Key findings

Industrial carbon pricing is seen as one of the most effective policy levers in reducing GHG emissions. Canada is reassessing its approach to scale investment in domestic climate action and put the country back on track for GHG emissions reductions. But all abatement options need to be on the table. Agriculture’s role as a vehicle to reduce GHG emissions and sequester carbon could prove to be a valuable tool in a nationally harmonized carbon market.

Climate-smart agriculture remains an unleveraged resource for Canada to attract investments and GHG emissions reduction. Agriculture could abate more than 37 megatonnes per year in GHG emissions by 2030—that’s about 6% of Canada’s projected GHG emissions in 2030.

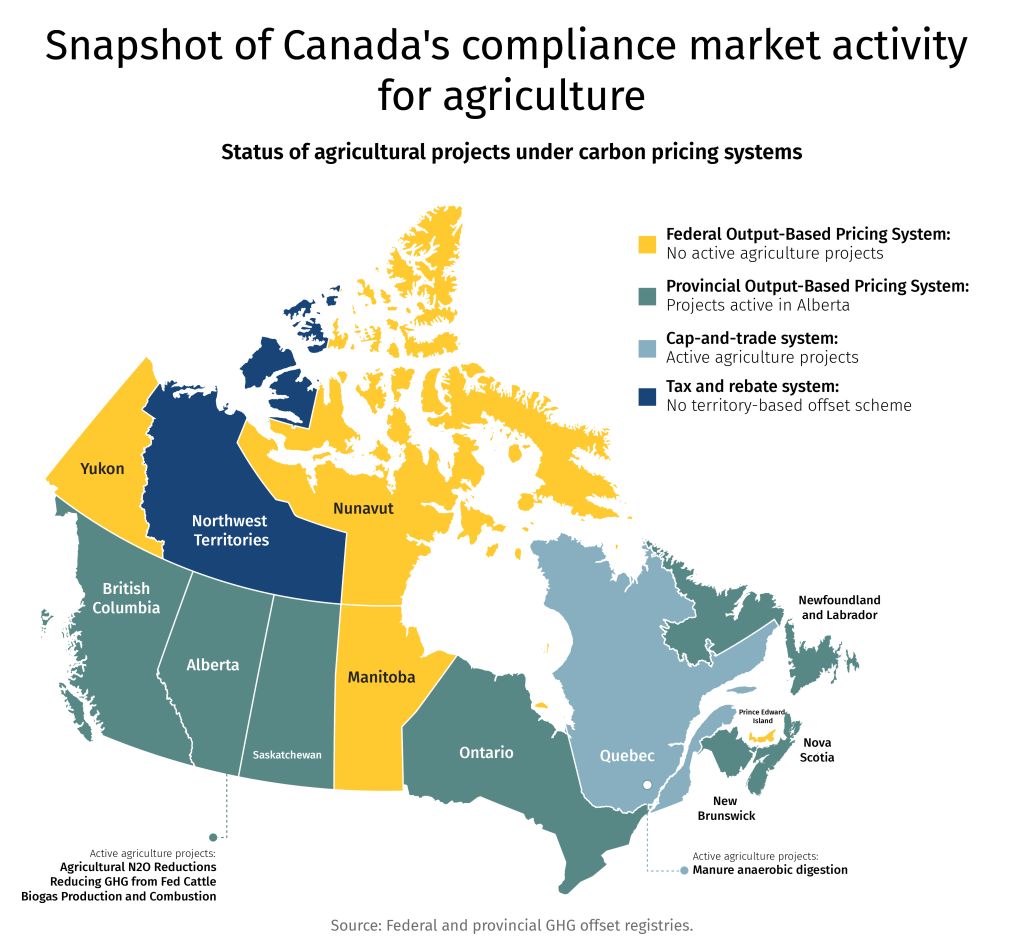

Ten carbon pricing systems make up Canada’s fragmented market. This approach is characterized by poor conditions like supply and demand discrepancies, price inconsistency, and a lack of transparency. Solving these macro issues is essential to making Canadian agriculture and other sectors competitive in climate action.

Agriculture is often sidelined in climate policy, with five major barriers holding back its development. In addition to fragmented, shallow markets, a lack of applicable protocols for climate-smart agricultural practices, high MMRV costs spread across small projects, limited risk mitigation for farmers and investors, and a small pool of carbon market expertise have stunted the growth of Canadian agriculture in the marketplace.

