-

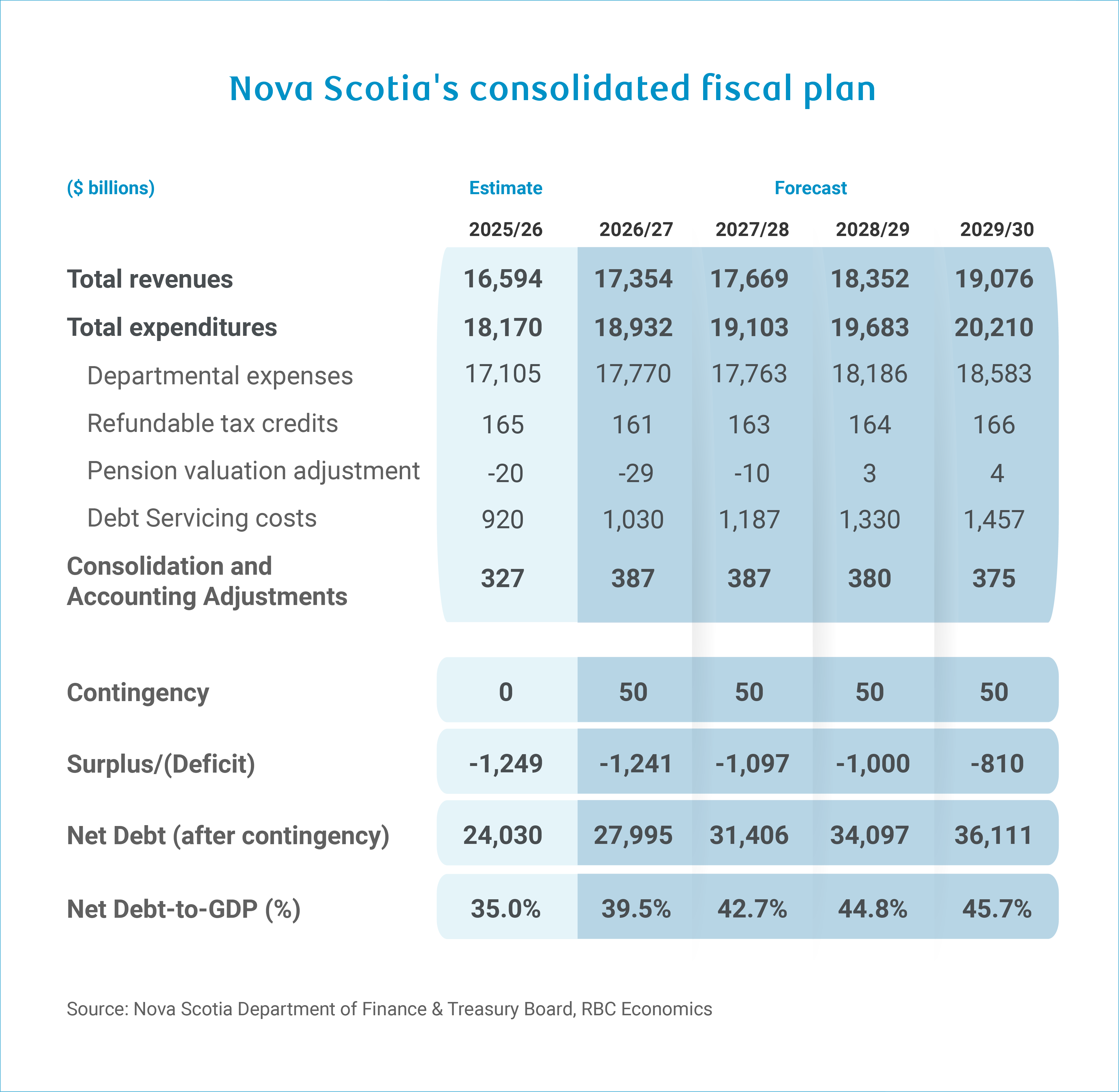

Nova Scotia projects a $1.24 billion deficit for 2026–27 that will remain above $1 billion through 2028–29, a stark shift from last year’s deficit reduction plan.

