Overheard

U.S.-Mexico trade talks have worsened over security issues

-

While talks between the U.S. and Mexico appear to be progressing, impasses have surfaced over security concerns, particularly extraterritorial U.S. operations to combat drug cartels.

Chinese EVs remain a major irritant for the U.S. in trade talks with Canada

-

It was no mistake that Prime Minister Mark Carney used his moment with President Donald Trump at the G7 Summit to explain the cap on the deal. Behind closed doors, a group of American policymakers remain highly concerned about the entry of China into strategic areas of the North American economy.

Government continues to align foreign and trade policies

-

Foreign Minister Anita Anand will take Türkiye’s foreign minister to a nuclear SMR facility in Darlington next week. Another sign that energy is increasingly a pillar of foreign policy.

How energy markets could shape up post-Hormuz

While hostilities between Iran and the U.S. appear to be subsiding, the re-opening of the Strait of Hormuz will continue to shape trade flows in the days, months, and years ahead.

Why it matters—an MoU is signed, but the Strait isn’t solved

The Washington-Tehran memorandum of understanding guarantees toll-free passage for 60 days only, followed by negotiations with Oman to define the future administration of the waterway.

The Red Sea serves as a cautionary tale. In July 2024, a deal was struck with the Houthis, and Bab el-Mandeb Strait traffic—in the Arabian Peninsula—has not returned to early 2024 levels. Reopening of the Hormuz will be a difficult logistical process regardless of when it starts; with more than 500 vessels stranded in the Persian Gulf, mines to clear, and insurers to convince. Peak Hormuz flows may be behind us. “The vase is broken,” said IEA Executive Director Fatih Birol. “Now all actors know that the Strait of Hormuz was closed once and it can be shut down again.”

By the numbers — resilience, and its limits

The oil market proved more resilient than most forecasts. Brent peaked at roughly US$126 per barrel—a significant shock, but far below the US$200 worst-case scenarios circulated at the height of the crisis.

The reason was adaptation, with a parallel logistics system emerging in real time.

-

U.S. crude exports surged to more than 6 million barrels per day (bpd)

-

Dark-tanker transits climbed to roughly 3 million bpd by early June, with cargoes shuttled by ship-to-ship transfer in the Gulf of Oman

-

Alternative Saudi and UAE pipelines absorbed what they could, which was meaningful even though short of pre-crisis Hormuz volumes

-

Kpler estimates more than 90 million barrels of non-Iranian crude and a further 70 million barrels of Iranian crude are now waiting to leave the region—a significant near-term overhang as the Strait reopens.

But even resilience has a limit, and it is grade. Asian refiners, built for heavy sour Middle Eastern crude, spent the quarter force-feeding light sweet American barrels as a stopgap. The Hormuz gap was more around heavy oil and LNG shipments.

The bigger picture—buyers won’t unlearn concentration risk

Concerns are shifting to a near-term supply glut as trapped Gulf barrels flood the market. The IEA expects a significant crude overhang by 2027 if peace holds. Still, a key learning is that oil markets remain remarkably resilient. When the system was under genuine stress, it adapted through shadow infrastructure, bypass routing, and emergency substitution. Some of this was ad-hoc, but some was planned years, if not decades, ago (such as Chinese strategic reserves, and the Saudi East-West pipeline).

These themes were discussed at RBC’s Global Energy, Power and Infrastructure Conference in New York this month, where access to global markets was the biggest topic among Canadian producers and importers—with buyers in Asia, and one in Germany cited as anchors for Canadian LNG projects in both the Atlantic and Pacific basins. Importing nations are chasing supply security and portfolio diversification, with a willingness to sew up new contracts running well ahead of the industry’s willingness to sanction new supply.

Bottom line — a ceasefire changes the headline, not the lesson

Canada, with one proposed cross-border crude pipeline targeting a mid-2027 final investment decision, TMX volumes already moving west, and West Coast LNG coming online, has meaningful volumes in the near to mid-term. The market will watch the Strait, but the next generation of trade will come from future agreements, which could increasingly include Canada.

—Shaz Merwat, Energy Policy Lead

What CUSMA means for food affordability

New research out of Purdue University illustrates the benefits to food prices of the trade deal now known as the United States-Canada-Mexico agreement and the costs if its dismantled. The USMCA Affordability Study: The Effect of North American Trade on U.S. Food Prices aims to quantify the effect of North American free trade agreements on U.S. food prices, and outlines a scenario where NAFTA was not implemented and historical tariff rates remained fixed. It concludes:

-

For every percentage point in reduced tariff rates, there was a cumulative food price reduction of 2.8% over a 10-year period.

-

Food prices were 12% lower by 2014 than they would have been in the no-NAFTA scenario, saving average households at the time approximately US$500 a year.

-

Reversing the trade agreements would unwind those gains. And since U.S. agri-food imports from Canada and Mexico have grown significantly since the studied period, American consumers could be hit with much higher grocery bills at a time when budgets are already strained.

Following the tariff reductions, key U.S. export commodities such as wheat, corn, and beef products did not see a rise in domestic prices that stronger export demand would normally predict. This is suggestive of how interconnected the North American food supply chains have become.