A transfer portal for agriculture projects from offset to inset markets is among five ideas to unlock agriculture’s potential in carbon pricing. Removing federal and inter-provincial regulatory barriersto develop and trade carbon creditsandaccelerating the approval of applicable agriculture protocols through a hierarchy system could also foster a marketplace that benefits from robust agriculture presence.

Agriculture has long been on the sidelines of Canada’s industrial carbon pricing system. But momentum may be shifting. The climate competitiveness strategy, industrial carbon pricing benchmark review, Canada-Alberta energy MoU, and a new nature strategy (A Force of Nature), are all potential launchpads to more deeply engage agriculture in climate innovation and nature-based investment opportunities like carbon markets.

Farmers have advocated for improved access to carbon markets as a source of offsets for some time.1 While climate-smart agriculture can create win-wins in profit margins and greenhouse gas (GHG) mitigation, innovation can be expensive at first—making incentives essential to scaling impact. On the surface, the financial opportunity of carbon markets for farmers innovating in climate-smart practices and technology is immense. Market participation can also help chip away at the sector’s GHG emissions and boost its carbon sinks. Canada’s agriculture sector produces 10% of Canada’s emissions and could abate more than 37 megatonnes of GHG emissions per year by 2030 by adopting climate-smart practices—that’s about 6% of Canada’s projected GHG emissions in 2030.2 With the right carbon market in place, that GHG abatement potential could be turned into assets for investors and companies looking to reduce their carbon footprint.

But for all its promise, Canada’s current carbon pricing regime is fragmented, characterized by underperforming markets, and unleveraged investment opportunities.Limited progress in building a fungible marketplace and utilizing agricultural landscapes and technologies as offsets in Canada has diverted climate-smart investments and projects to other countries. That said, scaling agriculture’s presence in carbon markets is still early days and remains a complex policy endeavor in most advanced economies. There’s still time for Canada to ramp up. And while structural, capital and talent barriers weaken the agriculture sector’s ability to issue offset credits at scale, addressing these issues is an opportunity to durably position agriculture GHG mitigation as a cost-effective path for Canada to meet its net-zero goals. Doing so, as is outlined below, requires targeted policy reform, accelerated action on protocols, and precise investment in capacity and resourcing.

That said, scaling agriculture’s presence in carbon markets is still in its early days and remains a complex policy endeavor in most advanced economies. And while structural, capital and talent barriers weaken the Canadian agriculture sector’s ability to issue offset credits at scale, addressing these issues is an opportunity to durably position agriculture GHG mitigation as a cost-effective path for Canada to meet its net-zero goals. Doing so, as is outlined below, requires targeted policy reform, accelerated action on protocols, and precise investment in capacity and resourcing.

Five factors stunting agriculture’s role in industrial carbon pricing

1. Fragmented federation: Shallow markets prevent scale

Fragmentation discourages investors from looking at Canada as a united market. Canada’s decentralized carbon pricing system poses several challenges with respect to scaling agriculture offsets for investment, including:

-

Policy complexity and ambiguity for farmers seeking market access points

-

High administrative burdens for regulated businesses, aggregators and investors that operate or need scale across jurisdictions to prove return on investment

-

Small markets that lack investor participation and liquidity

-

Ineffective use of Canada’s resources and expertise in market design and development

Further complicating matters, Canada’s system sits within an international voluntary and compliance market landscape that is disjointed. This landscape is difficult to navigate because of the varying offset registries, standards and protocols that are not equal, creating market and credit quality ambiguity.

