-

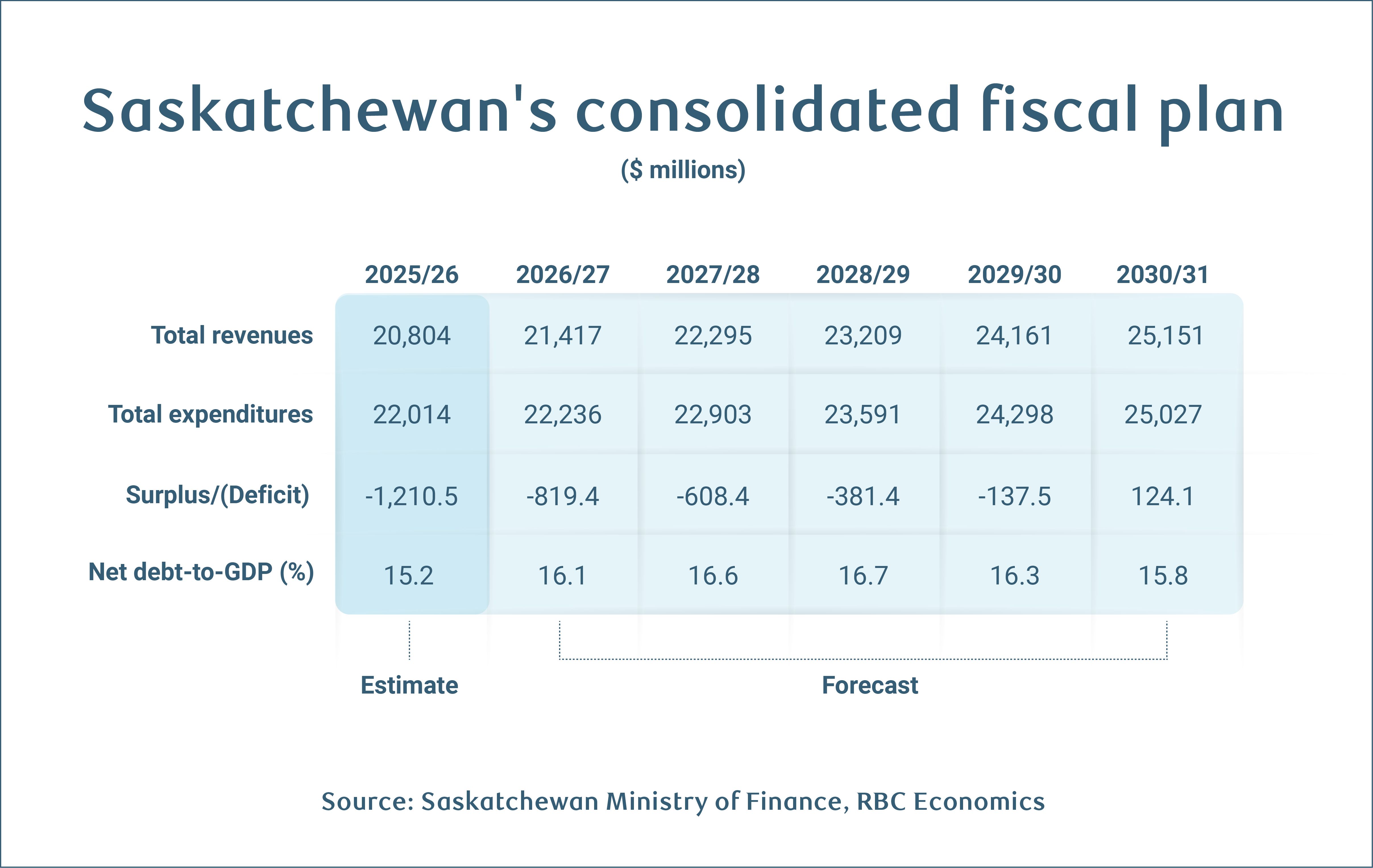

Saskatchewan’s strong fiscal position took a hit in 2025-26, with a $1.2 billion deficit (1% of GDP) now expected instead of a $12 million surplus originally budgeted.

-

Budget 2026 projects the deficit to narrow to $819 million (0.7% of GDP) in 2026-27 mainly thanks to slower spending growth.

