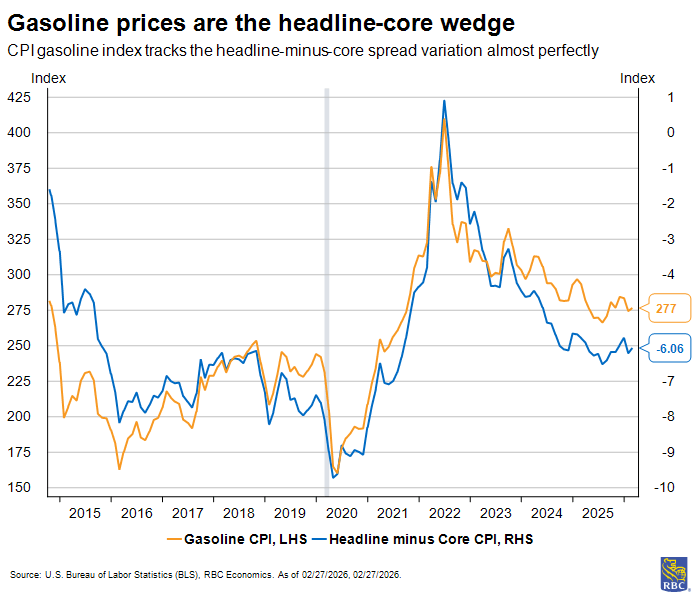

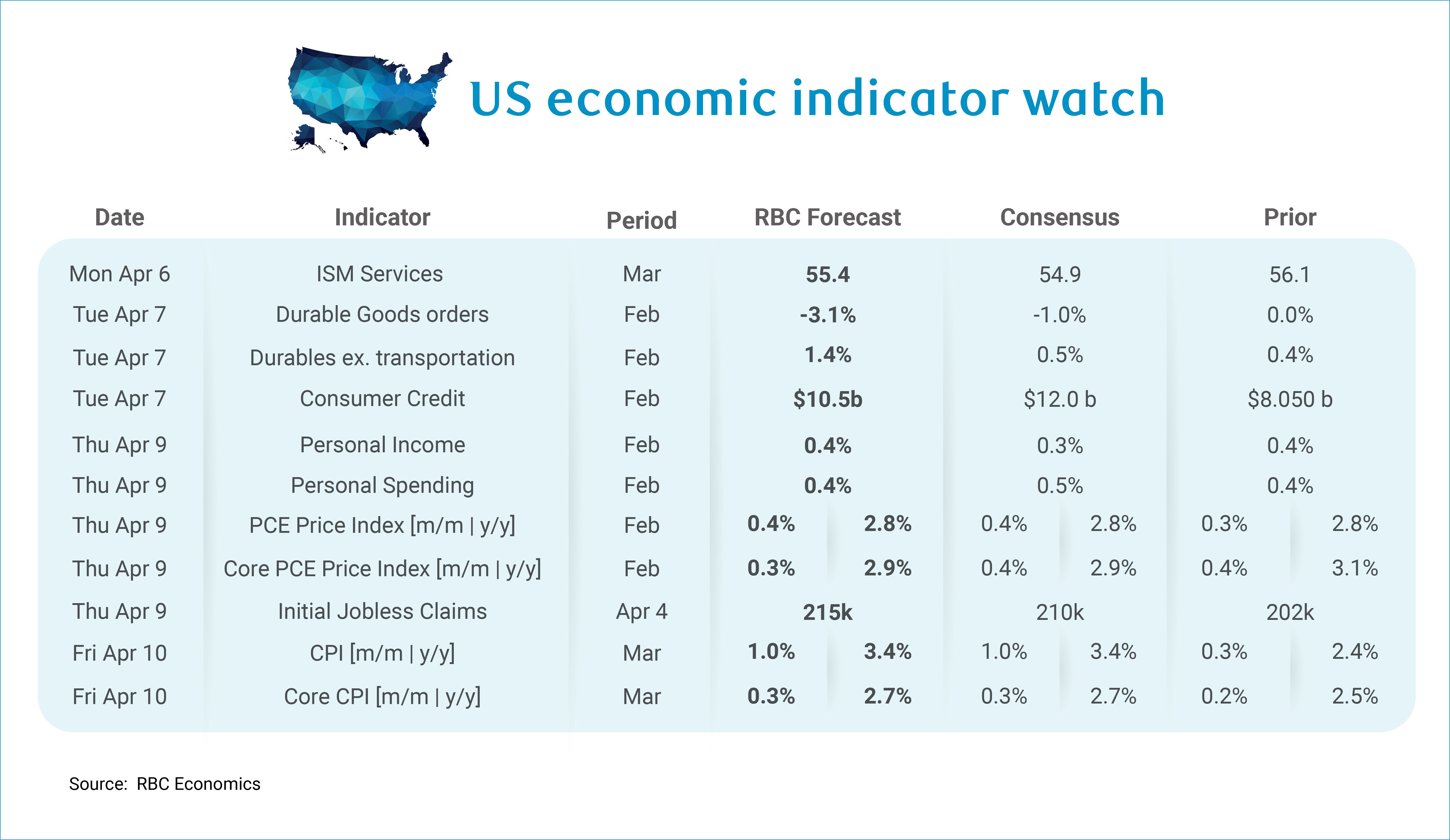

Next week’s headline inflation print will garner the most attention, though we will still be laser focused on core inflation for continued signs of tariff passthrough. We expect core inflation rose +0.3% m/m in March, bringing the year-over-year pace to 2.7%. Still, it will be difficult to ignore what we expect will be the highest monthly headline print since Russia’s invasion of Ukraine in 2022. We expect to see that headline inflation rose by +1.0% m/m in the wake of the Middle East conflict, pushing the year-over-year pace to 3.4%.

