-

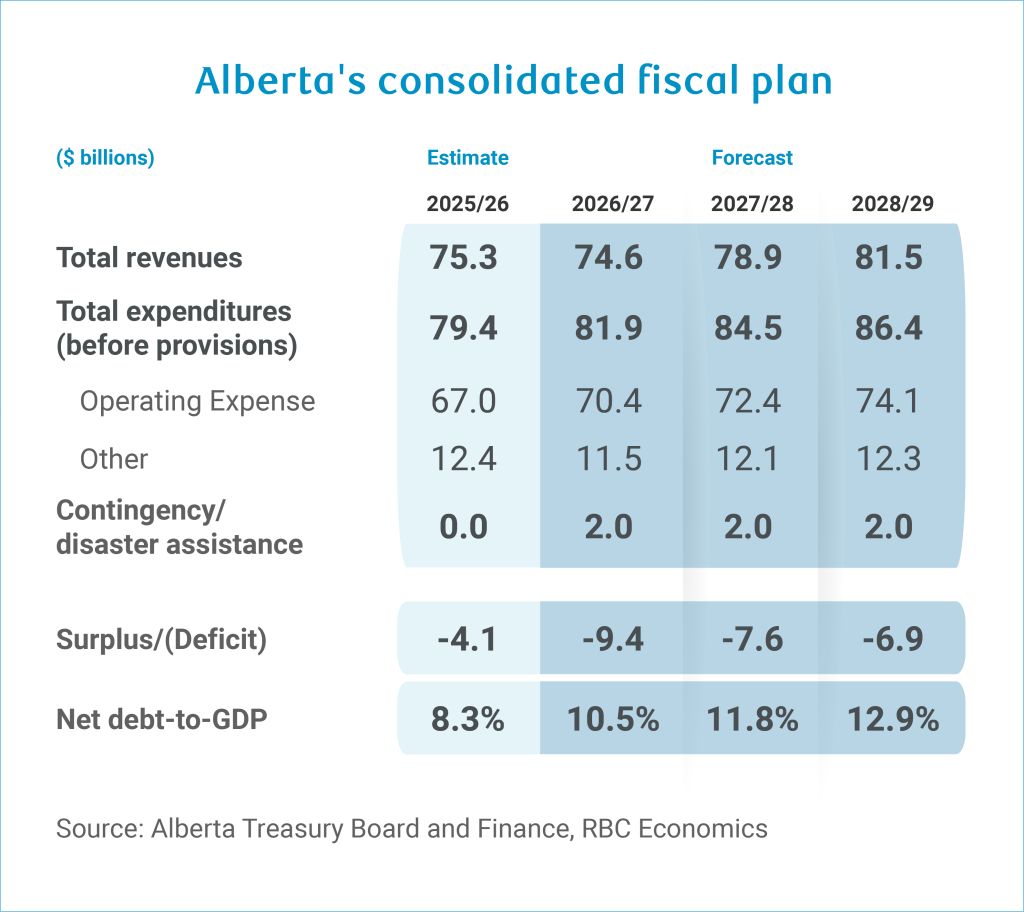

The Alberta government projects a $9.4 billion deficit in fiscal 2026-27, more than double the $4.1 billion shortfall now estimated for 2025-26.

-

Revenues to shrink in fiscal 2026-27 on lower resource royalties.

-

Balanced budget framework was temporarily suspended, with the government showing deficits over the entire the fiscal plan.

-

Net debt-to-GDP ratio will remain on an incline over the course of the fiscal plan, reaching 12.9% by 2028-29—the highest since the pandemic but still by far the lowest among the provinces.

Budget 2026 confirmed the fiscal pressures that have built in the last year, revealing a sizable increase to the 2026-27 deficit from Budget 2025’s projection. The government has temporarily stepped back from the balanced-budget framework that guided previous fiscal plans and now projects deficits to run through to fiscal 2028-29, including a substantial $9.4 billion shortfall in 2026-27.

While legislation permits deficits under certain circumstances, it also requires a return to balance within three years of reporting a deficit. The current revenue situation does not technically meet the legislated threshold for invoking deficit provisions—which requires a minimum $1 billion revenue decline.

An outsized 7.1% increase in total expense in 2025-26 set the province on a higher expenditure trajectory in 2026-27.Health and education expenses will continue to rise rapidly (by 6% and 8.1%, respectively in 2026-27), driven by population-related service demand, clinical complexity, and hefty public sector compensation settlements. These costs are expected to grow briskly again in 2027-28 but moderate by 2028-29.

Compounding this strain will be contracting revenues in 2026-27. Weak oil prices are expected to reduce bitumen royalties by $3 billion, while the drop in personal income taxation in the prior fiscal year set a lower baseline for 2026-27.

We warned of material fiscal deterioration last year when Budget 2025 introduced tax cuts ahead of schedule despite a weakening oil price forecast and the uncertain trade environment.

Revenues to contract on weak oil prices

Total revenue in 2026-27 is forecast at $74.6 billion, down $700 million (-1%) from the 2025-26 estimate.

Non-renewable resource revenue is the primary culprit. Bitumen royalties are forecast to plummet to $9.7 billion in 2026-27, a $3.0 billion (24%) drop from 2025-26 and a loss of more than 40% from 2024-25.

The falls comes as the benchmark WTI price is forecast to reach a low point of $60.50 USD per barrel, down from $61.50 USD per barrel in 2025-26 and far below the $71 USD per barrel assumed in last year’s budget. The light-heavy crude differential is expected to widen to $13 USD per barrel as oversupply weighs on global markets.

