An emerging crisis

As the Middle East crisis drags on, many oil-importing emerging economies face a “triple squeeze”: rising energy import costs, currency depreciation, and higher rates to reprice debt.

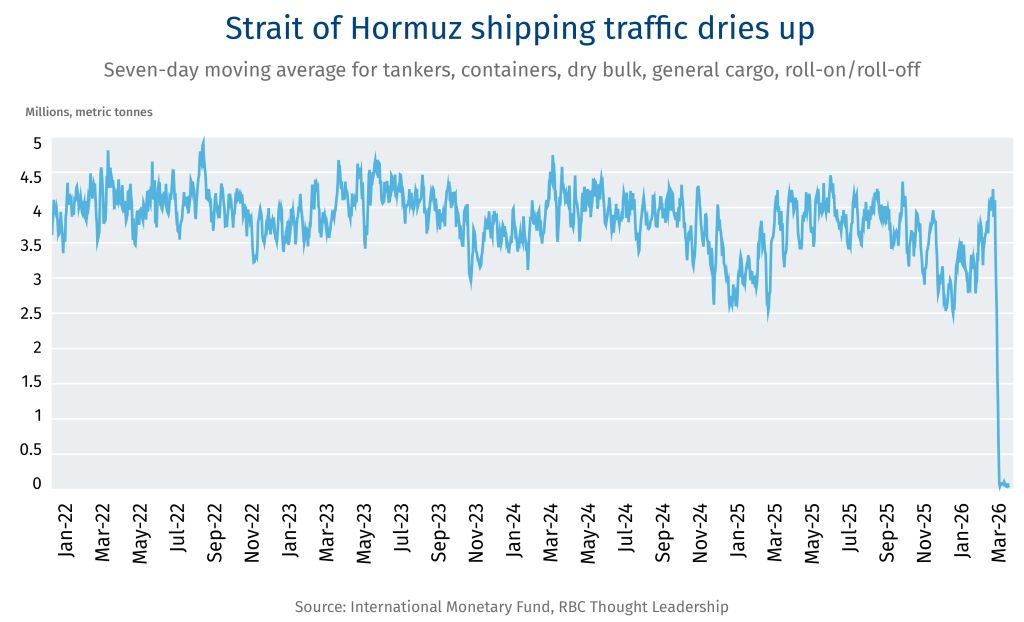

Iran’s virtual blockade of the Strait of Hormuz has sent oil, diesel and gas prices soaring, raising costs for food, fertilizer and transport globally. But it’s developing economies that are bearing the brunt. For several African economies, energy and transport make up 15-25% of the CPI basket, a stronger U.S. dollar (up 0.85% against a basket of currencies since the Iran war began) has raised local currency debt service costs. Countries from Argentina to Vietnam have embarked on energy conserving measures and/or initiated emergency consumer support measures to offer some relief. Energy-driven inflation is pressuring central banks to maintain high interest rates even as domestic economies slow and foreign exchange reserves are drained. Investor confidence has already taken a hit with the MSCI Emerging Market Index wiping out its 13% year-to-date gains, while emerging market bond sales hit their lowest level for March since 2009.

Emerging markets’ debt vulnerabilities were already at historic highs. Developing countries paid US$741 billion more in debt service than received in financing (2022–2024). Borrowing costs have risen materially, with post-2020 issuance coming at rates around 10%, roughly double pre-pandemic levels. With 29% of Low-Income Countries (LIC) bonds maturing by 2026, default risk is rising for some sovereigns. The World Bank says it’s “ready to respond at scale” to assist emerging markets that have reached out.

Here are some of the countries that are under strain:

-

Egypt: Net energy importer with large fuel subsidies (28% of government spending), high USD debt, and near-term Eurobond rollovers US$4 billion); FX pressure (currency −8%) and current account deficit (−3% GDP) compounded by reliance on GCC remittances (73% originate from Gulf economies) and declining Suez/tourism revenues.

-

Pakistan: Petroleum prices are up 25%, as upcoming rollover (US$1 billion) is due 2026; recent debt crisis history, and heavy reliance on GCC remittances (62% of remittances originate from Gulf economies) strain reserves and heighten balance-of-payments risk.

-

Bangladesh: Structurally dependent on LNG (50% of electricity) with no short-term substitutes; supply disruptions and rising transport costs are pushing inflation (~9%+) and increasing FX reserve pressure.

-

Zambia: Extremely high debt service burden (10% of GDP) and fertilizer import dependence (2.5% of GDP); FX depreciation (−5%) compounds external financing stress.

