The week of June 29th

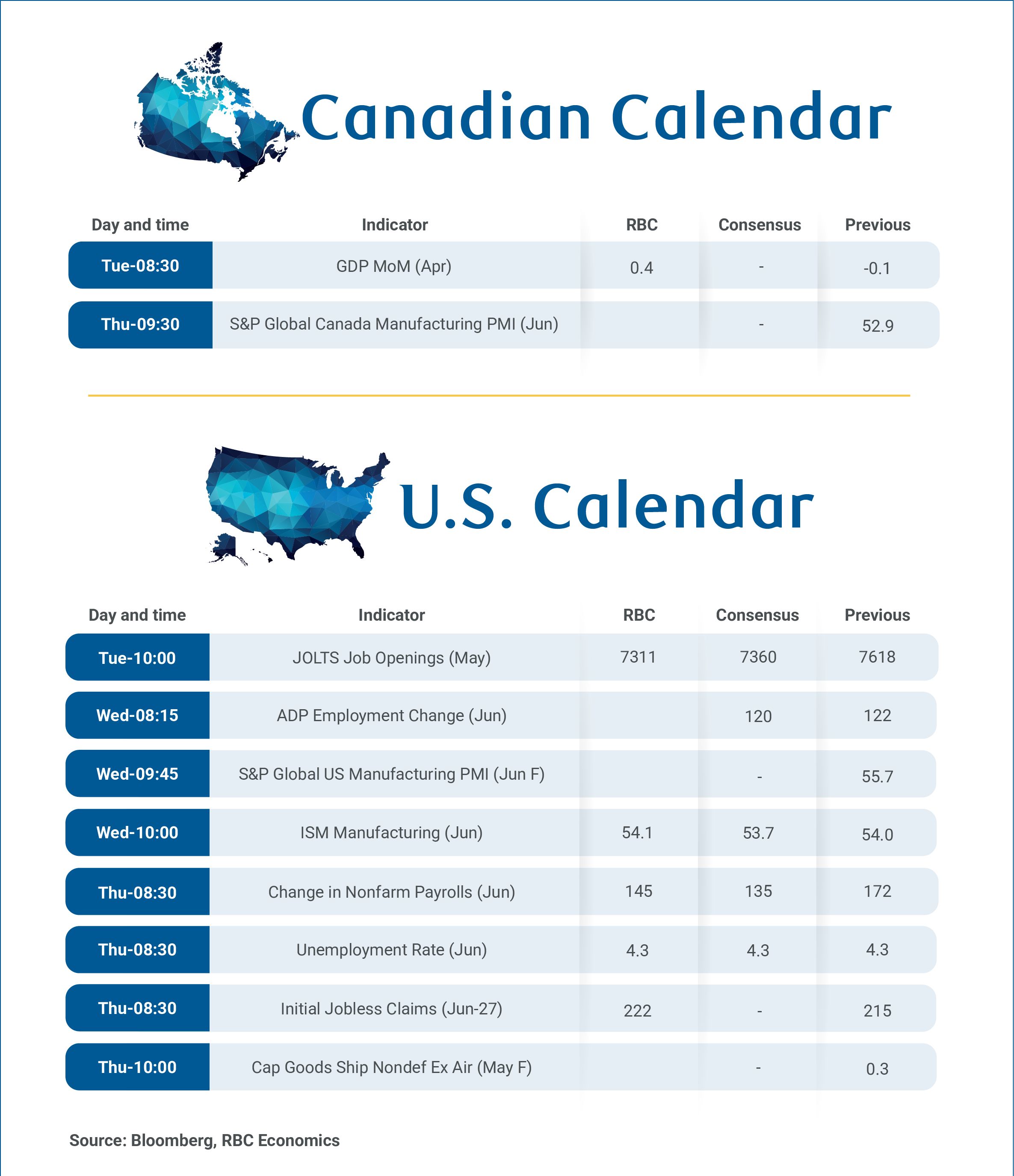

We expect real gross domestic product in Canada to show a 0.4% increase in April on Tuesday after stagnating for two straight quarters.

That would be consistent with Statistics Canada’s preliminary estimate a month ago, although we expect it was led by a relatively narrow rebound in mining, oil and gas extraction.

Early data is pointing to a significant increase in non-conventional oil extraction and oil drilling in April. Adding in a pickup in manufacturing GDP, goods-producing sectors overall likely expanded by 1%.

Service sector GDP is expected to have gained 0.1% with weaker wholesales (-0.3%), and flat retail GDP offset by growth in other industries including real estate and rentals after Canadian home resales ticked higher (seasonally adjusted) in April for the first time since October 2025.

Preliminary monthly GDP data has been highly revision-prone, but overall, data has been pointing to a firming in economic activity in Q2 with early May data also looking broadly better.

Labour market data in May firmed, and the housing market continued to show signs of thawing with resales up 5.1% from April (the largest increase since October 2024).

StatCan’s advanced indicators also pointed to rising nominal retail and manufacturing sales in May, the former consistent with our card transactions tracker suggesting resilient, albeit slightly weaker spending growth.

And, global oil prices have moved lower in recent weeks. If sustained, those declines will help to restore some household purchasing power eroded by higher fuel costs, while also limiting risks of inflation spreading beyond energy prices.

BoC to stay on hold in 2026

The combination of signs of firming Q2 GDP growth, and easing inflation pressures should help to validate the Bank of Canada’s call to not overreact to temporarily higher oil prices or mechanically softer economic data. With growth picking up in Q2 and core inflation remaining subdued, we continue to expect no change in interest rates from the central bank in 2026.

South of the border, the U.S. Federal Reserve tilted decidedly hawkish in their latest meeting—first under new Chair Kevin Warsh. Half of the FOMC (excluding Warsh) expected at least one rate hike in 2026, prompted by concerns over sticky-to-accelerating core inflation readings while labour markets remain robust.

On Thursday, we expect May’s U.S. employment report to broadly reinforce that view with a 145,000 payrolls’ gain, alongside a steadily low 4.3% unemployment rate.

About the authors:

Nathan Janzen is an Assistant Chief Economist, leading the macroeconomic analysis group. His focus is on analysis and forecasting macroeconomic developments in Canada and the United States.

Claire Fan is a Senior Economist at RBC. She focuses on macroeconomic analysis and is responsible for projecting key indicators including GDP, employment and inflation for Canada and the US.

Explore the latest from RBC Economics:

June Monthly Exec Briefing: US consumer bruised by persistent inflation

Energy drives Canada’s inflation to 3.2% as underlying pressures stay contained

Podcast: The 10-Minute Take. New Fed Chair’s first meeting: Inflation takes priority

Share these insights with your network:

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. The reader is solely liable for any use of the information contained in this document and Royal Bank of Canada (“RBC”) nor any of its affiliates nor any of their respective directors, officers, employees or agents shall be held responsible for any direct or indirect damages arising from the use of this document by the reader. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.

This document may contain forward-looking statements within the meaning of certain securities laws, which are subject to RBC’s caution regarding forward-looking statements. ESG (including climate) metrics, data and other information contained on this website are or may be based on assumptions, estimates and judgements. For cautionary statements relating to the information on this website, refer to the “Caution regarding forward-looking statements” and the “Important notice regarding this document” sections in our latest climate report or sustainability report, available at: https://www.rbc.com/community-social-impact/reporting-performance/index.html. Except as required by law, none of RBC nor any of its affiliates undertake to update any information in this document.