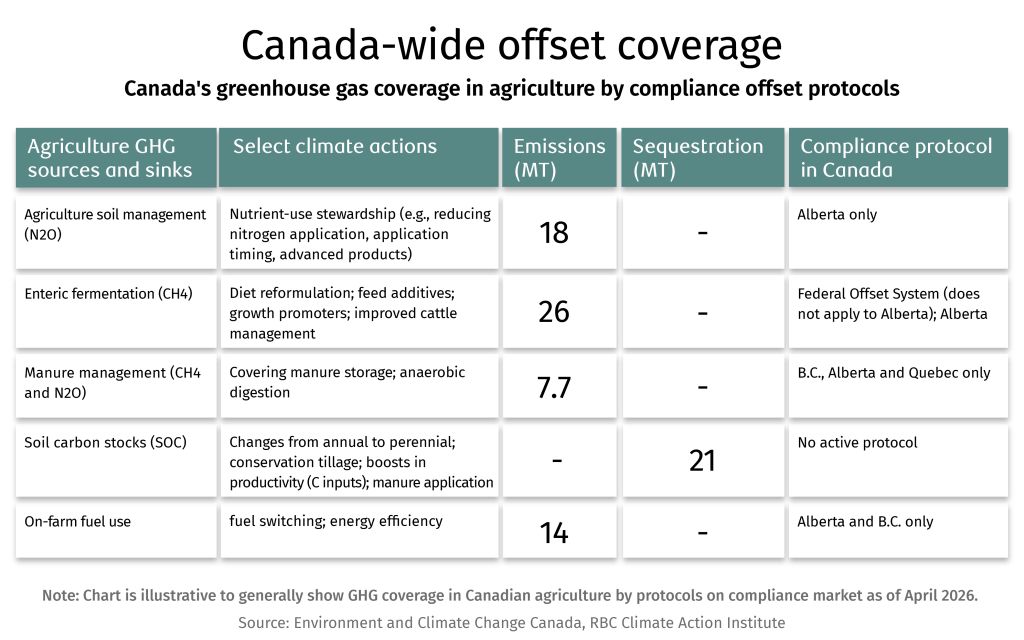

Fragmentation within Canada leads to several inefficiencies in the marketplace. In particular, the limitations in cross jurisdiction protocol use and project development restrain the effective use of domestic resources and expertise. Developing agricultural protocols and offset projects requires significant technical expertise and time to build measuring, monitoring, reporting, and verification (MMRV) standards and systems. When protocols are not transferable, and projects are not scaled across jurisdictions, it can lead to duplication of resource use and impede economies of scale in project development. For example, Environment and Climate Change (ECCC) recently developed a protocol in the federal offset system for emissions reductions in beef feedlots. Federal system protocols are not transferable to provincial systems when an equivalent protocol already exists. Alberta beef producers, who account for more than 70% of Canada’s feedlot cattle, cannot tap the federal protocol despite their suitability and must use the protocol on the Alberta TIER system–resulting in a new protocol that is not accessible by the majority of beef feedlots.

2. Impractical protocols: Agriculture’s role in GHG reductions is limited

One of the biggest obstacles in strengthening agriculture’s presence on compliance markets is the lack of approved and applicable protocols for climate-smart practices. Developers cannot issue credits without protocols that track and verify emission reductions. Without protocols, there are no offsets.

Developing protocols is a highly technical process and building consensus on MMRV approaches is a global challenge. However, agriculture protocols in Canada have proven to be especially challenging—recent protocols are the product of a slow, risk-averse approach. For instance, the Enrichment Soil Organic Carbon Protocol has been under development on the federal system for more than three years as the technical team works to devise a protocol that adheres to the offset system’s standards and is useable in practice.

In Canada, there is a focus on project-specific direct measurements to prove impacts. This often entails greater accuracy but can result in high costs and resourcing for MMRV, especially if projects are not scaled. Balancing rigor with MMRV feasibility is the key challenge in protocol design moving forward. Project developers that have piloted different versions of the Nitrous Oxide Emissions Protocol (NERP) on Alberta’s TIER system have brought this challenge into focus. NERP projects have demonstrated the mismatch that can occur between MMRV requirements, quality in farm-level data, and the realities of working farms in natural ecosystems.

3. Stuck in pilot phase: Small projects, small ROI, slow growth

Building an engaged network of farmers, project developers and policy makers requires piloting programs to build expertise and hubs of innovation. The problem is that many agricultural offset projects in Canada have struggled to get past the pilot phase. As a result, Canada has a small presence in the marketplace–accounting for 0.2% of agriculture projects on established global voluntary registries. These projects have not issued credits yet.3

Several other factors are to blame for the lack of scaled agriculture offset projects on voluntary and compliance markets, including protocol design, limited awareness in Canada on reputable carbon market options for agriculture, small pools of upfront capital for scaling projects, geographical dispersion, and few agri-tech and agri-food companies headquartered in Canada, which can influence where companies plan their first pilot projects and initial growth. The trialing of the Canadian Grasslands Protocol on the voluntary registry, Carbon Action Reserve, also demonstrates the challenges to scaling projects when the value of credits is not in step with the size of commitment asked of farmers and ranchers like signing conservation agreements or easements and 100-year permanence guarantees.

