The Bottom Line:

Canadian labour markets showed further signs of steadying in June after a larger improvement in May.

The employment increase itself in June (+18k) left the measure still down 6k on net for the year. But we continue to think that slower employment gains should be expected given a sharp slowing in Canadian population growth.

Critically, controlling for changes in the demographic backdrop, per-worker labour market conditions held onto a larger-than-expected improvement in May with the unemployment rate edging down to 6.5% in June from 6.6% the prior month, led by a pullback in the youth unemployment rate on an improved summer job market.

The labour market is still not strong—the unemployment rate is still higher than normal. But economic growth data has also shown signs of picking up in Q2 after stalling over the winter.

U.S. tariff rates have been drifting broadly lower rather than higher—CUSMA continues to backstop duty-free trade for most Canadian exports to the U.S. And oil prices have moved off of April/May peaks despite uncertainty around the evolution of the conflict in the middle east.

Against that backdrop, the June labour market data is broadly consistent with our own base-case that Canada’s economy is broadly still improving on a per-person and per-worker basis and we continue to look for the unemployment rate to edge down further over the second half of the year.

The details:

-

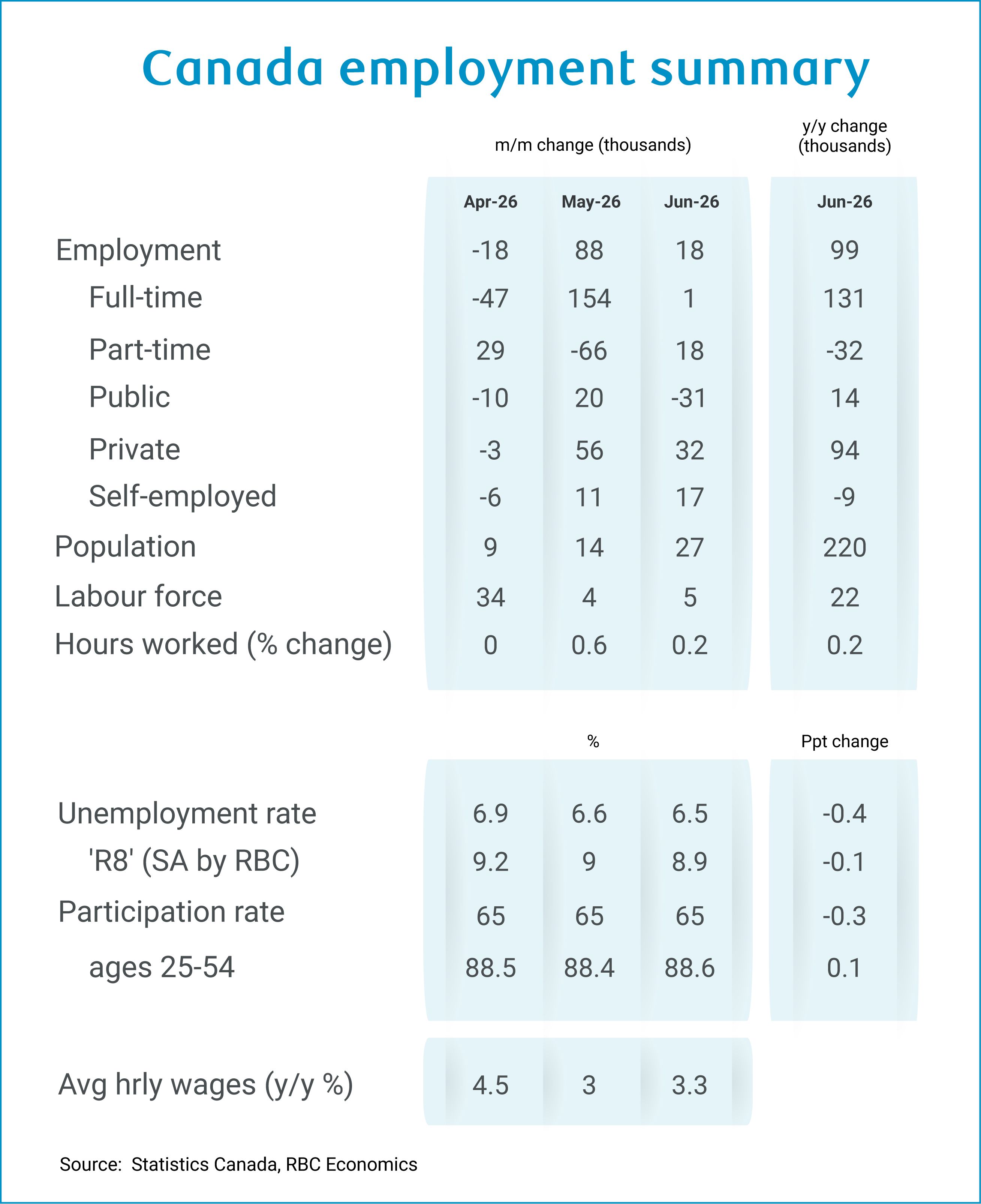

Employment rose 18k in June, adding to the 88k jump in May although still down 6k over the first half of 2026 in total following softer readings in prior months.

-

Full-time employment was little changed (+1k) but is still up 43k year-to-date following a 154k surge in May.

-

On an industry basis, manufacturing employment more-than-retraced a 15k May increase with a 17k drop in June—and left the employment count in that heavily trade-exposed sector at -38k over the first half of the year. But service-sector jobs jumped 62k in June and are up 45k year-to-date.

-

The 15+ population unexpectedly posted a 27k increase—a slightly puzzling gain given the unprecedented outright declines in total population counts in recent quarters.

-

But controlling for underlying demographic trends (slower broader population growth and a structurally aging population), per-worker labour market conditions showed further signs of improvement.

-

The unemployment rate edged down to 6.5%, to build on a 0.3 ppt drop to 6.6% in May from 6.9% in April.

-

