For week of Mar. 23

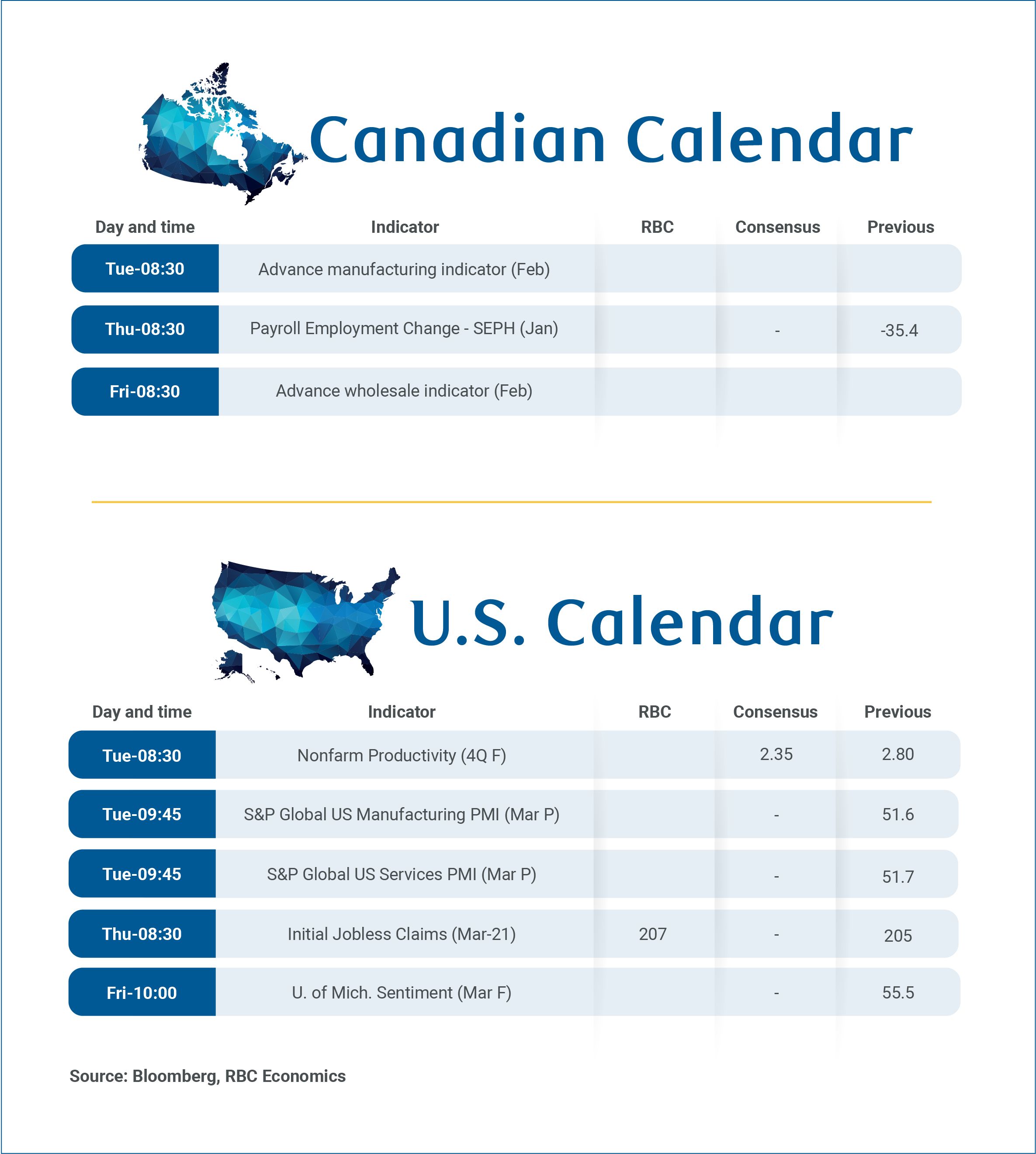

Economic data releases in Canada are quiet in the week ahead with the most notable being January’s Survey of Employment, Payrolls and Hours (SEPH) on Thursday, when we expect further stabilization in job vacancies following improvements in timelier job openings data from Indeed Hiring Lab.

February’s labour market report was weak with the unemployment rate rising to 6.7%. However, layoffs remained low and the unemployment rate was still below 7% in Q3, and 6.8% in Q4 2025.

Solid domestic demand beneath weak headline gross domestic product in Q4 2025 should continue to support a rebound in hiring early this year. We still look for the unemployment rate to gradually decline to 6.3% by the end of 2026.

We will also receive advance February industry data that should show a partial rebound after disruptions in the auto industry drove large declines in January.

Manufacturing sales dropped 3.9% due to a significant decline in transport equipment sales from atypical production disruptions at several Ontario plants. Wholesale sales also fell 1.5% in January. Some moderation in production disruptions should support a partial rebound in February sales with manufacturing on Tuesday and wholesales on Friday.

BoC and Fed stand pat on rates

Overall, as the Bank of Canada noted in its meeting on Wednesday, the economy started Q1 on a softer footing than expected. However, with weakness in production mostly driven by disruptions in the auto sector, we expect some recovery later in the quarter.

We have left our outlook for modest growth and improved per-capita economic conditions this year broadly unchanged, and for now expects relatively neutral economic impact from recent oil price increases in both Canada and the U.S. –with the BoC and U.S. Federal Reserve remaining on hold through 2026.

At their meetings this week, both central banks held rates steady and refrained from commenting too much on the economic impact from the ongoing Middle East conflict.

In Canada, persistently weak inflation pressure prior to the oil price shock should leave the BoC with room to wait for additional clarity, compared to the U.S., where inflation pressures have been more stubborn, and tariff-related pressures are starting to show up.

This report was authored by Senior Economist Claire Fan and Economist Abbey Xu.

Explore the latest from RBC Economics:

Saskatchewan Budget 2026. Taking the longer road to fiscal balance

Quebec Budget 2026: Showing restraint in an election year

Canadian Analysis. Bank of Canada meeting recap: One supply shock after another

U.S. Analysis. FOMC Recap: Fed remains on pause with uncertain path ahead

RBC Consumer Spending. Canadian cardholder spending warms up despite discretionary goods pullback

Monthly Housing Market Update. Canada’s housing market in a stalemate this February

Canadian Analysis. Canadian household balance sheets remained resilient in Q4/25

Canadian Analysis. More signs of easing inflation pressure in Canada ahead of rising oil prices

Share these insights with your network:

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. The reader is solely liable for any use of the information contained in this document and Royal Bank of Canada (“RBC”) nor any of its affiliates nor any of their respective directors, officers, employees or agents shall be held responsible for any direct or indirect damages arising from the use of this document by the reader. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.

This document may contain forward-looking statements within the meaning of certain securities laws, which are subject to RBC’s caution regarding forward-looking statements. ESG (including climate) metrics, data and other information contained on this website are or may be based on assumptions, estimates and judgements. For cautionary statements relating to the information on this website, refer to the “Caution regarding forward-looking statements” and the “Important notice regarding this document” sections in our latest climate report or sustainability report, available at: https://www.rbc.com/community-social-impact/reporting-performance/index.html. Except as required by law, none of RBC nor any of its affiliates undertake to update any information in this document.