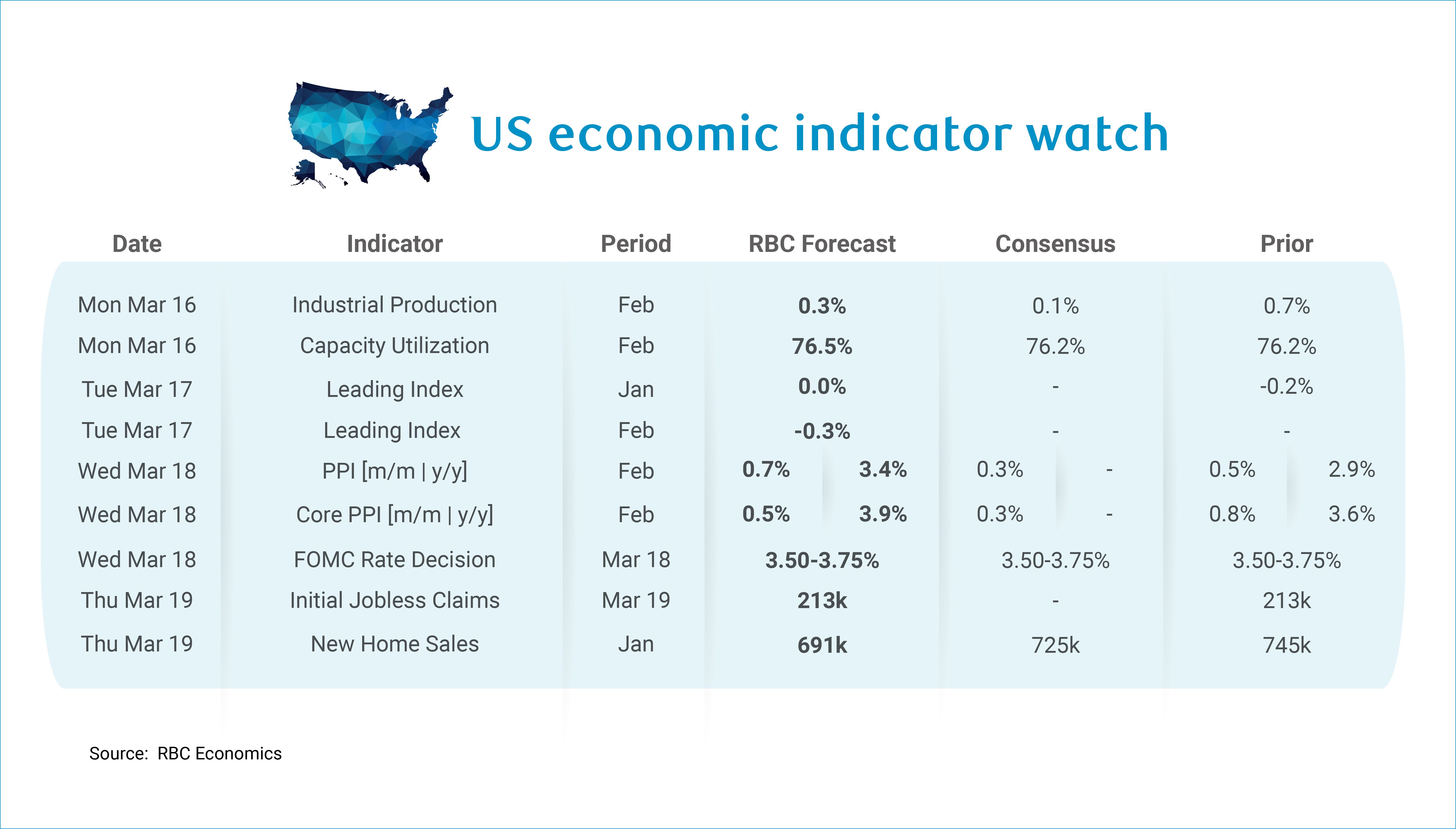

The main event for the week of March 16th is the Fed’s second meeting of 2026 but it is expected to be largely uneventful. We anticipate the Fed will hold rates steady at 3.50-3.75% as they remain on the sidelines keeping an eye on geopolitical developments as well as signs for continued weakness in the labor market.