And the labour force participation rate held at 65.0% despite a tick up in the retirement rate to 27k per-month over the last year from 26k per month measured in May.

-

Total hours worked edged up 0.2% to build on the 0.6% increase in May, and consistent with other early indicators pointing to a pickup in Q2 GDP growth

-

Wage growth edged up to 3.3% but still down from the 4.5%+ rates in March and April. While unemployment has begun to edge lower, it is still elevated and that is expected to keep wage growth under pressure in the near-term.

-

Regionally, the decline in June’s unemployment rate was fairly broad-based. Quebec led employment gains with a 15,000 increase, the second consecutive increase, narrowing year-to-date losses to roughly 60,000. The unemployment rate fell 0.2 percentage points to 5.4%, tying Manitoba as the lowest nationally, and in the CMA of Montreal dropped 0.6 percentage points to 5.9%.

-

British Columbia (7,800), Nova Scotia (4,900), Saskatchewan (2,900), also posted gains, lowering their unemployment rates. Ontario shed 17,000 jobs though the unemployment rate held steady at 7%. Alberta saw its unemployment rate rise 0.4 percentage points to 7%, as labour force growth outpaced job creation.

About the author:

Nathan Janzen is an Assistant Chief Economist, leading the macroeconomic analysis group. His focus is on analysis and forecasting macroeconomic developments in Canada and the United States.

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. The reader is solely liable for any use of the information contained in this document and Royal Bank of Canada (“RBC”) nor any of its affiliates nor any of their respective directors, officers, employees or agents shall be held responsible for any direct or indirect damages arising from the use of this document by the reader. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.

This document may contain forward-looking statements within the meaning of certain securities laws, which are subject to RBC’s caution regarding forward-looking statements. ESG (including climate) metrics, data and other information contained on this website are or may be based on assumptions, estimates and judgements. For cautionary statements relating to the information on this website, refer to the “Caution regarding forward-looking statements” and the “Important notice regarding this document” sections in our latest climate report or sustainability report, available at: https://www.rbc.com/community-social-impact/reporting-performance/index.html. Except as required by law, none of RBC nor any of its affiliates undertake to update any information in this document.