-

Spending pressures remain despite cuts to public service.

-

Revenues are recuperating from the soft performance in fiscal 2025-26, but not enough to materially shrink the deficit.

-

The debt-to-GDP ratio will breach the government’s 40% guardrail by 2027–28 and climb to 45.7% by 2029–30.

Nova Scotia’s fiscal trajectory has fundamentally shifted—and it’s taking the government on a long detour towards balancing the books. Budget 2026–27 projects a $1.24 billion deficit that will persist above $1 billion through 2028–29, a notable departure from the sharper deficit reduction path charted just one year ago that was projected to culminate in a deficit one-fifth of the billion-dollar shortfall now projected by 2028-29.

The divergence stems from spending pressures that have intensified across multiple fronts in 2025-26—like healthcare, education, and restructuring costs tied to public service downsizing–which put the province in a worse starting point for 2026-27. Program expenditures are now expected to increase 4.2% in 2026-27, following an outsized 7.2% increase in the year prior.

Revenues are estimated to contract in 2025-26 on tax cuts and economic weakness—and barely outpace spending growth in 2026-27. As a result, the province’s net debt-to-GDP ratio is approaching its self-imposed 40% guardrail and is expected to breach it by fiscal 2027-28, with further deterioration thereafter.

Public sector cuts won’t close the gap on their own

The $1.24 billion deficit for 2026–27 is $518 million larger than the previous year’s forecast—a gap that has blown open in just twelve months due to high expenditures and soft revenues.

Despite some cuts, total expenditures are projected to continue rising in 2026-27 (4.2%) driven by increases for Health and Wellness (up 6% to $6.7 billion)—reflecting higher staffing, facility, and supply costs. Seniors and Long-term Care and Education were other notable spending pressures, reflecting aging demographics and lunch programs for students.

The government has embedded significant public sector headcount reductions as a cornerstone of fiscal stabilization, targeting $914.3 million in cumulative savings by 2029–30. Still, departmental expenses will continue to outpace population growth and inflation at 3.9% in 2026–27, despite the reductions.

Though revenue growth is projected to accelerate to 4.6%, it won’t materially narrow the fiscal hole. Revenue generated from personal income tax is expected to gain momentum in 2026–27 after last year’s tax cuts and weak economic conditions caused revenues to fall.

