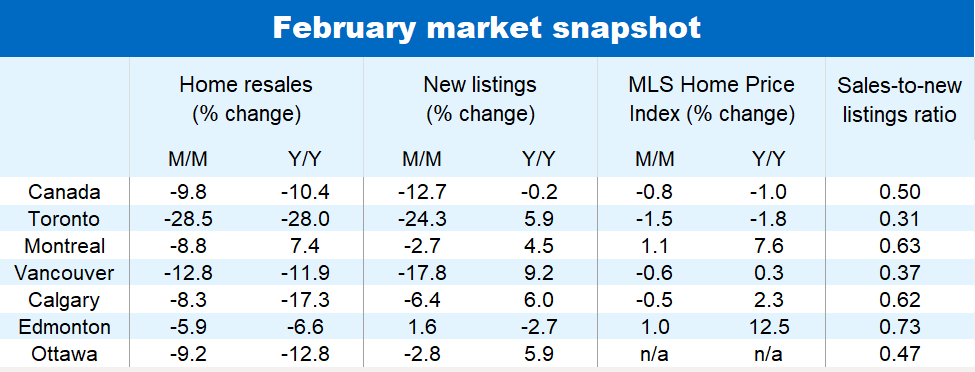

The threat of U.S. tariffs has become top of mind for those considering buying or selling a home in Canada. Concerns about the significant damage that hefty tariffs would inflict on the economy prompted many buyers and sellers to hit pause in February—leading to a nearly 10% plunge in home resales nationwide from January. It was the biggest monthly drop in close to three years.

Sellers’ hesitation sent new listings plunging 12.7%—entirely reversing January’s surge. Still, the number of homes for sale (active listings) continues to rise across most of the country.

Ontario, B.C. markets lead declines

The pullback in demand last month was concentrated in Ontario and British Columbia, where affordability challenges are more acute. Home resales plummeted -29% from January in the Greater Toronto Area, -20% in Hamilton, -17% in the Niagara region and -15% in Kitchener-Waterloo. A series of severe snowstorms in southern Ontario also made house hunting more difficult.

The Fraser Valley (-14%), Greater Vancouver (-13%) and Victoria (-5.7%) recorded third straight monthly resale declines in February.

Market activity has slumped to a new cycle low in Ontario, and isn’t far from one in B.C.

Soft demand and rising inventories are weighing on home prices. Canada’s composite MLS Home Price Index slipped for the second consecutive month in February, easing 0.8% from January and 1% from a year ago.

Again, Ontario and B.C. account for most of the erosion in property values. Ontario’s MLS HPI fell 1.3% sequentially last month (including a 1.5% drop in Toronto), and B.C.’s index edged 0.5% lower (including a 0.6% decline in Vancouver). We expect downward price pressure to persist in these regions in the near term.

Prairies and pockets out east remain vibrant

However, the picture is relatively resilient in other parts of Canada. It’s quite robust in Saskatchewan, where resales remain far above pre-pandemic levels (rising further in February), supply-demand conditions are very tight with inventories still falling, and prices are trending higher.

The market situation is also still broadly solid in Alberta, though Calgary has shown signs of cooling lately, which has considerably slowed down the annual rate of price increases. Edmonton remains one of the hotter markets in country.

There are signs of resilience east of Ontario as well, though its sparser. Quebec City, Sherbrooke and St. John’s maintain substantial sales and price momentum in early 2025. But the strong recovery in Montreal hit a bump in February (with resales down almost 9% from January), while Halifax, Saint John, Fredericton and Moncton are on winding uneven paths.

We expect buyers and sellers to stay cautious in the months ahead across Canada. The trade war launched by the U.S. in March threatens to further erode market confidence, upend buyers’ plans and quiet a usually busy spring season. The impact would intensify the longer trade uncertainty rages.

Robert Hogue is the Assistant Chief Economist responsible for providing analysis and forecasts on the Canadian housing market and provincial economies.

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. The reader is solely liable for any use of the information contained in this document and Royal Bank of Canada (“RBC”) nor any of its affiliates nor any of their respective directors, officers, employees or agents shall be held responsible for any direct or indirect damages arising from the use of this document by the reader. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.

This document may contain forward-looking statements within the meaning of certain securities laws, which are subject to RBC’s caution regarding forward-looking statements. ESG (including climate) metrics, data and other information contained on this website are or may be based on assumptions, estimates and judgements. For cautionary statements relating to the information on this website, refer to the “Caution regarding forward-looking statements” and the “Important notice regarding this document” sections in our latest climate report or sustainability report, available at: https://www.rbc.com/community-social-impact/reporting-performance/index.html. Except as required by law, none of RBC nor any of its affiliates undertake to update any information in this document.