U.S. President Donald Trump finally dropped the hammer on the auto sector with tariffs on automobile and parts imports, upending the global auto industry and threatening economic damage on major suppliers to the U.S. market. The headline 25% U.S. levy has dominated the news but, as we discuss, the true cost of tariffs will be in the details. With countries from Canada to Germany to Japan roiled by the announcements, the industry is grappling with the following questions:

1. How will the tariffs be applied?

-

The proclamation is light on detail on targeted automobiles and automobile parts. Engines and engine parts, transmission and powertrain parts, and electronic components were singled out in a 2019 investigation into the impacts of automotive imports on U.S. national security.

-

But industry remains uncertain about the extent of tariff applicability this time around. The proclamation also allows the U.S. Secretary of Commerce and domestic producers of automobiles or auto parts to request parts not already included to be tariffed in the future.

-

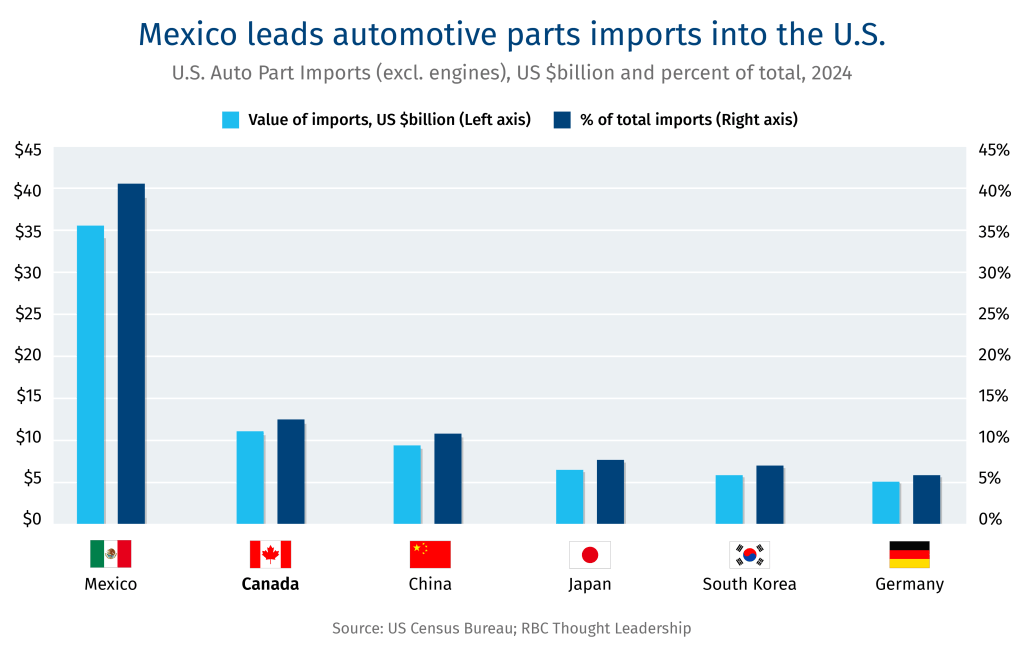

The U.S. imported US$83 billion in auto parts and accessories (not including engines) in 2024, with Mexico and Canada supplying 41% ($35 billion) and 13% (US$11 billion), respectively.

2. How will tariffs be implemented and compliance determined?

-

The true cost of tariffs will depend on the amount of U.S.-origin content in imported vehicles, but specifics remains unclear.

-

According to the president’s order, the 25% tariff will apply to the value of non-U.S. content in imported vehicles. However, discussions between the U.S. and Canada suggest CUSMA-compliant automobile imports with at least 50% U.S. content may be exempt. Those with less than 50% U.S. content may receive 12.5% tariffs.

-

Automotive parts will see tariffs of 25% applied to the value of non-U.S. content, according to a process being determined by U.S. Customs and Border Protection and the U.S. Secretary of Commerce. They are expected to come into force by May 3.

3. How will supply chains be affected?

-

The co-development of U.S., Canadian, and Mexican automotive industries have enabled efficiencies of production and market growth across the continent, from the Automotive Products Trade Agreement in 1965 (also known as the Canada-U.S. Auto Pact) through the integration of Mexico via NAFTA in 1994, and more recent renegotiations of Regional Content Values (RCV) under CUSMA.