Food affordability is already weighing heavily on household budgets in Canada and the U.S. New tariffs or trade restrictions emerging out of the upcoming negotiations could undo decades of food supply chain integrations and deepen pressure on consumers.

—Wilson Fink, Agriculture Policy Lead

More car trouble

On the hunt for domestic investment, Mélanie Joly was in China this week pressing Chinese automakers to build in Canada, not just sell. Shoring up investment in Canada’s battered auto industry is necessary, but there are multiple crises on the horizon.

Trapped between two auto giants

Canada is in a tight squeeze in CUSMA negotiations. Section 232 tariffs aim to make Canadian assembly too expensive, threatening one of Canada’s largest export industries unless removed. Meanwhile, China eyes Canada as its North American beachhead—BYD already secured quota approval, with Chery and Geely racing for their slice of the 49,000-unit imports.

The dynamics are stark: China wants Canadian consumers, America wants Canadian assembly jobs. Canada’s 125,000-strong auto workforce is caught in the crosshairs.

But here’s what everyone’s missing in this tug-of-war: while Canada struggles to secure its share of North American assembly, rising vehicle prices are pushing more consumers out of the new vehicle market altogether, compressing demand while the global auto industry is facing over-capacity issues.

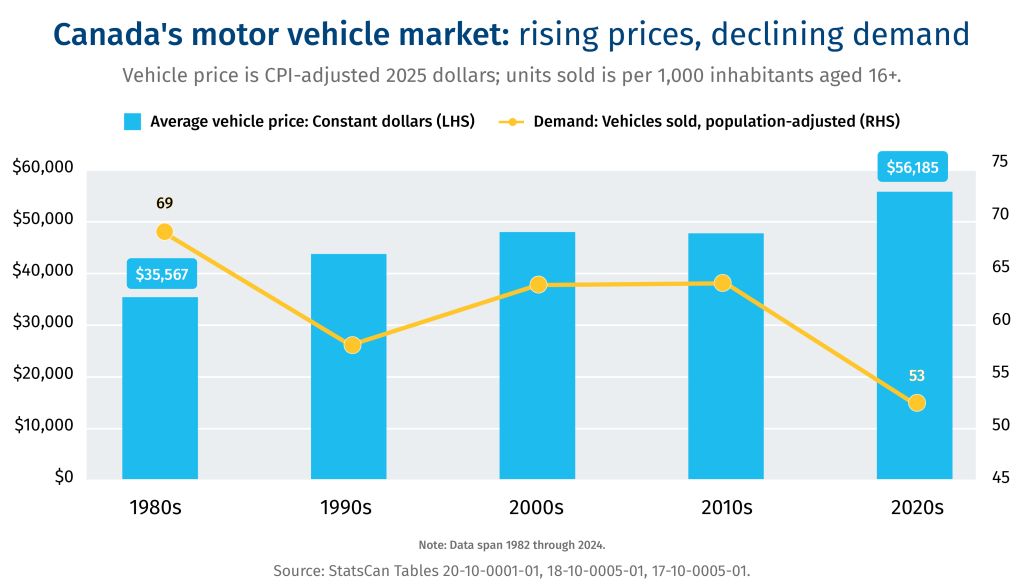

The affordability trap no one’s watching

Vehicle prices have structural headwinds that make tariffs particularly dangerous. SUVs and pickups, which are more expensive than sedans and compact vehicles, already dominate sales. Ever-more tech features also pump up the price tag. When we layer tariffs on vehicles, steel, and aluminum, affordability doesn’t just suffer—it tanks.

The Canadian numbers illustrate the trend: 1.92 million new vehicles sold in 2024, down 160,000 units from 2017 despite 4.3 million more driving-age residents in Canada. Population-adjusted sales have collapsed more than 20% since the 1980s while average vehicle prices have cruised 60% higher after inflation.

The pattern repeats stateside—there are 20 million more Americans today than 10 years ago, but vehicle sales fell from 17.4 million units in 2015 to 16.4 million in 2025. As the price of vehicles rise, buyers will be pushed into the resale market.

Bottom line

Higher prices don’t just hurt consumers—they kill the very jobs these policies aim to protect. Fewer purchases mean reduced demand, worsening oversupply, and ultimately eliminating assembly positions across North America.

(For more on North America’s auto industry, read our latest report: Steering Through Uncertainty)

—Jordan Brennan, Managing Director, RBC Thought Leadership

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. The reader is solely liable for any use of the information contained in this document and Royal Bank of Canada (“RBC”) nor any of its affiliates nor any of their respective directors, officers, employees or agents shall be held responsible for any direct or indirect damages arising from the use of this document by the reader. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.

This document may contain forward-looking statements within the meaning of certain securities laws, which are subject to RBC’s caution regarding forward-looking statements. ESG (including climate) metrics, data and other information contained on this website are or may be based on assumptions, estimates and judgements. For cautionary statements relating to the information on this website, refer to the “Caution regarding forward-looking statements” and the “Important notice regarding this document” sections in our latest climate report or sustainability report, available at: https://www.rbc.com/our-impact/sustainability-reporting/index.html. Except as required by law, none of RBC nor any of its affiliates undertake to update any information in this document.