With an escalating geopolitical crisis in the Middle East, the Strait of Hormuz has been closed. The closure risks fueling energy price spikes that will add to inflation. We have run our own range of estimates, which suggest that if oil lands in the $75 to $100/barrel range for a meaningful duration, inflation would likely settle above 3% y/y.

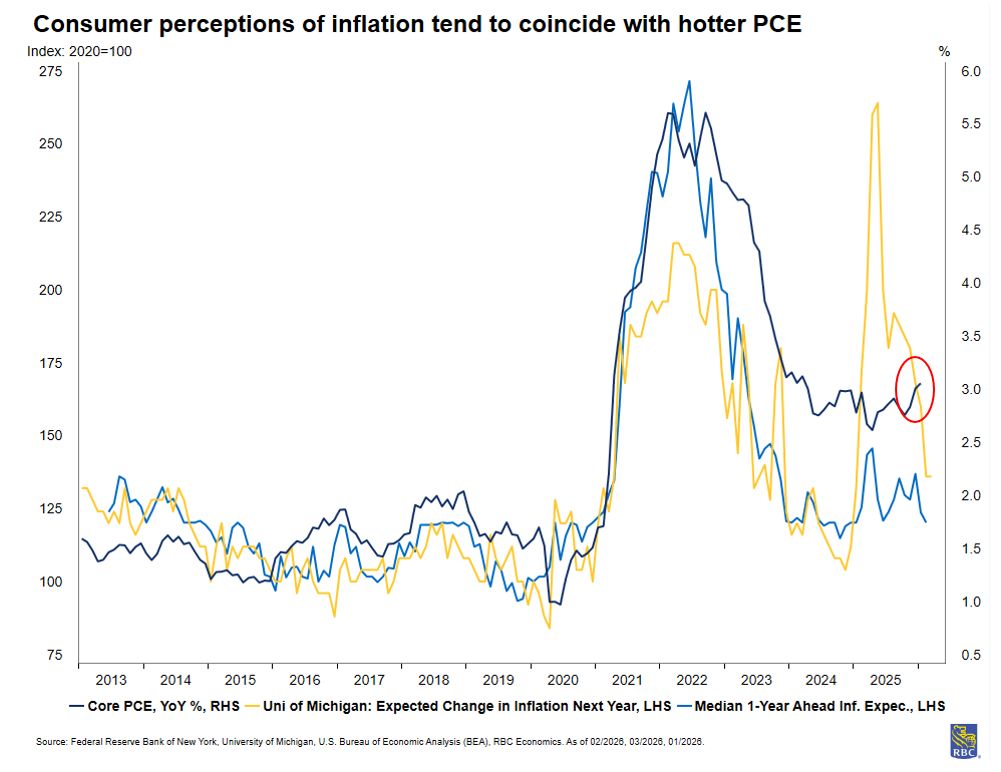

Zooming in on core inflation, the details of the February inflation report were problematic, despite the numbers looking benign on the surface. The core goods sector has been helped by used car prices, and stripping this out, we are seeing a meaningful acceleration driven by trade-exposed sectors, specifically, auto parts, apparel, recreation goods, and personal care products. Pair this with the fact that we see a limited path for disinflation in core services for the remainder of the year, and core inflation has a sticky trajectory. Of growing concern is the pace of core PCE, which accelerated to 3.1% in January, This is the Fed’s preferred measure of inflation and has been diverging from core CPI for several months.

