Next week we get quite a bit of soft data – we have several regional Fed surveys on deck (Chicago, Philadelphia, Richmond, and Kansas City) alongside the final University of Michigan Survey of Consumer sentiment data for the month of March. We expect to see significant revisions to inflation expectations in U-Mich because about half of the sample was collected before the start of the war in Iran.

The March preliminary release is based on survey responses collected between February 17th and March 9th. According to U-Mich, about half of the preliminary sample of respondents were interviewed prior to the start of the US military conflict in Iran (which commenced on February 28th). We will be watching all surveys for important clues about inflation expectations in the face of both tariff-driven inflation pressures and the oil price shock. The 1-year inflation expectations are most likely to shift meaningfully higher from the preliminary release.

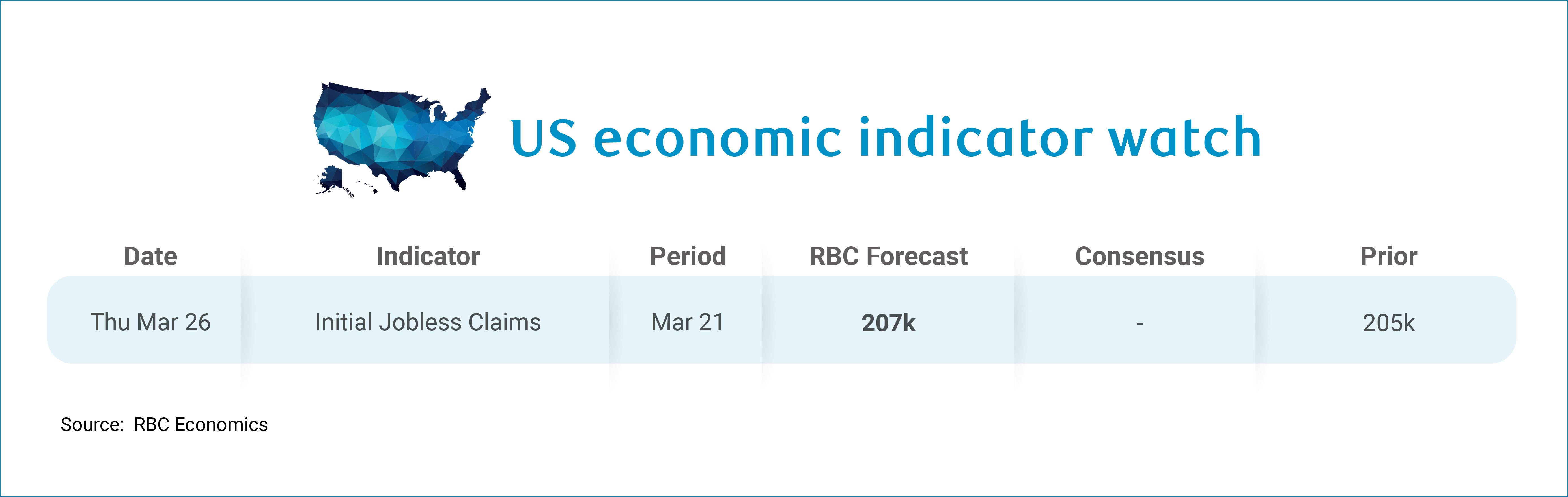

We expect that both the Richmond Fed and Kansas City Fed manufacturing indices will continue to highlight rising prices paid alongside the Philadelphia Fed nonmanufacturing survey. PPI has accelerated the last 4 months, driven by price pressures in transportation and warehousing and wholesaler margins. Those price pressures are being passed through the supply chain, and signal intermediate inputs are becoming more expensive, increasing costs for manufacturers The Kansas City Fed sample is collected over a period of five days from the third Wednesday of the month to the following Monday. The short and recent data collection window means that we can be confident that we are getting real-time perceptions. Both the Richmond Fed manufacturing survey and Philly nonmanufacturing surveys run over slightly longer horizons but still took place during the Iran conflict. Despite the concerns we expect to see in the survey data, we forecast initial jobless claims will hold relatively steady at 207k for the week of March 21st as the uncertainty surrounding current events means the low firing environment is likely to continue.