-

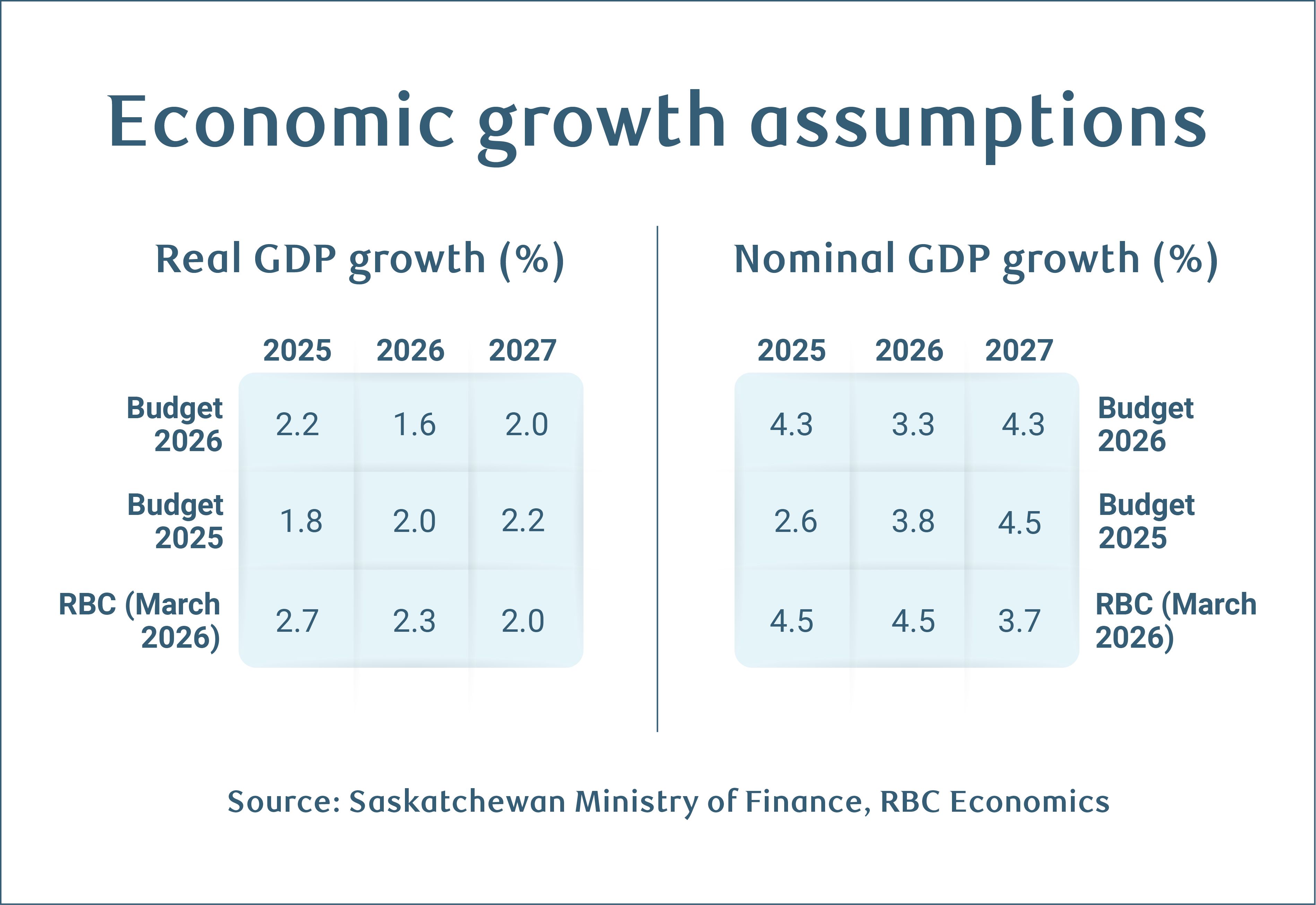

The economic assumptions underpinning Budget 2026 look conservative in light of the recent spike in oil prices, offering material revenue upside.

-

Saskatchewan is one of the few provinces with a plan to balance its book and set its debt load on a downtrend.

Saskatchewan’s 2026 budget projections mark a deterioration from last year’s fiscal path—a common trend among provinces that have reported to date.

The outlook for revenues are downgraded through the entire fiscal plan while expenditures are revised higher. This results in deficits in the next four years—which contrasts with the steady (small) surpluses Budget 2025 projected.