Experience in the voluntary market can be a test bed for farmers, aggregators and regulators that need case studies like the pilot of the Canadian Grasslands Protocol to work out technical kinks and inform future market participation and protocol development. But it requires regulators to action the lessons learned. Proving out the scalability of agriculture offsets and exploring market design components before introducing them into compliance systems is an approach that is being led by the European Union (EU), where the largest Emissions Trading Scheme (ETS) by value is operated. The European Commission has been pressed to include carbon removals, including agriculture offsets, into the EU ETS. The commission is responding to the demand by first exploring impacts in voluntary marketplaces. The EU adopted the Carbon Removals and Carbon Farming Regulation in 2024, which establishes the market scaffolding for the first EU-wide voluntary certification framework for carbon removal projects that are recognized by the European Commission. Approaches like this can help scale projects past the pilot phase by promoting investor confidence via regulatory recognition, while also providing a stepwise approach to stringency and compliance by starting in the voluntary space.

4. Lack of risk sharing: Market conditions silo farmers, regulators, and investors to manage their own risks

Introducing new practices can pose financial and operational risks for farmers–a global challenge farmers face in scaling climate-smart practices. Carbon credit payments are typically issued after GHG emissions are verified and credits are sold on the marketplace. This can create a lengthy period between farmers’ investment into practice and technology adoption and carbon credit payments. Depending on the project design and upfront capital availability from credit buyers (e.g., off-take agreements), project aggregators can provide intermediary payments to farmers that cover part of the credit value while the project goes through the MMRV process. This option, however, can create risks for investors–what if the project does not meet the MMRV standards and cannot generate credits? This dynamic of investor and farmer risks being at odds is critical to solve for in scaling agriculture offset projects. Carbon markets, especially compliance markets, impose strict guardrails around additionality, which requires proving the practice change was incentivized by the carbon market, often limiting use of funds from other incentives to supplement crediting gaps.

Climate-smart practices can contribute to improving profit margins, but it can take time. There are not only upfront costs such as purchasing cover crop seed, but risks to yields and margins if the new practice does not perform well. Bain and Company estimate that Canadian farmers who adopt climate-smart practices risk, on average, three to five years of potentially lower yields and higher costs per acre before they start to see profits.4 Farmers, are therefore, taking on risks that relate to market participation costs, especially for MMRV, and farm productivity losses if the practices do not deliver on robust GHG abatement.

5. Talent and innovation wanted: Canada is a laggard in carbon market expertise

The market design limitations, from fragmentation to unpractical protocols, has led to Canada falling behind in developing the right talent and tools needed to design protocols, scale projects and issue agriculture credits on the marketplace. In the meantime, our global peers are pulling ahead. The U.S., EU, and Australia, along with emerging economies like Brazil, are establishing large networks of relevant expertise, including project developers, agri-tech companies specializing in MMRV, and institutions and consultants that have deep knowledge and experience in defining market pathways for agriculture within environmental governance frameworks.

Government policy and programming that stimulates market development can play an important role in boosting carbon market know-how and expertise. The United States Department of Agriculture (USDA) launched Partnerships for Climate Smart Commodities in 2022–a US$3.1 billion investment in more than 140 projects that has provided technical and financial assistance to help producers implement climate-smart practices, pilot innovative and cost-effective methods for MMRV, and develop markets for climate-smart agriculture. According to the USDA, this investment has led to hundreds of expanded market opportunities and the reduction of 60MT GHG emissions over the projects’ lifespan.5 Investments like this also stimulate the need for support services, like agronomists and financial advisors in agriculture, to boost their expertise in positioning farmers to be successful in market-based mechanisms that incentivize GHG mitigation.

How other jurisdictions are approaching agriculture’s integration into industrial carbon pricing

Context:

The bloc traditionally supports climate-smart practices via subsidy programs, but as of 2024, the EU has been developing the market architecture for farmers to have more options for hybrid funding.

