As was widely expected, the Federal Reserve remained on pause at the March meeting. Indeed, the importance of this meeting was not about the rate decision itself, but the opportunity to gain insight into how the Fed is thinking about (and outwardly characterizing) the growing risks resulting from the conflict in the Middle East. We saw this in both the SEP adjustments to inflation and growth as well as the language used to describe the geopolitical backdrop and its impact on the US economy. On top of this, we continue to see tariff pressures materialize. The oil price shock is adding another layer of uncertainty in terms of inflation and growth. Still, there is little that the Fed can do to combat an oil price shock other than to wait and see. As Chair Powell himself acknowledged at the press conference:

“I want to emphasize, nobody knows, the economic effects could be smaller or much bigger. We just don’t know.”

At the same time, concerns around demand destruction and job losses are top of mind. As risks mount on both sides of the mandate, we continue expect that the Fed will remain on pause and shift back towards a data dependent approach in the months ahead while they continue to monitor the trajectory of the US economy.

“We also think it is important, though, to keep policy mildly restrictive or close to that… We’re balancing the two goals in a situation where the risks to the labor market or downside…would call for lower rates and the risks to inflation are to the upside or higher rates.”

The lack of progress on inflation was already a concern prior to the oil price shock

We are seeing evidence of tariff pressures materializing in several inflation metrics. We have seen a notable acceleration in PPI, driven by the trade-exposed sectors (reflective of wholesalers raising prices that they are charging to retailers) since December. The next stage involves retailers passing off higher prices to consumers, and we expect the full extent of the passthrough will come in the months ahead. From there, Powell reiterated that the runoff process can take several months to a year to go through the system, reflecting the Fed’s view that inflation is unlikely to return to the 2% target by 2027. Outside of the goods space, non-housing services inflation has been another point of concern. We think much of that inflationary pressure can be traced to a tight labor market. Powell acknowledged that the Fed’s expectations for nonhousing services deflation are not aligned to what the data is showing. And in that lens, it could take a more notable slowdown in hiring for the labor market to see wage growth slow. Indeed, other factors are at play, including a shifting consumer base – one that is growing older and demanding more services (i.e., health, legal, financial, etc.) over goods. We think the impact retirements are having on the labor market and consumption has been underappreciated.

“It is frustrating. Nonhousing services have basically moved sideways for a year… We expect they’ll come down. Stay bunch of idiosyncratic things. At the same time that is something we should see…the labor market is clearly not a source of inflationary pressures. That should matter for nonhousing services. We’re not seeing progress there.”

Meanwhile the lack of job creation is not a comfortable trend

For now, the labor backdrop is looking relatively stable. Jobless claims have settled at low levels and the unemployment rate has remained largely unchanged since September. While a sizeable decline in February payrolls can be partially attributed to a nurse’s strike (the effects of which will be mechanically reversed next month), it exposed a key theme in the US labor market which is job creation in the US labor market is being driven by structural growth while cyclically-exposed sectors are shrinking. The upshot is, the Fed does view the labor market as being near equilibrium – meaning the break even pace of job growth is near zero. But Powell expressed concern that the balance is sitting on a shaky foundation:

“Effectively there is zero net job creation in the private sector. Actually that looks like that is about what the economy needs in terms of dealing with very low nonexistent growth in the labor force. Which we never had in our history…Now, that is balance…but I would say it does have a feel of downside risk.”