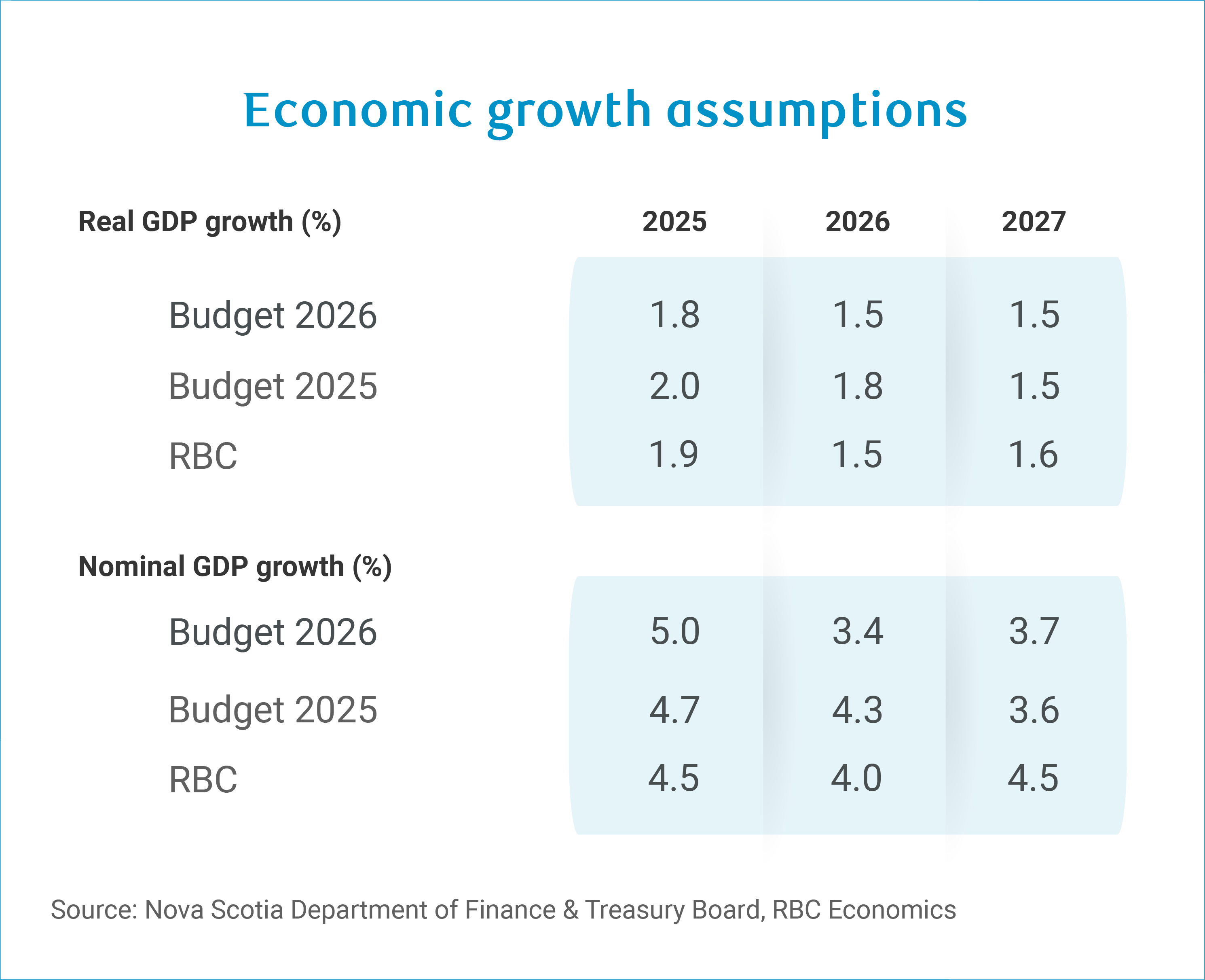

Conservative economic growth assumptions among the few prudence measures

Budget projections are based on conservative economic assumptions. The government expects nominal GDP to expand by 3.4% in 2026, lower than RBC Economics’ projection of 4%.

Added to an annual $50 million contingency reserve fund, they provide some cushion against unforeseen shocks—a prudent safeguard in such times of economic uncertainty.

Spending more on debt servicing

Net debt is projected to reach $28 billion in 2026–27 and $36 billion by 2029–30. The net debt-to-GDP ratio will breach the government’s 40% guardrail by 2027–28 and continue climbing to 45.7% by 2029–30.

Debt servicing costs are expected to rise from 5.5% of revenues in 2025–26 to 7.6% by 2029–30. Interest payments will consume an ever-larger share of provincial revenues that won’t be available for schools, healthcare, and emergency response.

About the author

Rachel Battaglia is an economist at RBC. She is a member of the Macro and Regional Analysis Group, providing analysis for the provincial macroeconomic outlook.

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. The reader is solely liable for any use of the information contained in this document and Royal Bank of Canada (“RBC”) nor any of its affiliates nor any of their respective directors, officers, employees or agents shall be held responsible for any direct or indirect damages arising from the use of this document by the reader. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.

This document may contain forward-looking statements within the meaning of certain securities laws, which are subject to RBC’s caution regarding forward-looking statements. ESG (including climate) metrics, data and other information contained on this website are or may be based on assumptions, estimates and judgements. For cautionary statements relating to the information on this website, refer to the “Caution regarding forward-looking statements” and the “Important notice regarding this document” sections in our latest climate report or sustainability report, available at: https://www.rbc.com/community-social-impact/reporting-performance/index.html. Except as required by law, none of RBC nor any of its affiliates undertake to update any information in this document.