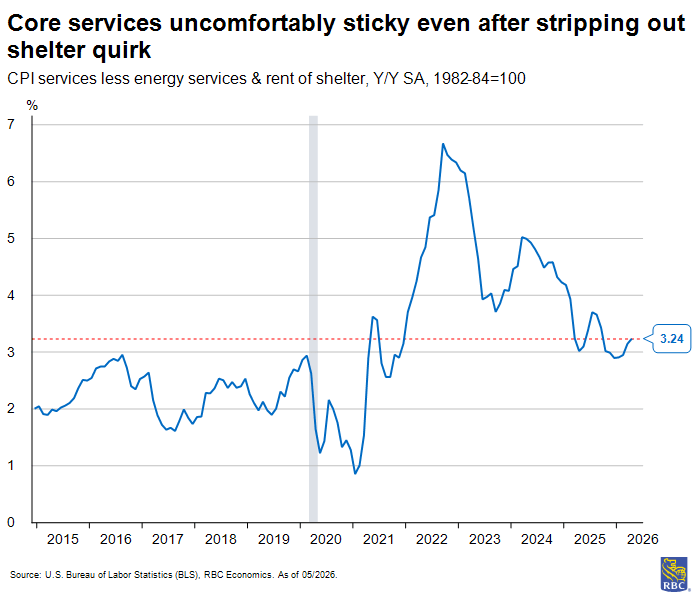

Still, core services excluding housing rose +0.45% m/m with the year-over-year pace of growth rising to 3.3%, up meaningfully from 2.7% pace reported at the start of the year.

2) Tariff pressures are evident in nondiscretionary goods, but motor vehicle deflation continued to mask core goods

-

We continue to see pressures in trade-exposed sectors, notably in nondiscretionary goods. Prices increased over 0.6% m/m in Apparel, IT goods (i.e., cell phones and PCs) and Personal care products.

-

But the motor vehicle sector continued to mask tariff pressures in other areas. Used cars (+0.0% m/m) did not add to overall core goods inflation and new car prices fell -0.2% m/m.

-

Still, the year-over-year pace of growth for core goods was only down 0.1 percentage point in April despite a meaningful reprieve in the largest weighted component of core goods (i.e., new cars).

3) Food and energy prices are weighing on consumers – there is not much that the Fed can do to help

-

Gasoline prices (+5.4% m/m) continued to climb, as the ongoing conflict in the Middle East limits any near-term relief. And higher prices weigh disproportionately on lower and middle-income households.

-

The reality remains that the longer oil prices remain elevated, the more likely it is there will be spillovers to other product groups resulting from rising transportation costs. Higher jet fuel costs resulted in another spike in airfares (+2.8% m/m) in April.

-

While we aren’t expecting to see consumer spending derailed by higher prices, lower and middle-income households will feel the pain of higher prices until these shocks dissipate.

-

We acknowledge that there is little that the Fed can do to address an external shock of higher oil prices, and the same can be said for tariffs. We continue to expect the FOMC will remain on the sidelines throughout the remainder of the year.

About the Authors:

Mike Reid is Head of US Economics at RBC. He is responsible for generating RBC’s U.S. economic outlook, providing commentary on macro indicators, and producing written analysis around the economic backdrop.

Carrie Freestone is a Senior US Economist at RBC. Carrie is responsible for projecting key US indicators including GDP, employment, consumer spending and inflation for the US. She also contributes to commentary surrounding the US economic backdrop which she delivers to clients through publications, presentations, and the media.

Imri Haggin is an US Economist at RBC, where he focuses on thematic research. His prior work has centered on consumer credit dynamics and treasury modeling, with an emphasis on leveraging data to understand behavior.

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. The reader is solely liable for any use of the information contained in this document and Royal Bank of Canada (“RBC”) nor any of its affiliates nor any of their respective directors, officers, employees or agents shall be held responsible for any direct or indirect damages arising from the use of this document by the reader. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.

This document may contain forward-looking statements within the meaning of certain securities laws, which are subject to RBC’s caution regarding forward-looking statements. ESG (including climate) metrics, data and other information contained on this website are or may be based on assumptions, estimates and judgements. For cautionary statements relating to the information on this website, refer to the “Caution regarding forward-looking statements” and the “Important notice regarding this document” sections in our latest climate report or sustainability report, available at: https://www.rbc.com/community-social-impact/reporting-performance/index.html. Except as required by law, none of RBC nor any of its affiliates undertake to update any information in this document.