FOMC is no longer in the driver’s seat and will be data dependent in 2026

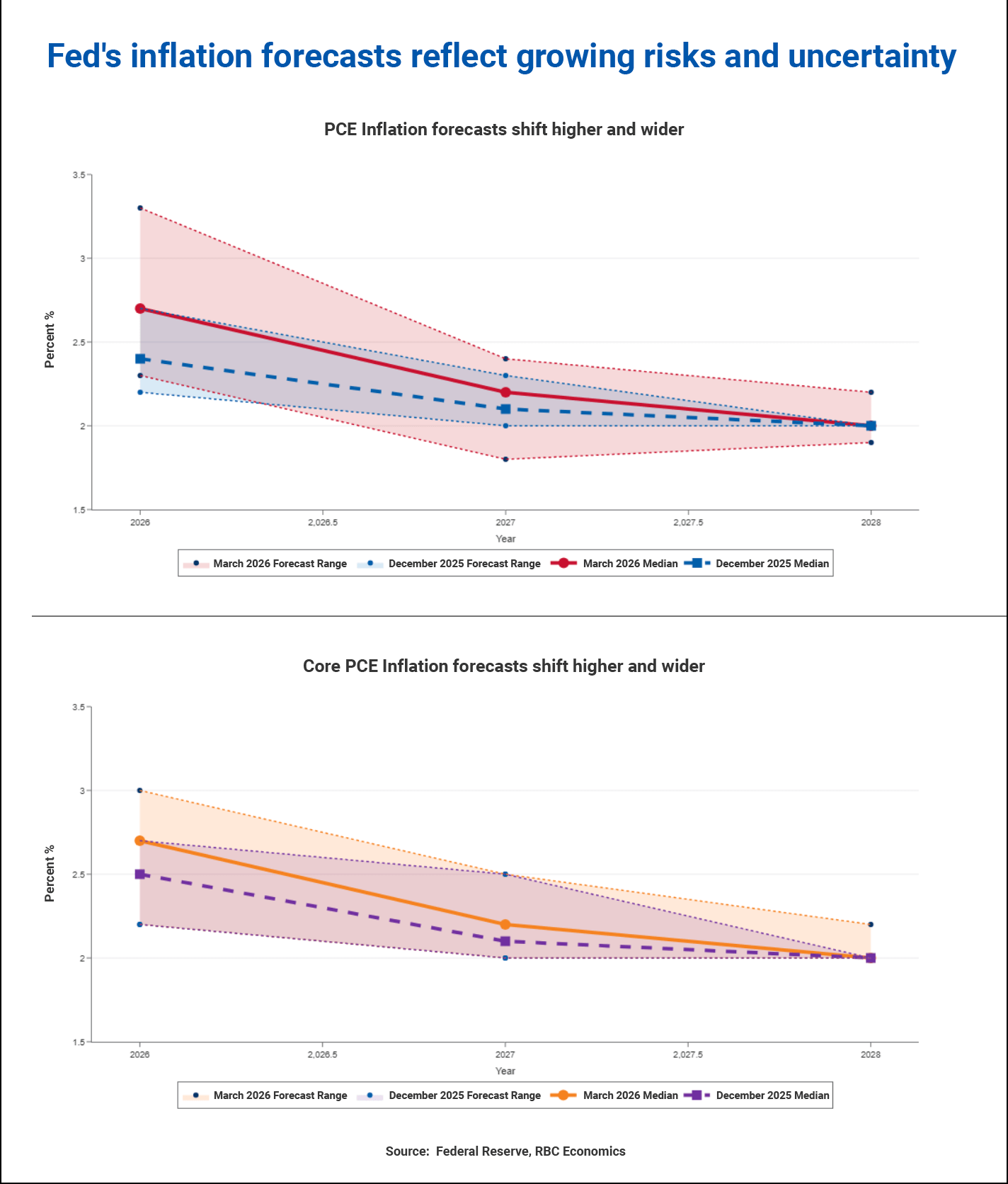

Changes to the Summary of Economic Projections (SEP) showed upgrades to the 2026 outlook relative to the December SEP. As expected, there was a material adjustment to PCE inflation. The median projections for both core (+0.2 ppt) and headline (+0.3 ppt) inflation were revised higher to 2.7% for 2026. Interestingly, GDP growth was revised up (+0.1 ppt) to 2.4% for 2026 and (+0.3 ppt) to 2.3% for 2027 while the unemployment rate was mostly unchanged. Despite these changes, the median number of interest rate cuts for 2026 as indicated by the Dot Plot remained unchanged and still assumes one additional 25 basis point cut (as implied by a Fed Funds target rate of 3.4%). While we can appreciate the SEP materials are reflective of several views, it continues to reflect a view that the Fed will be more sympathetic to the risks to the labor market, especially if they become non-linear. Still, as is typical, Chair Powell remained non-committal as to which side of the mandate would bear more weight, reflecting the uncertainty facing the economy.

In many ways, the Fed’s influence on the economy is increasingly being handcuffed by the confluence of court rulings, geopolitical events, price shocks, and data distortions. This reflects the increasingly evident dynamic that central banks are no longer driving the business cycle and instead reacting to external shocks. This is a relatively new dynamic for markets, and one that the Fed will have to contend with in the year ahead. And it further solidifies our stance that the Fed will remain in wait-and-see mode.

About the authors:

Mike Reid is Head of U.S. Economics at RBC. He is responsible for generating RBC’s U.S. economic outlook, providing commentary on macro indicators, and producing written analysis around the economic backdrop.

Carrie Freestone is a Senior Economist and a member of the macroeconomic analysis group. She is responsible for examining key economic trends including consumer spending, labour markets, GDP, and inflation.

Imri Haggin is an Economist at RBC Capital Markets, where he focuses on thematic research. His prior work has centered on consumer credit dynamics and treasury modeling, with an emphasis on leveraging data to understand behavior.

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. The reader is solely liable for any use of the information contained in this document and Royal Bank of Canada (“RBC”) nor any of its affiliates nor any of their respective directors, officers, employees or agents shall be held responsible for any direct or indirect damages arising from the use of this document by the reader. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.

This document may contain forward-looking statements within the meaning of certain securities laws, which are subject to RBC’s caution regarding forward-looking statements. ESG (including climate) metrics, data and other information contained on this website are or may be based on assumptions, estimates and judgements. For cautionary statements relating to the information on this website, refer to the “Caution regarding forward-looking statements” and the “Important notice regarding this document” sections in our latest climate report or sustainability report, available at: https://www.rbc.com/community-social-impact/reporting-performance/index.html. Except as required by law, none of RBC nor any of its affiliates undertake to update any information in this document.