At the onset of the conflict, we estimated that for every $10 per barrel increase in oil prices (WTI), gasoline prices rise roughly 30 cents. Indeed, in March, average WTI prices rose by over $26 per barrel and gasoline prices rose 77 cents, a 26% increase over the month. While we will not immediately see secondary effects show up in the March report, over the longer term we are more concerned about the passthrough of higher energy prices to transport costs and fertilizer prices should higher oil prices be sustained. If WTI prices settle at $100 barrel, we expect headline inflation will likely surpass 3.5% and stay there throughout the year. Outside of energy, the US Department of Agriculture’s farmer prices paid index suggests there is little relief to be had where food prices are concerned. Beneath the surface, we have witnessed price pressures materializing from tariffs for trade-exposed goods like household furnishings and supplies, apparel, and recreation commodities. Three consecutive months of strong PPI prints add additional conviction to our view that the tariff passthrough is well underway.

We have acknowledged before that there is little that the Fed can do to combat an oil price shock other than wait and see. Monetary policy is not an effective tool to combat a geopolitical shock any more than a tariff shock. If anything, inflationary pressures will handcuff the Fed and further solidifies our view that the FOMC will remain on pause throughout the year. Still, consumer perceptions will matter and as we have written before, prices for essentials like gasoline and food influence on consumers’ perceptions of inflation and wage expectations. And expectations will be top of mind for a Fed that is no longer in the driver’s seat.

Aside from CPI, here’s what else we are watching:

-

PCE data for February will be stale, but we expect it will continue to highlight a growing divide between core PCE and core CPI due to different weighting and methodological quirks associated with the handling of missing shelter CPI data during the government shutdown. With this in mind, we will be giving more weight to core PCE, especially for the next few months. Core PCE likely rose +0.3% m/m in February, with headline up slightly higher +0.4% m/m.

-

Both personal income and personal spending likely rose by +0.4% m/m in February. We expect to see the personal savings rate tick lower to 4.4%. Spending on both durables and non-durables grew at a healthy clip in February after a strong retail sales print was supported across nearly all spend categories (excluding furniture sales). And despite inclement weather in February, strong restaurant spending proved consumers maintain a healthy appetite for discretionary spending. But a retracement in the S&P will translate to weaker financial services spending in February and subtract from otherwise strong services sector spending.

-

We expect that the ISM Services index will continue to expand in March, though at a slightly more subdued pace than we saw in February. Data among the four regional Fed surveys were mixed, with Texas and Philadelphia pointing to weaker activity and Kansas City and Richmond Fed Surveys showing improvement.

-

We expect to see that durable goods orders fell during the month of February relative to January, entirely a reflection of weaker Boeing orders. Excluding transportation, durable goods orders likely improved in February. Nondefense capital goods orders are expected to tick up, excluding aircraft.

-

We expect initial jobless claims will come in at 215k for the week ending April 4th, after dipping the week prior. Throughout the first quarter, jobless claims have largely held steady as firms facing uncertainty paralysis in the midst of simultaneous oil and trade shocks opt not to lay staff off. In the current environment, firms can opt to reduce headcount without laying staff off by choosing not to backfill roles left vacated by retirees.

About the Authors :

Mike Reid is Head of US Economics at RBC. He is responsible for generating RBC’s US economic outlook, providing commentary on macro indicators, and producing written analysis around the economic backdrop.

Carrie Freestone is a Senior US Economist at RBC. Carrie is responsible for projecting key US indicators including GDP, employment, consumer spending and inflation for the US. She also contributes to commentary surrounding the US economic backdrop which she delivers to clients through publications, presentations, and the media.

Imri Haggin is an US Economist at RBC, where he focuses on thematic research. His prior work has centered on consumer credit dynamics and treasury modeling, with an emphasis on leveraging data to understand behavior.

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. The reader is solely liable for any use of the information contained in this document and Royal Bank of Canada (“RBC”) nor any of its affiliates nor any of their respective directors, officers, employees or agents shall be held responsible for any direct or indirect damages arising from the use of this document by the reader. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.

This document may contain forward-looking statements within the meaning of certain securities laws, which are subject to RBC’s caution regarding forward-looking statements. ESG (including climate) metrics, data and other information contained on this website are or may be based on assumptions, estimates and judgements. For cautionary statements relating to the information on this website, refer to the “Caution regarding forward-looking statements” and the “Important notice regarding this document” sections in our latest climate report or sustainability report, available at: https://www.rbc.com/community-social-impact/reporting-performance/index.html. Except as required by law, none of RBC nor any of its affiliates undertake to update any information in this document.