The turning point occurred in the fiscal year that will end on March 31st, which is now on track for a $1.2 billion deficit—a far cry from the modest $12 million surplus projected in Budget 2025 and $427 million deficit expected in November’s mid-year update.

This deterioration is unsurprising given the government’s decision to exclude a contingency fund from last year’s fiscal plan despite acknowledged trade policy uncertainty. Though trade disruptions proved less severe than initially feared, the absence of that buffer left the province exposed to unplanned spending or revenue hit. Health and protection of persons and property expenditures alone account for nearly half of the $449 million in added costs since the mid-year update—including a $141 million increase in healthcare to address utilization pressures across the system and an additional $52 million to address wildfire and evacuation activities.

Saskatchewan’s government now charts out a path to balance by fiscal 2030-31— a commitment that distinguishes it from most other provinces that released their 2026 budget. While the timeline is well into the future, the detailed map to balance is noteworthy nonetheless.

Conservative commodity assumptions add upside to revenues

Revenues for 2026-27 are projected to grow $613 million from fiscal 2025-26, lead by increases from taxation, federal transfers, and government business enterprises. Total revenues are now expected to come in at $21.4 billion—which is still a solid increase in percentage terms (2.9%) compared to the last three years (averaging 0.7%).

Non-renewable resources are projected to fall $125 million (-4.6%), on the assumption that uranium production will fall modestly and the WTI oil price benchmark will ease to US$59.75 per barrel in 2026 from US$61.69 in 2025. The latter assumption appears overly soft given WTI prices have surged above US$90 per barrel since the Iran war began and are likely to stay high for several more months.

Movements in commodity prices can meaningfully affect the province’s fiscal position. A US$1 per barrel change in WTI prices is estimated to shift oil revenues by $16 million. Should oil prices stay above US$70 per barrel on a sustained basis, total revenues could increase by more than $160 million over the 2026-27 baseline revenue projection. All else equal, that could shrink the deficit by ~20%.

Expenditures poised for little growth following one-time health and evacuation expenses

Expenditures are on a tight track, poised to grow just 1% from fiscal 2025-26 to $22 billion.

The budget’s central theme—”Protecting Saskatchewan”—emphasizes maintenance of government programs and services while avoiding tax increases. Under normal circumstances, we would be skeptical of achieving both simultaneously without adding risk to higher deficits. The recent oil price shock has already prompted an upward adjustment to our inflation forecast, which would make the 1% expenditure target difficult to hit—even with stalled population growth.

However, the prior year’s spike in expenditures from one-off wildfires and elevated healthcare costs—the latter unlikely to recur at the same magnitude given slowing population growth—makes the 1% expenditure growth target achievable, barring another severe wildfire season.

Debt load to peak higher

Saskatchewan’s net debt-to-GDP ratio will continue rising over most of the fiscal plan—peaking at 16.7% in 2028-29—after which, its expected to resume its downward trajectory.

Saskatchewan is the second-least indebted province after Alberta and is positioned to maintain that standing despite an upwardly revised debt trajectory over the fiscal plan period.

The relatively strong financial footing affords the government meaningful room to address emerging challenges—like trade-related headwinds and unexpected evacuation costs—without resorting to sweeping cuts to core services. Budget 2026 bears this out. Upside revenue risk could also limit the near-term erosion in the province’s fiscal position.

About the author:

Rachel Battaglia is an Economist at RBC, providing forecasts for the Canadian provincial economies and analyzing key trends in housing and consumer spending.

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. The reader is solely liable for any use of the information contained in this document and Royal Bank of Canada (“RBC”) nor any of its affiliates nor any of their respective directors, officers, employees or agents shall be held responsible for any direct or indirect damages arising from the use of this document by the reader. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.

This document may contain forward-looking statements within the meaning of certain securities laws, which are subject to RBC’s caution regarding forward-looking statements. ESG (including climate) metrics, data and other information contained on this website are or may be based on assumptions, estimates and judgements. For cautionary statements relating to the information on this website, refer to the “Caution regarding forward-looking statements” and the “Important notice regarding this document” sections in our latest climate report or sustainability report, available at: https://www.rbc.com/community-social-impact/reporting-performance/index.html. Except as required by law, none of RBC nor any of its affiliates undertake to update any information in this document.