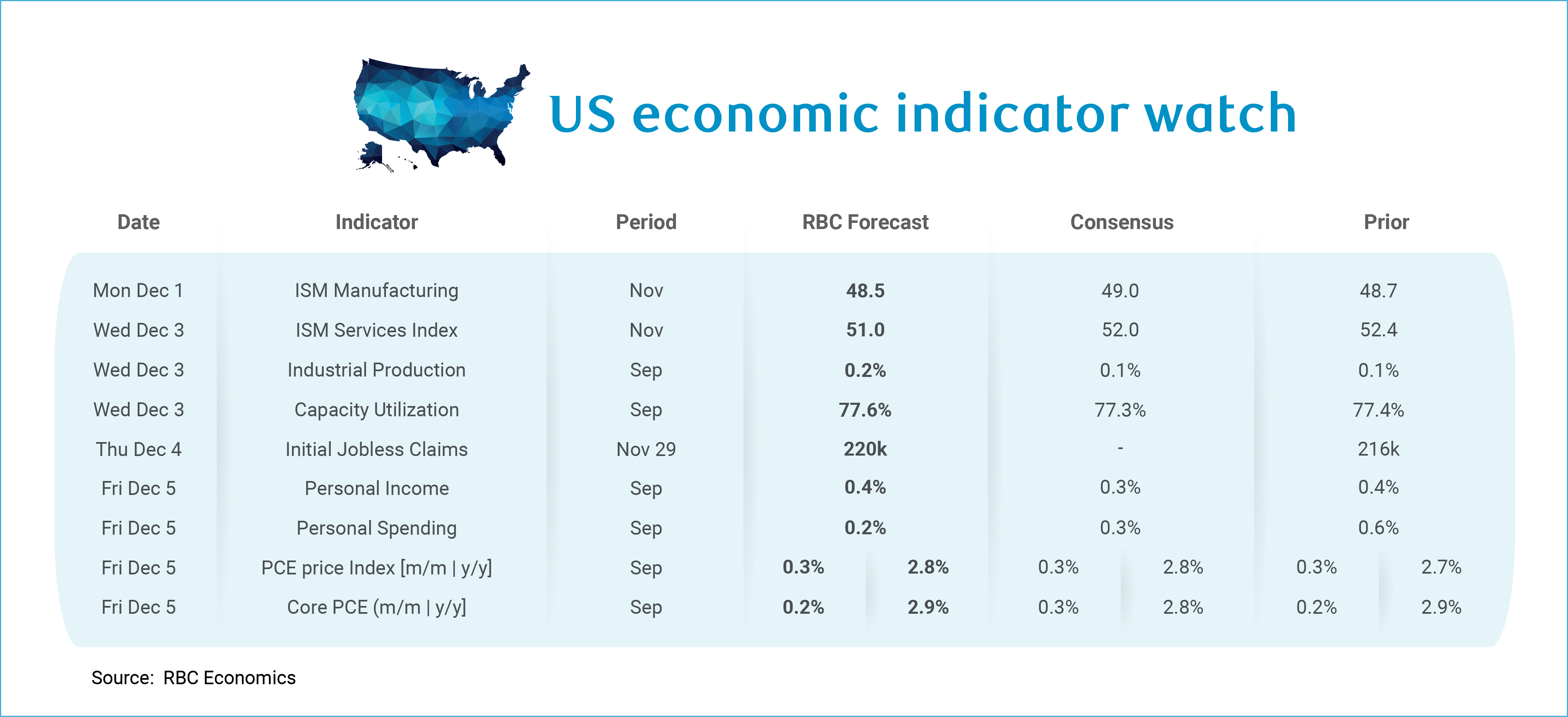

We get more delayed September data in the coming week with the PCE data landing on Friday. This will be top of mind for the Fed ahead of their rate decision the following week.