-

Sri Lanka: Post-2022 default economy remains fragile; fuel rationing and continued import dependence constrain recovery despite partial stabilization of LNG supply via the U.S.

-

Côte d’Ivoire, Mongolia, Dominican Republic: Combination of FX-denominated debt exposure, current account deficits, and 2026 maturities; several also carry subsidy burdens (e.g., Mongolia) that amplify fiscal pressure as energy prices rise

-

South Africa: High share of local debt held by non-residents (16% of GDP); FX pressure (currency –5.2%); vulnerable to capital outflows, bond market volatility, and tightening financial conditions.

-

Turkey: Extremely high domestic yields (>35%), persistent currency depreciation, and significant reserve depletion (US$23 billion) from FX intervention; limited policy flexibility.

-

India: crude import dependence is at 89%, roughly half via the Strait; rupee at record lows, fertilizer plants capped at 70% capacity; exposure amplified by reliance on remittances.

-

Philippines: Imports 90% of its oil from the Middle East; current account deficit (−3.4% GDP). Maritime shipping disruptions are compressing margins in its most critical export sector (as semiconductors and electronics account for roughly 60% of total exports), while energy price pass-through is driving inflation above target.

How it impacts Canada

Several of the markets critical to Canada’s diversification strategy are exposed to the war in Iran: Bangladesh and Pakistan are key destinations for Canadian pulses. In Zambia, where copper accounts for roughly 70% of export earnings, Canadian firms are leading major production expansions. Reports of hours-long queues at fuel stations in India signal the shock is already hitting at the household level—and it comes as the Canada-India Comprehensive Economic Partnership Agreement (CEPA) negotiations target $70 billion in two-way trade by 2030. Meanwhile, Canadian entities’ exposure to emerging market assets across South America, Africa and Asia, could also present another challenge.

— Sydney Wisener

The week that was

World Trade Organization (WTO) reform talks derailed

-

The WTO’s 14th Ministerial Conference, held in Cameroon last week, failed to usher in a new era of global trade reform after the U.S. and Brazil sharply diverged over how long to extend the E-Commerce Moratorium, an agreement that prohibits levies being placed on electronic transmissions and digital services.

-

The disagreement was the primary reason why a draft plan for reform of the WTO was not adopted, a major setback for the organization as it looked for ways to fight back against its marginalization and remain relevant in this new era of trade disruption.

-

U.S. Trade Representative Jamieson Greer slammed the WTO upon his return to the U.S., saying it would only play a “limited role” in future global trade policy discussions.

Helium emerges as another Hormuz headache

-

As well as disrupting global energy, aluminum, shipping, and fertilizer markets, the quasi-closure of the strait threatens the global supply of helium, a key component in the production of semiconductors.

-

Since helium is primarily a by-product of LNG production, LNG supply chokes threaten to also disrupt the flow of the gas, of which a third of global supply passes through Hormuz. Helium prices have roughly doubled since the war began according to Fitch Ratings, which could have knock-on effects for technology-heavy economies, such as South Korea, Japan, and even the United States tech sector.

-

Tungsten and sulfur are also key components of the global semiconductor supply chain and have experienced sharp price increases. Prior to the war beginning on February 28th, China had restricted its tungsten exports and called for tighter limits on sulfuric acid exports.

The U.S. announces new tariffs on pharmaceuticals

-

Donald Trump announced new levies on branded drugs from pharmaceutical companies, including 100% tariffs on patented medications and their active ingredients.

-

This follows through on the threats Trump made last fall as part of his administrations drive to pressure pharmaceutical manufacturers to build or onshore production facilities to the U.S.

-

Reduced rates of 15% will be offered to jurisdictions that have secured trade deals with Washington, including Switzerland, Japan, the EU and South Korea. A U.S. official said the UK will essentially have zero tariffs on its imports as major British companies have struck deals with the administration.

— Thomas Ashcroft

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. The reader is solely liable for any use of the information contained in this document and Royal Bank of Canada (“RBC”) nor any of its affiliates nor any of their respective directors, officers, employees or agents shall be held responsible for any direct or indirect damages arising from the use of this document by the reader. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.

This document may contain forward-looking statements within the meaning of certain securities laws, which are subject to RBC’s caution regarding forward-looking statements. ESG (including climate) metrics, data and other information contained on this website are or may be based on assumptions, estimates and judgements. For cautionary statements relating to the information on this website, refer to the “Caution regarding forward-looking statements” and the “Important notice regarding this document” sections in our latest climate report or sustainability report, available at: https://www.rbc.com/our-impact/sustainability-reporting/index.html. Except as required by law, none of RBC nor any of its affiliates undertake to update any information in this document.