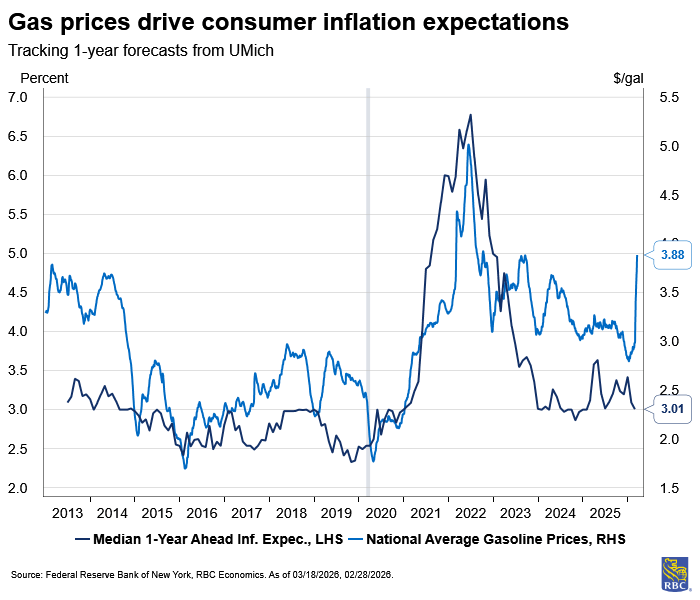

We have written about a relatively new dynamic that central banks are facing globally: central banks are no longer driving the business cycle and are instead reacting to external shocks. Since monetary policy is not the correct tool to address an oil price shock nor tariffs, the appropriate response would be for the Fed to look through these shocks. However, when asked about credibility concerns surrounding looking through both shocks at the March press conference, Chair Powell acknowledged that inflation expectations are top of mind for the Fed, “You worry that that is the kind of thing that can, you know, cause trouble for inflation expectations. And so, we worry a lot about that. You know, we are strongly committed to doing what it takes to keep inflation expectations anchored at 2%.” The challenge that the Fed will face is that the current shock is impacting prices for essentials like gasoline and food, which drastically weigh on consumer perceptions of inflation because they are purchased more frequently, and the price changes are highly visible to consumers. A prolonged conflict risks broadening out the inflationary pressures into other sectors of the economy.

About the Authors

Mike Reid is Head of U.S. Economics at RBC. He is responsible for generating RBC’s U.S. economic outlook, providing commentary on macro indicators, and producing written analysis around the economic backdrop.

Carrie Freestone is a Senior US Economist at RBC Capital Markets. Carrie is responsible for projecting key US indicators including GDP, employment, consumer spending and inflation for the US. She also contributes to commentary surrounding the US economic backdrop which she delivers to clients through publications, presentations, and the media.

Imri Haggin is an Economist at RBC Capital Markets, where he focuses on thematic research. His prior work has centered on consumer credit dynamics and treasury modeling, with an emphasis on leveraging data to understand behavior.

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. The reader is solely liable for any use of the information contained in this document and Royal Bank of Canada (“RBC”) nor any of its affiliates nor any of their respective directors, officers, employees or agents shall be held responsible for any direct or indirect damages arising from the use of this document by the reader. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.

This document may contain forward-looking statements within the meaning of certain securities laws, which are subject to RBC’s caution regarding forward-looking statements. ESG (including climate) metrics, data and other information contained on this website are or may be based on assumptions, estimates and judgements. For cautionary statements relating to the information on this website, refer to the “Caution regarding forward-looking statements” and the “Important notice regarding this document” sections in our latest climate report or sustainability report, available at: https://www.rbc.com/community-social-impact/reporting-performance/index.html. Except as required by law, none of RBC nor any of its affiliates undertake to update any information in this document.