Bottom line:

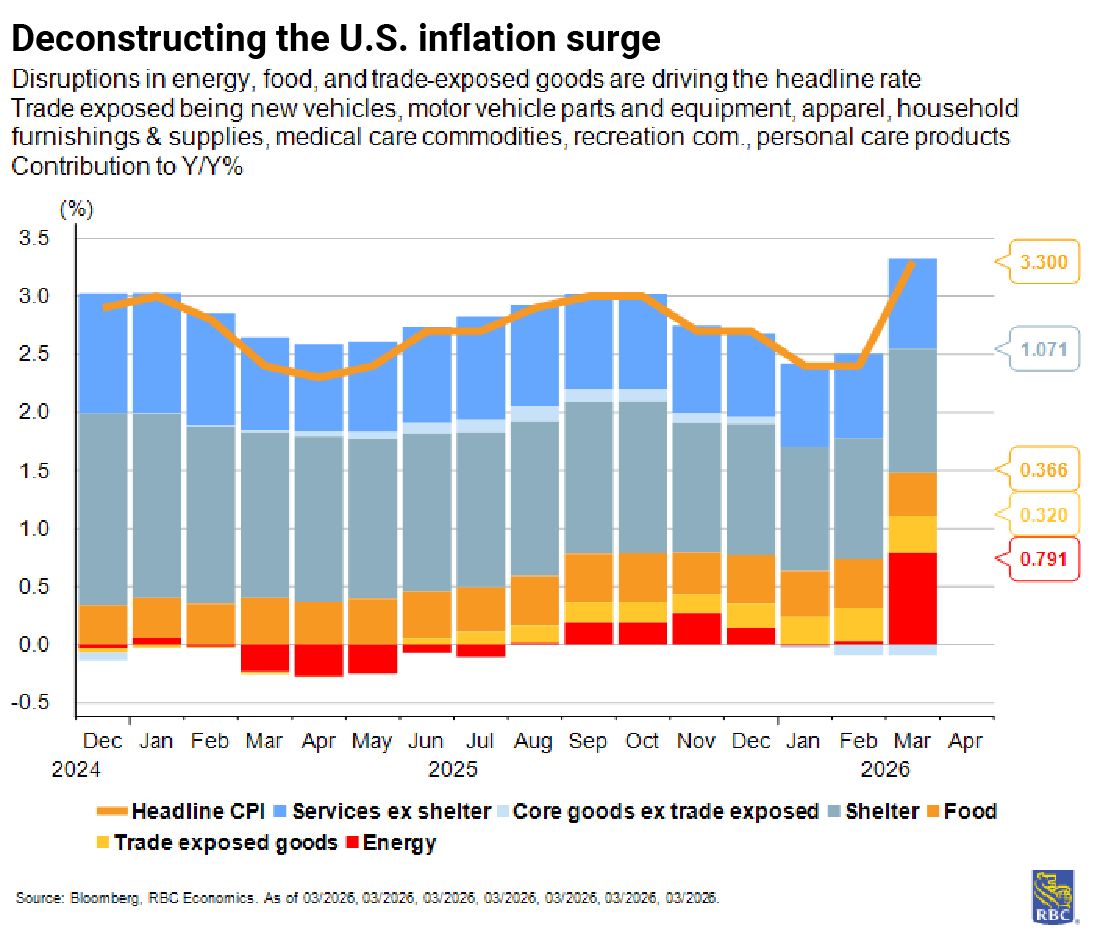

Higher gas prices sent headline inflation soaring in March as the monthly rise (+0.9% m/m) was reminiscent of 1970s inflation. The silver lining is core inflation remained subdued, rising a modest +0.2% m/m. The continued slowdown in core inflation will provide some term relief for the Fed. But the risk remains that higher energy prices could start to spill over into the broader economy if the conflict in the Middle East persists. Higher oil risks pushing transport costs up and continued tariff effects are layering additional pressure onto core goods. As we’ve been highlighting, prices for trade exposed sectors, including auto parts, apparel, personal and recreational goods continued to rise at an uncomfortable pace. For the Fed, the question remains how businesses will react to the oil price shock: will they continue to pass on higher prices to consumers or will they protect margin compression through layoffs? For now, the Fed will have to remain data dependent before they decide their next move.