Approach:

The cornerstone of building the market architecture for agriculture to engage in carbon markets recognized by the European Commission is the Carbon Removals and Carbon Farming Regulation.

The CRFC establishes an EU-wide certification system for carbon removals for farmers to generate offsets that will first be available on voluntary markets. The EU is considering a step-wise approach that could lead to agriculture being integrated into the EU ETS.

Ambition:

Build market-based pathways for agriculture to engage in carbon markets that contribute to decarbonizing the EU food system with a strong focus on credit integrity and quality.

Context:

A market-driven approach since 2011 that is focused on agriculture integration into compliance markets as a core supply of credits.

Approach:

Australia’s compliance framework positions farmers to voluntarily generate Australian Carbon Credit Units that are bought by regulated, large industrial emitters and by the government via auction to guarentee long-term demand.

Focus on carbon removal credit creation from agriculture has led to credit integrity and quality debates.

Ambition:

Fully integrate agriculture into compliance markets as a source of offsets to contribute to national decarbonization targets.

Context:

California has aligned its cap-and-trade system with funds to invest in decarbonization, providing pathways for farmers to earn carbon credits and receive support for climate-smart projects.

Approach:

California’s cap-and-trade system covers regulated, large industrial emitters and allows companies to use a limited number of offset credits when they do not meet the compliance benchmark.

Agriculture can be a source of these credits via approved protocols including anerobic digestion and reducing methane from rice cultivation. To support carbon removals in agriculture, Californa uses funding programs like the Healthy Soils Program.

Ambition:

Provide multiple pathways for agriculture to be supported for climate-smart practice adoption via credits and funding programs, while reducing risks associated with removal credits in the compliance market.

Context:

Policy frameworks on compliance markets and agriculture’s participation are in transition and being consolidated. Currently there is a mix of voluntary markets, compliance pilots and funding programs with plans to develop a compliance market for large, industrial emitters and potentially include agriculture as a source for offsets.

Approach:

The Brazilian Greenhouse Gas Emissions Trading System (SBCE), established in 2024, is currently in its initial setup phase. The system is aiming for full operation by 2030. Policy experts are anticipating that agriculture will be positioned to produce credits under the trading system. The amount of offsets used by regulated emitters is expected to have a quantitative limit.

Ambition:

Position agriculture to be a voluntary participant in the compliance marketplace to help incentivize emissions reductions alongside other active mechanisms in the country like insetting programs and voluntary markets.

Context:

Agriculture, particularly methane emissions from livestock, is the largest source of emissions in the country, which has led to a heated debate on how to approach emissions reductions in the sector.

A carbon price for on-farm emissions was planned, but New Zealand’s updated 2026 Emissions Reduction Plan revised its approach to focus on investing in on-farm innovation and technology to help drive down GHG emissions.

Approach:

Currently agricultural practices are not regulated under the country’s ETS and farmers are generating credits via forestry projects.

To address its livestock emissions, the country has developed a public-private investment fund, AgriZero, for scaling innovations that are proven to reduce GHG emissions from livestock. This fund operates seperately from the ETS.

Ambition:

Balance the economic ambitions and GHG mitigation objectives of the livestock sector, recognizing it uniquely as a central driver for growth and the national GHG inventory.

Five ideas to grow agriculture’s market access

1. Develop a federal, provincial, and territory offset harmonization framework for agriculture

Harmonize agriculture offset registries, projects and protocols across provincial, territorial, and federal systems. It’s like lifting inter-provincial trade barriers. The federal government and provinces could negotiate formal harmonization revisions under the GGPPA covering:

-

Protocol equivalency recognition: Positions each jurisdiction to accept the other’s standards, reducing redundancies and red tape.

-

Credit fungibility: Stimulates market activity and diversified demand across jurisdictions.

-

Shared MMRV standards and safeguards: Avoids inconsistency in MMRV approaches and double accounting, while injecting clarity and certainty for investors on credit quality.

-

Registry interoperability: Allows for project developers and investors to scale projects across jurisdictions and seamlessly access, exchange and interpret data on projects across Canada.

-

Buffer pool coordination: Centralizes credit reserves that are used to act as an insurance policy across projects under equivalent protocols in the case of reversals or overstatements.

