Also in this edition: 10 numbers that define Brexit’s impact on the U.K. 10 years later

Overheard

Expertise, not electrons, could be Canada’s critical energy export

-

Ottawa’s electricity trade debate keeps circling east-west interties and cross-border electricity flows, but Canadian expertise could be an understated export asset. One such example, called out during Canada’s National Electricity Summit in Ottawa this week, was Manitoba Hydro International (revived in 2024 by the provincial utility following a three-year closure), which started selling Canadian utility expertise to more than 120 clients around the world in 1998.

Canada needs to remove barriers to trade and to investment

-

A big takeaway from a C.D. Howe Institute roundtable this week was that while trade diversification is important, lowering barriers to foreign investment is just as urgent. Holistically reforming the country’s corporate income tax system was one of the ideas that was floated.

What’s the deal with CUSMA?

Next week, North America will cross a threshold in the Canada-U.S.-Mexico trade relationship.

It’s not a cliff, but it will start a new chapter in what has been the world’s most successful trade pact.

To assess what may come next, RBC’s John Stackhouse joined a Brookings Institution virtual roundtable this week, with policy thinkers from all three countries. One thing seemed certain: no matter how a revised CUSMA looks, the spirit of North American trade is likely to bring more elbows and fewer handshakes.

Some other takeaways:

1. There will be a deal: “Reason for optimism” was a refrain, although the costs of that deal will be felt in all three countries. So, too, is timing, especially if negotiations continue after the U.S. mid-terms and into a more fractious Washington.

2. Get used to tariffs: Beyond the July 1 trigger for a CUSMA review, the current regime of Section 122 tariffs will expire on July 24, when we should expect the Trump administration to create another regime. Canadians need to think through a range of tariffs that could follow, from a “heavy hand” option of 15-25% tariffs (unlikely), to a variation of the status quo, which could carry greater border measures on digital trade. A safe bet is some form of “market access” price, perhaps in the 5% range, with plenty of exemptions.

3. Side letters will be key: The general agreement may stay largely in place, with a host of side agreements that don’t require legislation. That can be good news, as such letters can be changed more easily than a full agreement. But that risk can also apply to safeguards that Canada and Mexico may seek in side deals.

4. Mexico is willing to make concessions: Claudia Sheinbaum’s government—more overtly than Canada—has made the U.S. its top trade priority, and is adopting policies to align with Washington’s asks. That could include stricter rules of origin for the auto sector. Mexico is also interested in a broader framework, to address border, energy and food security issues as well as trade.

5. Canada needs to manage internal divisions: There’s no single Canadian economy when it comes to trade. The current 232 tariffs cover 36-37% of Canadian exports to the U.S.—but 58% for Ontario and 55% for Quebec. The Maritimes, Saskatchewan and Alberta face hits of less than 10%. Canadian opinion has also hardened against a deal at any cost, in part because Canadian trust in U.S. commitments has declined.

6. Uncertainty is hurting investment and growth: In all three countries, businesses are hedging the borders, diversifying production to get ahead of new tariff and non-tariff measures. For Canada, there also may be some investments taking place to serve non-U.S. export markets, notably Europe and China.

