U.S. President Donald Trump’s refusal to renew the Canada-United States-Mexico (CUSMA) agreement by the July 1st deadline came as no surprise. But it did usher in a new era for the agreement, one that will include more talks—and even more uncertainty.

What does the no deal by the deadline really mean?

-

For starters, the deal is not dead: The agreement will require annual reviews for the next decade. So little changes in the near term, as tariff carve outs for Canadian and Mexican goods that comply with CUSMA remain in place. If, however, the three parties do not reach an extension agreement by 2036, the deal expires.

-

Will the U.S. withdraw before then? Trump has threatened to do so. But he would need to provide six-months written notice—and, according to the U.S. Senate’s finance committee, requires approval from Congress. As our colleagues in RBC Economics pointed out in their latest report, “We continue to view outright termination of CUSMA as unlikely if economic reasoning holds. Exporters/importers on both sides of the border have a strong incentive to maintain the deal.”

-

What about side deals? The U.S. is expected to push for separate “protocols” with Canada and Mexico. Canada-U.S. Trade Minister Dominic LeBlanc said his government is open to this path.

The roadblocks:

The U.S. has a long list of irritants, outlined in the 2026 National Trade Estimate report released by the U.S. Trade Representative (USTR) earlier this year. That includes a few often-cited issues—Canada’s supply management system; a lack of market access for American wine, beer and spirits; and the federal government’s Buy Canadian policy.

But that’s not all:

-

Improved access to Alberta’s power market: The USTR believes there’s been little progress in improving points of access to Alberta’s energy market for Montana energy producers, and that equally priced power generated in Montana is being deprioritized to benefit Alberta power producers.

-

Aircraft regulatory approvals take too long: The U.S. said stakeholders raised concerns about the regulatory process and timelines associated with aircraft validation in Canada.

-

‘Cumbersome’ seed regulations: Canada’s system for importing of seeds, claims the USTR, is “slow and cumbersome and disadvantages U.S. seed and grain exports to Canada.”

-

A lack of IP protection: The USTR put Canada on its Watch List for intellectual property protection and enforcement. It also flagged the poor enforcement of counterfeit or pirated goods at the border and within Canada as a concern, referring specifically to the Pacific Mall in Toronto.

What’s next:

-

Negotiations will continue through the summer: The U.S. is meeting with Mexico the week of July 20 for a third round of bilateral negotiations. Mexico may be willing to make concessions, as Claudia Sheinbaum’s government has made the U.S. its top trade priority. Washington and Ottawa have yet to start negotiations.

-

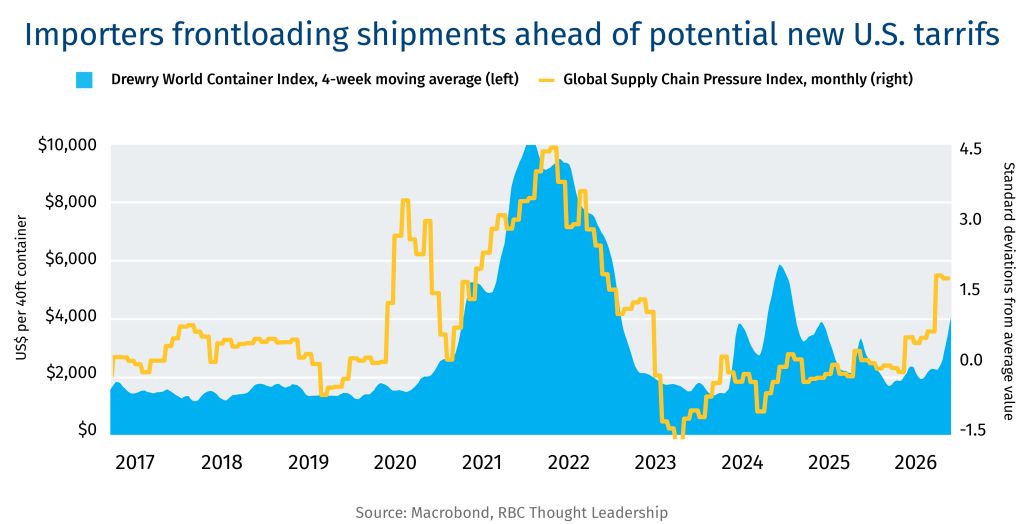

Another deadline looms: Section 122 tariffs will expire on July 24 unless Congress extends them, which is unlikely. It’s expected that the Trump administration will instead introduce a new set of tariffs. That’s already spurred an increase in shipping—and shipping rates—as businesses try to get ahead of a fresh batch of tariffs.

-

Investment uncertainty will dominate: Although the agreement is still in place, the annual reviews will prolong the business uncertainty that is already weighing on investment. Without clarity, businesses are likely to hold off on making critical long-term investment decisions. As Mexico’s economic minister Marcelo Ebrard recently said, “if you drag us into a constant review process, you’re going to choke off investment.”

What if agriculture supply outpaces demand?

The urgency to feed 10 billion people by 2050 has long been a central concern in agri-food research and policy. But with fertility rates down and global populations beginning to stabilize, a new S&P Global Energy study reframes the long-term question for the ag sector: what if supply outpaces demand?

For certain crop commodities, the rate of demand growth is predicted to slow through 2050, with feed crops especially exposed as growth in per capita meat consumption decelerates toward 0.1% annually.

Meanwhile, crop yields and food production continue to increase. That story rings true for Canada, which has boosted its yields and overall production of most crops considerably since the turn of the millennium. For instance, between 2000 and 2012 annual wheat production did not exceed 30 million tonnes, but had reached nearly 40 million in 2025.

| Type of crop | Average annual yield growth (percent), 2000-2025 |

|---|---|

| Canola (rapeseed) | 3.4 |

| Corn for grain | 2.1 |

| Wheat, all types | 3.0 |

| Barley | 3.3 |

Source: Statistics Canada. Table 32-10-0359-01 Estimated areas, yield, production, average farm price and total farm value of principal field crops, in metric and imperial units

If such annual yield increases continue from 2026 to 2050 — and seeded acres remain constant —wheat and canola output would grow by tens of million tonnes.

Although an absolute reduction in food consumption is not expected, when slowing population growth contrasts with continued gains in ag outputs, a gap could pose structural challenges for the export market’s long-term health and profitability. Rising demand for biofuels and alternative markets may take some of that surplus, but Canada will need to continue enhancing its efficiency while working to differentiate itself from other major crop exporting countries. Emphasizing the quality of Canada’s exports and its dependability as a trade partner can help preserve its reputation as a preferred supplier.

Contributors: Alicja Siekierska, Farhad Panahov, Wilson Fink

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. The reader is solely liable for any use of the information contained in this document and Royal Bank of Canada (“RBC”) nor any of its affiliates nor any of their respective directors, officers, employees or agents shall be held responsible for any direct or indirect damages arising from the use of this document by the reader. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.

This document may contain forward-looking statements within the meaning of certain securities laws, which are subject to RBC’s caution regarding forward-looking statements. ESG (including climate) metrics, data and other information contained on this website are or may be based on assumptions, estimates and judgements. For cautionary statements relating to the information on this website, refer to the “Caution regarding forward-looking statements” and the “Important notice regarding this document” sections in our latest climate report or sustainability report, available at: https://www.rbc.com/our-impact/sustainability-reporting/index.html. Except as required by law, none of RBC nor any of its affiliates undertake to update any information in this document.