Under this framework, agricultural projects that meet federal environmental integrity standards could be developed across compliance markets. This approach could scale projects across more than one province with similar production systems. Examples include the Aspen Parkland, extending from Manitoba into Alberta, the Peace River Region, split between British Columbia and Alberta, and the Great Clay Belt, which crosses the northern border of Ontario into western Quebec. Such interoperability could increase market liquidity, minimize project cost for farmers and project developers, reduce administrative duplication, and create clearer incentives for farmers and investors.

Integrated carbon markets such as the Western Carbon Initiative that caps market activity at 352 megatonnes of GHG emissions across the participating jurisdictions, prove that harmonized systems are possible and produce deeper markets that can significantly increase trading volumes and price stability.6

To ensure agriculture offset harmonization does not invoke volatility and protects benchmark integrity, additional measures within a harmonized system could include:

-

Introducing a floor price for agricultural offsets tied to the federal carbon price

-

Allowing multi-year forward contracting between farms and industrial emitters

-

Setting annual issuance ceilings

-

Reviewing market impacts every three years

2. A transfer portal for agriculture projects from offset to inset markets

The lack of market integration for GHG mitigation projects across compliance and voluntary marketplaces is often pointed to as a barrier in growing investor activity and reducing market access challenges for farmers. The portal would allow projects to be transferred to voluntary carbon insetting registries—where companies are investing in GHG reductions in their supply chain. The transfer portal would therefore act as a mechanism to increase access to robust agriculture projects that are GHG mitigating and prevent oversupply in compliance markets.

Complementary to compliance with market demand, GHG mitigating agricultural projects are sought after from agri-food companies that have made commitments to reduce their supply-chain’s GHG emissions (i.e., Scope 3), which primarily come from agriculture production. Creating a national transfer portal for agricultural projects would allow projects to be redirected to corporate agri-food buyers seeking to reduce their supply-chain emissions. Transferring offset projects to an inset project can require some changes to the MMRV approach, such as changing the baseline measurement from an intervention to an inventory methodology. But making such changes when projects are transferred is necessary to do before issuing credits because international guidance for agri-food companies with scope 3 targets prohibits the use of offset credits in accounting scope 3 emissions reductions. Enabling such transfers is being led by groups like VERRA, who will soon publish guidance on how to transfer projects from their voluntary offset registry, Verified Carbon Standard (VCS) to their inset program, Scope 3 Standard (S3S). Allowing this type of market integration could create the market conditions necessary to boost agri-food companies confidence and investment in Canada-based inset projects because they would be following government approved protocols.

3. Create a dedicated “agriculture offset stream” within OBPS

An agriculture offset stream defined within regulated emitters’ allotted use of offset credits could be an approach to balancing the risk of flooding the market with credits, while also stimulating targeted agriculture offset credit creation. Within the existing caps and limitations for offset use across the provincial and federal system, this agriculture offset stream could be carved out of the existing requirements for regulated emitters purchasing offsets, where they must dedicate a share of their purchases to agriculture projects when projects are available on the marketplace.

Agricultural offsets should be integrated into the industrial carbon market in a way that supports cost containment without weakening incentives for industrial decarbonization. As industrial benchmarks tighten toward Canada’s 2035 and 2050 climate targets, the required use of agricultural offsets could gradually decline.

This structure would allow agricultural credits to play three complementary roles, while ensuring that industrial decarbonization remains the primary driver of emissions reductions:

-

Provide cost containment for industry

-

Generate new income streams for farmers and support rural economies

-

Deliver incremental mitigation outside heavy industry.

4. Accelerate approval of applicable agriculture protocols

Not all agricultural offsets projects are equal in their strategic value. Recognizing that some agriculture offsets have more co-benefits than others and some carry more risk, Canada could adopt a public hierarchy for agriculture protocol development that tiers climate-smart practices by their MMRV cost and risks, GHG mitigation impact and co-benefits to prioritize protocol development and reform.