-

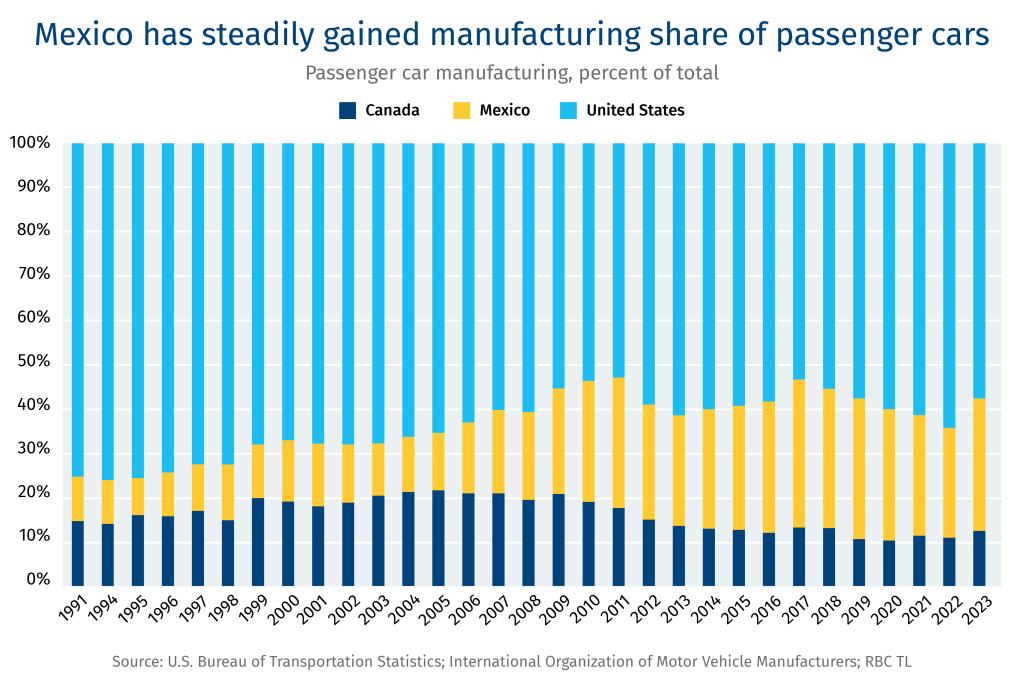

Over the past three decades, Mexico has steadily gained on the U.S. in production share of passenger vehicles in North America, rising from 10% pre-NAFTA in 1991, to 30% of passenger car manufacturing within the continent by 2023. Over the same period, the U.S.’s share of passenger car manufacturing dropped from 75% to 58%. Mexico surpassed Canada’s production share within the continent in 2008.

-

Though Canada’s share of passenger vehicle manufacturing grew from 15% in 1991 to peak at about 22% by 2005, it had dropped to 12% by 2023.

-

A similar trend has emerged in motor vehicle parts. From supplying 9% of U.S. imports in 1990, Mexico has grown to 41% of automotive parts imports in 2024, while Canada’s contribution has reduced to 13% in 2024 from a 1990 peak of 36%.

-

Data on the geographic origins of components across 315 car models available to the U.S. public between 2021-2025, show that, combined, U.S. and Canadian auto parts make up as much as 77% of the total value of certain models, with Mexican origin parts reaching as much as 80% in others.

-

Such high levels of integration means tariff-driven disruptions to automotive supply chains have a high likelihood of rippling through the industry, raising costs and putting pressure on manufacturers, distributors, and consumers across all geographies.

4. What’s the way forward?

-

The precise nature of tariff applicability, compliance, and enforcement remains largely uncertain, leaving manufacturers with few clear options on the way forward.

-

What’s certain is that impacts will be felt on both sides of the border, with 35 U.S. districts across 26 states importing auto parts from Canada in 2024, and southern Ontario’s automotive sector among the hardest hit.

-

The severity of reciprocal tariffs would dictate the added burdens on auto and parts manufacturers. Canada’s response to the U.S. auto tariffs would also determine the future of RCV-based tariff exemption thresholds.

Vivan Sorab is Senior Manager, Clean Technology, RBC Climate Action Institute

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.