There are 3 core themes that stood out in today’s report:

I. Even if the Fed is not focused on headline, higher energy prices will hurt consumers

As expected, motor fuel prices posted a massive spike in March (+21.5% m/m). And higher fuel prices translated to a spike in airfares in March (+2.7% m/m). Energy commodities and services added close to 0.8 percentage point to the overall index. While the Fed is more focused on core inflation, spikes in gasoline prices influence consumer inflation expectations. Persistently elevated gas prices could ultimately be a problem for wage expectations, and the duration of the shock will matter.

If the oil price shock persists (weighing on fertilizer prices and transportation costs), we would expect to see core goods pressures heat up from higher input costs at the same time that tariff passthrough peaks (later this year). We are already seeing spikes in wholesaler margins in PPI, declining corporate profits in trade-exposed sectors, and now, a spike in manufacturers’ prices paid (as reflected in the March ISM data).

II. Tariff pressures are continuing to show up in core goods inflation

In March, core goods (+0.11% m/m) was modest, but similar to last month, this is a story of used motor vehicle prices masking tariff passthrough. Here’s what we saw in trade-exposed sectors:

-

Apparel prices continued to climb reporting m/m price growth exceeding 1% for the second consecutive month. Spikes in PPI trade services in recent months suggest wholesalers are passing off higher prices to retailers.

-

Motor vehicle parts and equipment continued to run hot (+0.7% m/m) but this has yet to translate to higher new motor vehicle prices (+0.1% m/m).

-

Recreation commodities (+0.5%) and personal care products (+0.4%) also rose meaningfully for the third consecutive month.

-

Interestingly, prices for household furnishings and supplies (-0.2% m/m) cooled in March – a reprieve after a few hotter months.

III. We are still seeing a stark divide between core CPI and PCE prints

This March core inflation print – at 2.6% y/y – is notably lower than core PCE for February (+3.0% y/y). Differences in weighting between CPI and PCE baskets are the culprit. Shelter bears more weight in CPI and has been relatively benign in recent months (OER rose +0.3% in March and rents +0.2%). But methodological quirks associated with the BLS’s handling of missing October shelter data means that shelter CPI could be bumpy in the April data.

Our own diffusion index pointed to accelerating price pressures. In March, 50% of CPI basket items reported price growth >3% after a moderation in January and February.

About the authors:

Mike Reid is Head of US Economics at RBC. He is responsible for generating RBC’s US economic outlook, providing commentary on macro indicators, and producing written analysis around the economic backdrop.

Carrie Freestone is a Senior US Economist at RBC. Carrie is responsible for projecting key US indicators including GDP, employment, consumer spending and inflation for the US. She also contributes to commentary surrounding the US economic backdrop which she delivers to clients through publications, presentations, and the media.

Imri Haggin is an US Economist at RBC, where he focuses on thematic research. His prior work has centered on consumer credit dynamics and treasury modeling, with an emphasis on leveraging data to understand behavior.

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. The reader is solely liable for any use of the information contained in this document and Royal Bank of Canada (“RBC”) nor any of its affiliates nor any of their respective directors, officers, employees or agents shall be held responsible for any direct or indirect damages arising from the use of this document by the reader. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.

This document may contain forward-looking statements within the meaning of certain securities laws, which are subject to RBC’s caution regarding forward-looking statements. ESG (including climate) metrics, data and other information contained on this website are or may be based on assumptions, estimates and judgements. For cautionary statements relating to the information on this website, refer to the “Caution regarding forward-looking statements” and the “Important notice regarding this document” sections in our latest climate report or sustainability report, available at: https://www.rbc.com/community-social-impact/reporting-performance/index.html. Except as required by law, none of RBC nor any of its affiliates undertake to update any information in this document.