-

High-priority protocols could focus on offsets that have strong MMRV frameworks and deliver tangible long-term economic value beyond credits, including:

-

Manure digesters linked to renewable natural gas

-

Livestock methane-reducing feed additives

-

Precision nitrogen management

-

-

Medium-priority protocols could focus on those that have broader ecosystem service values and are identified as critical to building resilience, but have less certainty in MMRV, including:

-

Cover cropping

-

Reduced/no-till systems

-

Improved crop rotations

-

Grassland restoration

-

Edge of field rehabilitation (e.g., restoring wetlands)

-

-

Low priority protocols could focus on emerging practices that have potential but require scaling in processing or advancements in technologies to be applicable in Canada, including:

-

Biochar

-

Microbial inoculants

-

The science behind MMRV of agriculture protocols is not perfect—our understanding of natural ecosystems is inherently limited–and there are material risks in miscalculating the correlation between farmers’ practice adoption and GHG mitigation outcome. Yet, there are ways to responsibly manage these risks, while accelerating the approval process of protocols.

For example, agriculture protocols can adopt:

-

Conservative baselines

-

Additionality tests against counterfactual baselines

-

Reversal risk buffers

-

20+ year monitoring frameworks for soil carbon

5. Aggregate agriculture offset projects and invest in regional MMRV to achieve critical mass

Most Canadian farms can influence relatively small volumes of GHG emissions reductions, often making the cost of registering and verifying individual farm offset projects cost prohibitive. But many Canadian farmers are also unclear on the pathways to participate in aggregated projects.

To overcome these barriers, the federal government could establish a national aggregation framework that licenses third-party project aggregators via the existing Credit and Tracking System (CATS), and publicly lists them when they are developing projects for farmers to enroll, which would be in addition to the list of active projects listed on the registry. This list of third-party aggregators then becomes the trusted gateway for farmers seeking opportunities to participate in projects.

Complementary to improving the transparency in market access, federal and provincial governments could also consider structuring funding streams under programs like the Agricultural Clean Technology Program that are dedicated to improving regional approaches to MMRV frameworks. The funding stream could be accessible by agriculture organizations in partnership with project aggregators to develop on-the-ground resources and technical expertise that help facilitate farmer participation in projects and adoption of technology required to collect data for MMRV systems and drive down GHG emissions. Advanced targeted investments in MMRV technology and resources that are required to issue robust agriculture offset credits include:

-

Remote sensing and satellite-based soil monitoring

-

Streamlined and consistent soil sampling processes

-

Integration of digital farm data platforms and farmer awareness on data requirements

-

Standardized emission factors for climate smart-practices that are regionally adapted.

By adopting a more inclusive model of project development and opportunities for engagement, Canada could expand agriculture’s participation in the marketplace while maintaining rigorous environmental oversight.

Download the report

Author

Lisa Ashton, Interim Head of Climate Action Institute & Policy Lead, Agriculture and Nature, RBC Thought Leadership

Editorial

John Intini, Senior Director, Editorial, RBC Thought Leadership

Yadullah Hussain, Managing Editor, RBC Thought Leadership

Caprice Biasoni, Design Lead, RBC Thought Leadership

Lavanya Kaleeswaran, Director, Digital & Production, RBC Thought Leadership

Canadian Federation of Agriculture. Environmental Sustainability and Climate Change.

Drever, R. et al. Natural Climate Solutions for Canada. Science Advances, 2021.

Haya, B. et al. Voluntary Registry Offsets Database – Berkeley Carbon Trading Project, 2026.

Bain and Company. Helping Farmers Shift to Regenerative Agriculture, 2021.

USDA. Partnership for Climate-Smart Commodities, 2025..

Western Climate Initiative. Results and Impact, 2026.

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. The reader is solely liable for any use of the information contained in this document and Royal Bank of Canada (“RBC”) nor any of its affiliates nor any of their respective directors, officers, employees or agents shall be held responsible for any direct or indirect damages arising from the use of this document by the reader. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates. This document may contain forward-looking statements within the meaning of certain securities laws, which are subject to RBC’s caution regarding forward-looking statements. ESG (including climate) metrics, data and other information contained on this website are or may be based on assumptions, estimates and judgements. For cautionary statements relating to the information on this website, refer to the “Caution regarding forward-looking statements” and the “Important notice regarding this document” sections in our latest climate report or sustainability report, available at: https://www.rbc.com/our-impact/sustainability-reporting/index.html. Except as required by law, none of RBC nor any of its affiliates undertake to update any information in this document.