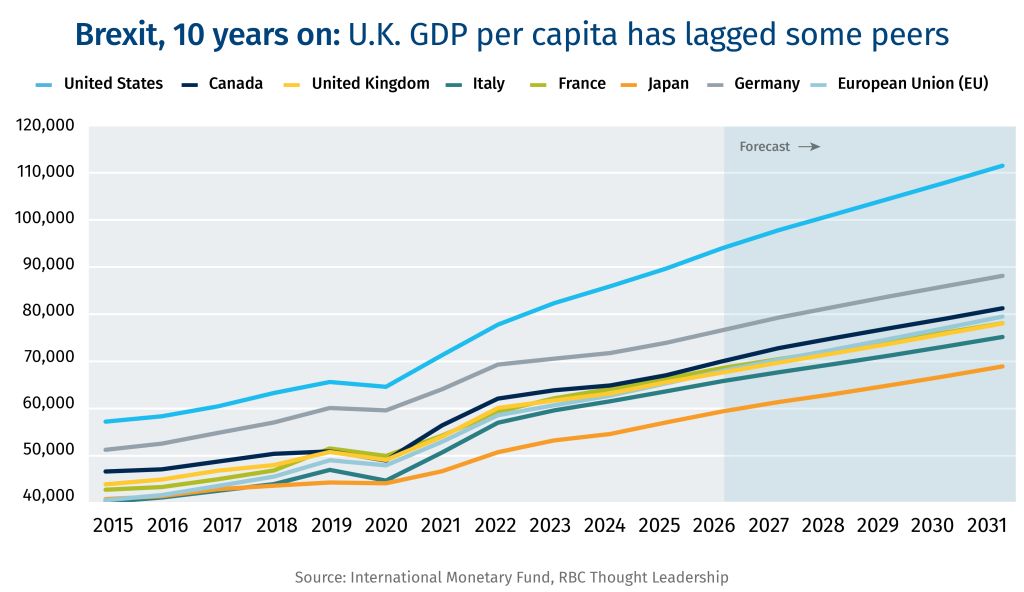

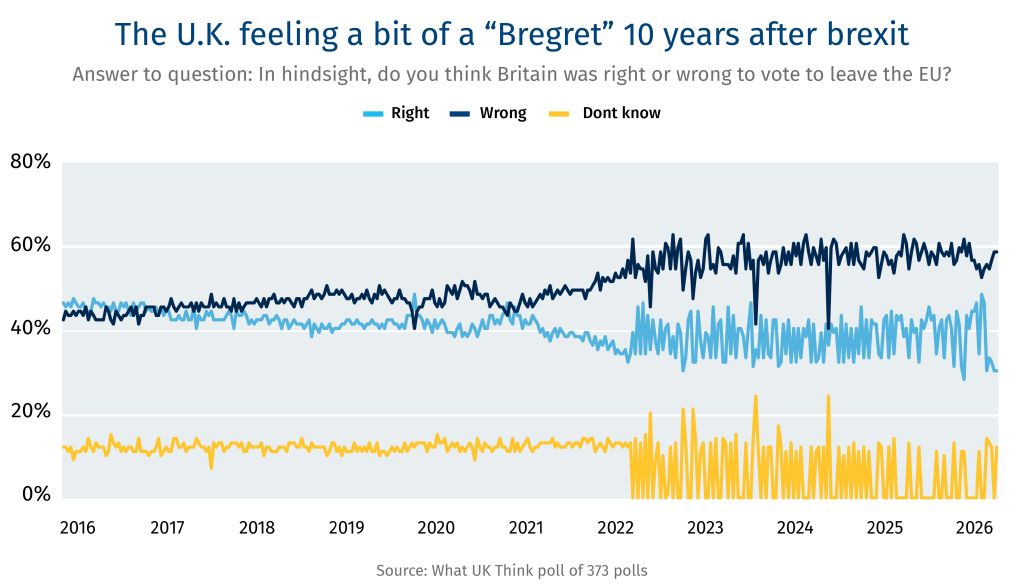

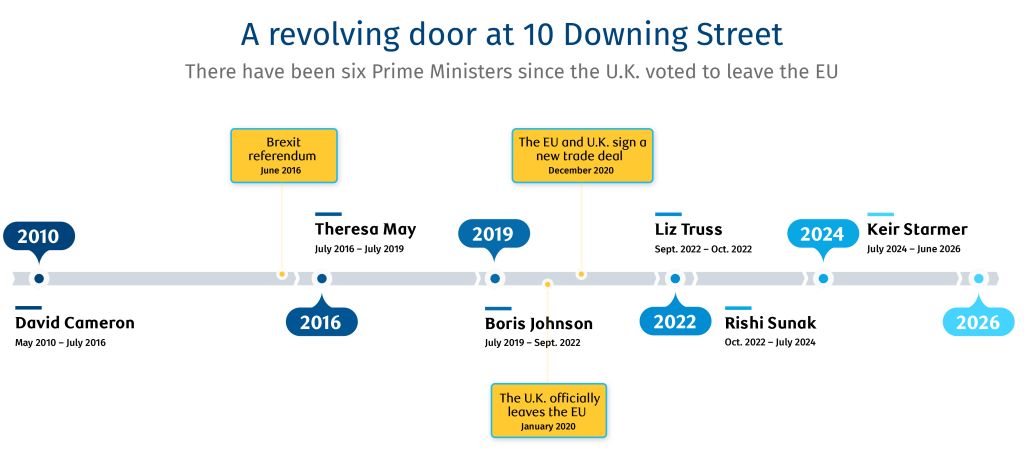

By the numbers: Brexit at 10

This week marked the 10-year anniversary of the referendum that resulted in the United Kingdom leaving the European Union. A decade after the seismic vote, the ramifications are still being calculated and realized.

-

↓ 14% – The decline in U.K.’s exports of goods to the EU in 2025 compared to 2019, before the two partners signed a new trade deal. During the same period, U.K. exports to non-EU countries were down 8%.

-

↑ 28% – The jump in U.K.’s services exports to the EU compared to 2019. Exports to non-EU countries were up 26% from 2019. However, the Centre for European Reform estimates that service exports are still 7% lower than they would have been if the U.K. had stayed in the EU.

-

↓ 6-8% – The decline in the U.K.’s GDP growth by the end of 2025 due to Brexit, according to a study from the National Bureau of Economic Research.

-

↓ 5-10% – The U.K.’s GDP per capita growth was between 5% and 10% less than other similar countries between Brexit and the end of 2025, NBER also estimates.

-

↓ 13% – The decline in the U.K. business investment. Another study suggested U.K. firms invest just 11.1% cent of GDP, with only Canada lower in the G7.

-

16% – The share of businesses reporting that Brexit was an important source of uncertainty as of Sept. 2025. It was as high as 40% shortly after the U.K. left the EU.

-

39 – The number of trade deals Britain has signed covering 72 countries since Brexit. Still, while the U.K.’s trading relationship with the EU fundamentally changed post-Brexit, the bloc remains the U.K’s largest trading partner.

-

57% – Of respondents said Britain was wrong to leave the EU in a recent poll.

-

41% – The EU accounted for 41% of the U.K.’s exports, and 50% of the U.K.’s imports.

-

6 – The number of Prime Ministers the U.K. has had since the referendum. Former Greater Manchester major Andy Burnham is expected to become the seventh PM since Brexit.

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. The reader is solely liable for any use of the information contained in this document and Royal Bank of Canada (“RBC”) nor any of its affiliates nor any of their respective directors, officers, employees or agents shall be held responsible for any direct or indirect damages arising from the use of this document by the reader. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates. This document may contain forward-looking statements within the meaning of certain securities laws, which are subject to RBC’s caution regarding forward-looking statements. ESG (including climate) metrics, data and other information contained on this website are or may be based on assumptions, estimates and judgements. For cautionary statements relating to the information on this website, refer to the “Caution regarding forward-looking statements” and the “Important notice regarding this document” sections in our latest climate report or sustainability report, available at: https://www.rbc.com/our-impact/sustainability-reporting/index.html. Except as required by law, none of RBC nor any of its affiliates undertake to update any information in this document.