Indeed, monetary policy is not the appropriate tool to combat a tariff shock any more than it is to address an energy shock. What the Fed will be concerned with, however, is inflation expectations rising. And as RBC Rates Strategists, Blake Gwinn and Izaac Brook, have written, “[..]Recent Fed speakers have already emphasized their willingness to look through higher energy prices. But “looking through” doesn’t necessarily mean they will be comfortable cutting into energy-related pressures, and they can’t afford to take anchored expectations for granted.” For now, we expect that the Fed will be increasingly data dependent. The impact of an oil shock exacerbates our “stagflation lite” scenario, putting upward pressure on prices and dampening growth.

Turning to the other side of the Fed’s mandate, it will take time for the oil shock to be demand destructive. US consumers will likely draw down savings or rely on the use of credit before paring back discretionary spending. Still, the longer the oil shock draws out, the more realistic it is to expect a deterioration in real consumer purchasing power. The question remains – is the US labor market positioned to handle the deterioration? And while the February jobs report looked worse from the headlines than it was (-92K jobs were shed, in part due to a nurses’ strike), it did expose a key theme that the US labor market is currently grappling with, which is there is minimal job creation. Thankfully, record retirements will continue to create vacancies for those searching for work, and this should help keep the unemployment rate relatively steady. But as trade-exposed sectors continue to shed jobs (and refrain from backfilling), an energy price shock compounds pre-existing worries.

Aside from the Fed meeting, here is what else we’re watching next week:

-

We expect to see core PPI tick up +0.5% in February. Headline is positioned to outpace core growth (we expect a headline pace of +0.7% m/m), as energy prices spiked at the end of February. We will continue to watch trade services for signs of tariff passthrough, as January data pointed to wider wholesaler margins, suggesting wholesalers are charging retailers higher prices. We will also be monitoring food prices, as the USDA farmers prices paid index suggests pre-existing price pressures coming down the pipeline even before the Strait of Hormuz closer risks pushing up fertilizer costs.

-

Industrial Production is forecast to rise +0.3% m/m in February. This would translate to a capacity utilization rate of 76.5%. Still those expectations should be tempered since manufacturing hours worked held steady in February and the ISM production index slowed.

-

We expect initial jobless claims will hold stay rangebound for the week of March 14th at 213k, as firms maintain a low firing environment. The JOLTS layoff rate has remained exceptionally low and ticked down to 1.0% in January.

-

We continue to expect new home sales activity to remain subdued. Building permits came in below expectations in January as lingering inventory is likely weighing on new builds. We expect new home sales will continue to be sluggish in the months ahead in this high rate environment.

About the Authors

Mike Reid is Head of U.S. Economics at RBC. He is responsible for generating RBC’s U.S. economic outlook, providing commentary on macro indicators, and producing written analysis around the economic backdrop.

Carrie Freestone is a Senior US Economist at RBC Capital Markets. Carrie is responsible for projecting key US indicators including GDP, employment, consumer spending and inflation for the US. She also contributes to commentary surrounding the US economic backdrop which she delivers to clients through publications, presentations, and the media.

Imri Haggin is an Economist at RBC Capital Markets, where he focuses on thematic research. His prior work has centered on consumer credit dynamics and treasury modeling, with an emphasis on leveraging data to understand behavior.

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. The reader is solely liable for any use of the information contained in this document and Royal Bank of Canada (“RBC”) nor any of its affiliates nor any of their respective directors, officers, employees or agents shall be held responsible for any direct or indirect damages arising from the use of this document by the reader. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.

This document may contain forward-looking statements within the meaning of certain securities laws, which are subject to RBC’s caution regarding forward-looking statements. ESG (including climate) metrics, data and other information contained on this website are or may be based on assumptions, estimates and judgements. For cautionary statements relating to the information on this website, refer to the “Caution regarding forward-looking statements” and the “Important notice regarding this document” sections in our latest climate report or sustainability report, available at: https://www.rbc.com/community-social-impact/reporting-performance/index.html. Except as required by law, none of RBC nor any of its affiliates undertake to update any information in this document.