Heading into the December meeting, we know that the Fed faces significant data visibility challenges with lagged data on both sides of the mandate. Core PCE – as the Fed’s preferred measure of inflation – is expected to continue to heat up (+0.2% m/m), leaving the year-over-year pace of inflation just below 3%, well-above the Fed’s target. Even though the September inflation report was a downside surprise, we do not expect the PCE measure to benefit from the same reprieve that we saw in CPI. The downside in the CPI data could be largely attributed to a significant slowdown – likely a one-off – in the pace of growth for the Owners’ Equivalent of Rent (OER) component of the CPI basket. This matters because shelter bears less weight in the PCE price index. And despite a PPI print that looked cooler on the surface, specific price indices within the PPI that matter more for PCE – like home health care, nursing home care, and scheduled domestic passenger air transport – were hotter in September.

Consumer momentum also matters for both halves of the Fed’s mandate. And we expect to see growth in personal spending moderate in September (+0.1% m/m) after this week’s retail sales report pointed to US consumers running out of steam in September after months of front-loading. An outright decline in the retail sales control group (which excludes auto sales, building materials, gasoline, and restaurant spending) was the first since April. Lower motor vehicle sales suggested softer durable goods spending and non-durables are expected to slow from August. Services will likely continue to hold up as the upper end of the K (higher income households) continues to spend, if September spending on food services and drinking places was any indication. Personal income is expected to continue to grow at a healthy clip (+0.3% m/m in September) but non-labor income (specifically, personal current transfer receipts i.e. social security and Medicare, and dividend income), in many cases, will outpace wage growth.

On the back of strong spending through the summer, we see room for a slight upside to our Q3 GDP print ahead of Q4 where the government shutdown is expected to meaningfully hamper growth. Still, flagging consumer activity in September paints a worrying picture ahead of full tariff passthrough as the Fed grapples with two uncomfortable realities – inflation that is stuck well-above target and growth that is grinding lower. We still expect to see a pause at the December meeting before additional data releases help clear the fog, but with increasing risk of a cut after an upside to unemployment in September helped the doves argue their case to a FOMC that has increasingly shown preference to the labor side of the mandate.

Aside from personal income and outlays, we have the following releases:

-

We start the week off with some soft data for November – ISM Manufacturing data lands on Monday and is expected to continue to point to weaker activity. Three of five regional Fed manufacturing indices (Richmond, Texas, and Philly) pointed to softening activity. ISM Services will likely report another month of expansion in November, though at a slower pace.

-

Industrial Production and Capacity Utilization data for September will finally be published on Wednesday. We expect to see that the Industrial Production measure improved slightly in September (+0.2% m/m) as both an uptick in September ISM manufacturing and higher electric utility output point to an improvement in activity while manufacturing hours worked ticked up. This would nudge the capacity utilization rate up to 77.6% in September.

-

Initial Jobless Claims will likely land around 220k next week for the week ending November 29th but it is worth noting that we could likely see some volatility in this measure during the holiday week. Any major upside or downside swing will be attributed to the holiday period, with more focus on the claims data the following week.

About the Authors

Mike Reid is a Senior U.S. Economist at RBC. He is responsible for generating RBC’s U.S. economic outlook, providing commentary on macro indicators, and producing written analysis around the economic backdrop.

Carrie Freestone is an economist and a member of the macroeconomic analysis group. She is responsible for examining key economic trends including consumer spending, labour markets, GDP, and inflation.

Imri Haggin is an economist at RBC Capital Markets, where he focuses on thematic research. His prior work has centered on consumer credit dynamics and treasury modeling, with an emphasis on leveraging data to understand behavior.

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. The reader is solely liable for any use of the information contained in this document and Royal Bank of Canada (“RBC”) nor any of its affiliates nor any of their respective directors, officers, employees or agents shall be held responsible for any direct or indirect damages arising from the use of this document by the reader. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.

This document may contain forward-looking statements within the meaning of certain securities laws, which are subject to RBC’s caution regarding forward-looking statements. ESG (including climate) metrics, data and other information contained on this website are or may be based on assumptions, estimates and judgements. For cautionary statements relating to the information on this website, refer to the “Caution regarding forward-looking statements” and the “Important notice regarding this document” sections in our latest climate report or sustainability report, available at: https://www.rbc.com/community-social-impact/reporting-performance/index.html. Except as required by law, none of RBC nor any of its affiliates undertake to update any information in this document.