For week of Mar. 30

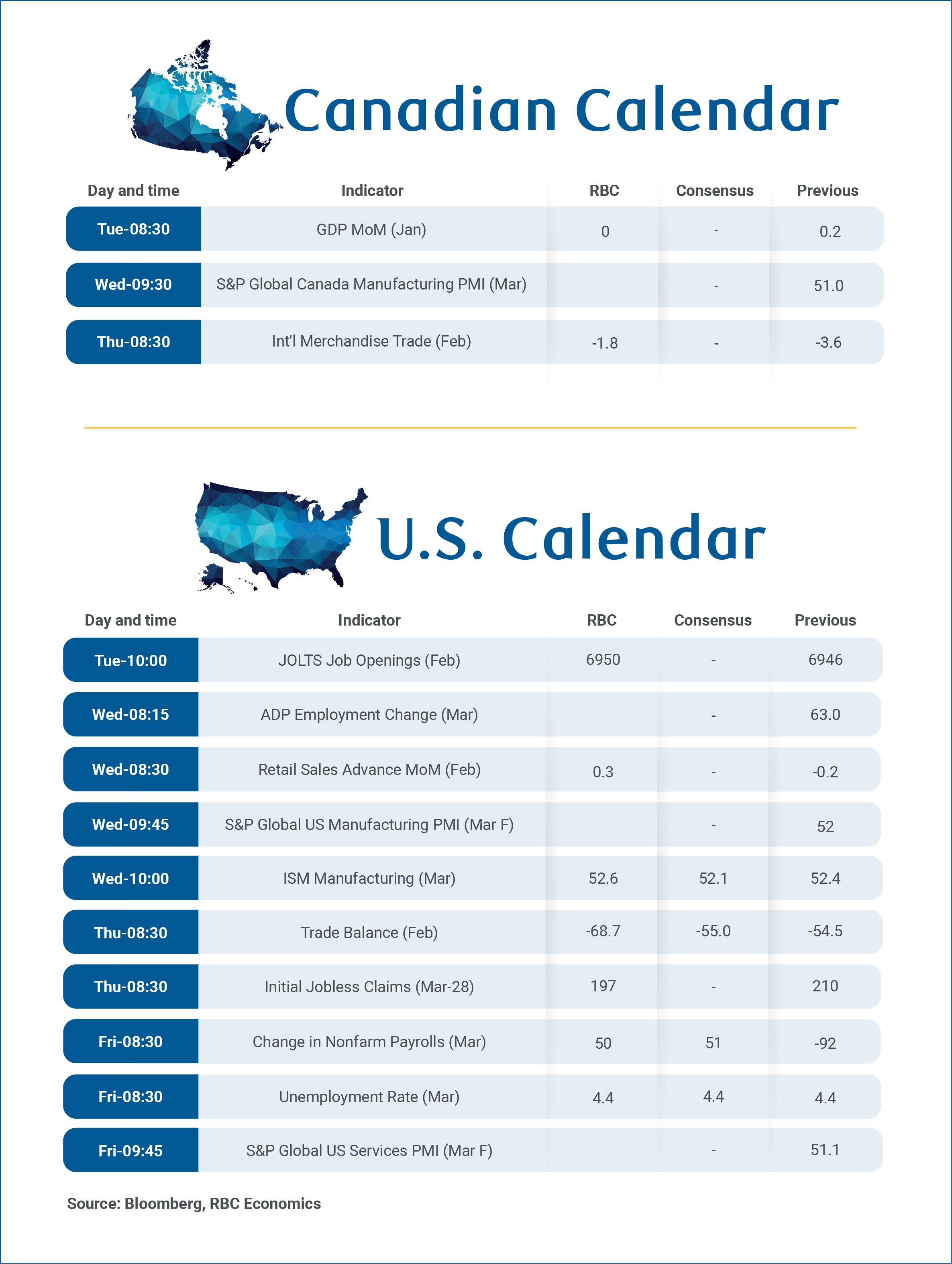

Canada’s gross domestic product for January on Tuesday, and February trade data on Thursday will provide more clues on the economy’s trajectory in early 2026.

In line with Statistics Canada’s advance estimate, we expect GDP growth to have slowed to essentially flat in January after rising 0.2% in December.

Weakness was concentrated in the auto sector, where production disruptions at Ontario plants drove manufacturing and wholesale sales down 3.9% and 1.5%, respectively. Early indicators, however, point to a partial rebound in February as disruptions unwound.

Real estate agents and broker services also weakened, as unusually harsh weather dampened home resales in January. Strength in energy sectors offset these declines with Alberta’s non-conventional oil production and mining (excluding oil and gas) both rising modestly after contracting in December. Retail sales increased 1%, reflecting resilient household spending.

February indicators point to partial rebound

Spending resilience appears to have extended into February. Early indicators including our tracking of RBC card spending data, as well as Statistics Canada’s advance retail sales estimate (a 0.9% nominal increase) all point to improvement.

Other advance industry estimates also showed recovery. Manufacturing sales rose 3.8% in nominal terms, according to Statistics Canada, driven by strength in transportation equipment and food product manufacturing. Wholesale sales increased 2.3%, lifted similarly by higher auto and parts sales. Housing-related activity likely remained soft in February as home resales remained soft.

The Bank of Canada flagged downside risks to their 1.8% annualized GDP growth forecast for Q1 at the March meeting. After a weak January, improvements in activities in February and March as auto disruptions eased should still leave growth on balance in line with our forecast for a modest increase.

For February’s international trade data, we expect a narrowing in Canada’s trade deficit from $3.6 billion to $1.8 billion driven by a partial rebound in auto exports and higher oil prices. The deficit should continue to narrow in March after the Middle East conflict drove oil prices sharply higher.

-

We expect next week’s U.S. March payroll report to show a 50,000 increase in employment, partly driven by the end of the nurses’ strike. The unemployment rate is expected to remain steady at 4.4%, given subdued layoffs and stable initial jobless claims.

This report was authored by Senior Economist Claire Fan and Economist Abbey Xu.

Explore the latest from RBC Economics:

Ontario Budget. Delayed path to balance

Podcast: The 10-Minute Take. Are higher oil prices good or bad for Canada’s economy?

Manitoba Budget 2026. Path to balance maintained despite negative in-year surprise

Share these insights with your network:

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. The reader is solely liable for any use of the information contained in this document and Royal Bank of Canada (“RBC”) nor any of its affiliates nor any of their respective directors, officers, employees or agents shall be held responsible for any direct or indirect damages arising from the use of this document by the reader. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.

This document may contain forward-looking statements within the meaning of certain securities laws, which are subject to RBC’s caution regarding forward-looking statements. ESG (including climate) metrics, data and other information contained on this website are or may be based on assumptions, estimates and judgements. For cautionary statements relating to the information on this website, refer to the “Caution regarding forward-looking statements” and the “Important notice regarding this document” sections in our latest climate report or sustainability report, available at: https://www.rbc.com/community-social-impact/reporting-performance/index.html. Except as required by law, none of RBC nor any of its affiliates undertake to update any information in this document.