The government’s oil price assumption is grounded in the current market consensus but leaves minimal room for downside surprises. While the 2026 oil price forecast is only marginally higher than our own, the oil price forecast in 2027 departs more meaningfully from ours and is nearly 10% above the $60.50 USD per barrel of consensus.

Operating pressure without offset

Total expenditures (before contingencies) are set to rise $2.5 billion (3.1%) year-over-year from 2025-26, fuelled by increases to operating expenses.

Health and education are taking centre stage, with health spending rising $1.8 billion year-over-year (6%) in 2026-27, while education expense grows $959 million (8.1%). Meantime, debt servicing costs will jump $485 million to $3.4 billion.

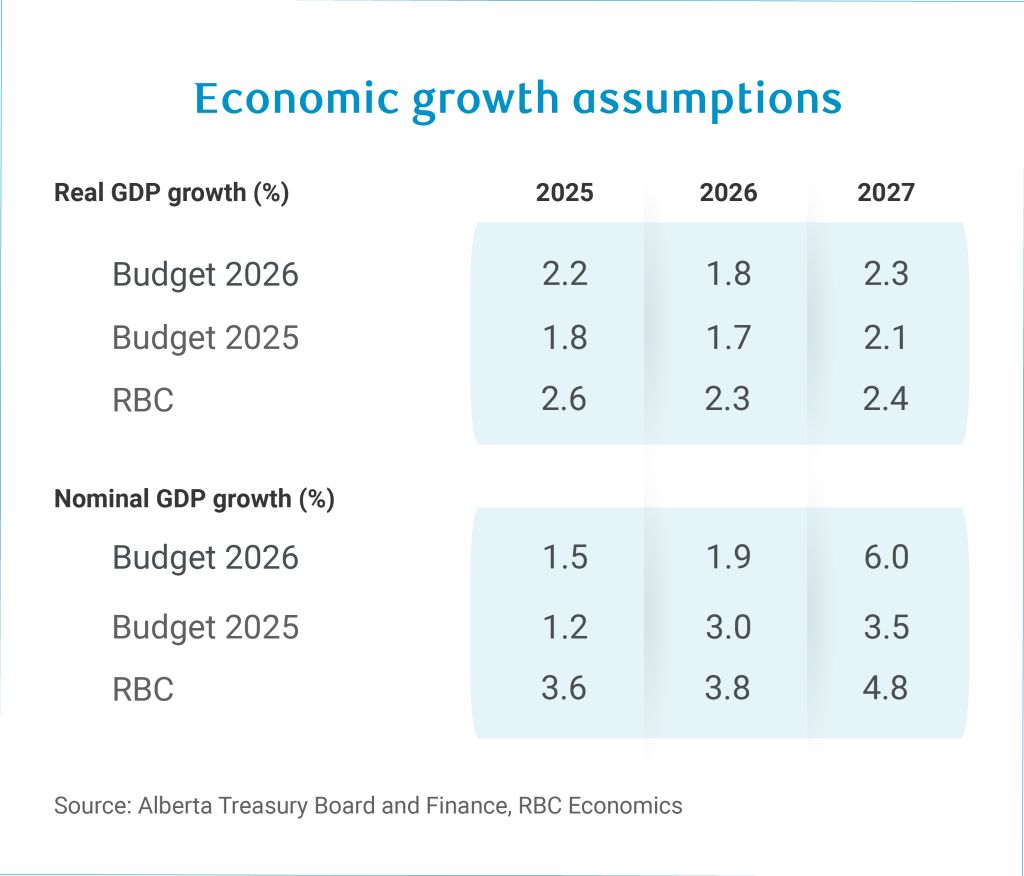

Growth assumptions offer near-term prudence, but risks beyond this year

The government’s economic assumptions for 2026-27 appear prudent. Nominal GDP growth of 1.9% in 2026 is considerably lower than our (3.8%), assuming little change in US tariffs and population growth hovers just over 1%.

That said, the subsequent year warrants some scrutiny. Like the WTI forecast, our expectations for a rebound are more muted than the assumptions underpinning the outer years of the fiscal plan.

The budget projects nominal GDP growth to accelerate to 6% in 2027-28, driven by investments in infrastructure, clean energy, and pipeline expansions alongside stronger U.S. growth and a recovery in WTI prices. Should these rebounds materialize more slowly than projected, the revenue recovery embedded in the medium-term forecasts could fall materially short—extending the deficit period beyond current projections.

Deficits put debt burden on an upward trajectory

Budget 2026 marks a departure from the commitment to keep Alberta’s net debt-to-GDP ratio on a downward path. The debt burden is now expected to climb to 12.9% by 2028-29, the highest level since the pandemic, up from 7.2 per cent in 2024-25.

We’ve long recognized Alberta’s strong fiscal standing relative to other provinces—and this continues to be the case—but its fiscal advantage is eroding. Wide swings in non-renewable resource revenues over which the province has little control tend to exacerbate cyclical budgetary challenges. Greater revenue diversification would help temper such volatility and protect the province’s advantageous fiscal position.

About the author

Rachel Battaglia is an economist at RBC. She is a member of the Macro and Regional Analysis Group, providing analysis for the provincial macroeconomic outlook.

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. The reader is solely liable for any use of the information contained in this document and Royal Bank of Canada (“RBC”) nor any of its affiliates nor any of their respective directors, officers, employees or agents shall be held responsible for any direct or indirect damages arising from the use of this document by the reader. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.

This document may contain forward-looking statements within the meaning of certain securities laws, which are subject to RBC’s caution regarding forward-looking statements. ESG (including climate) metrics, data and other information contained on this website are or may be based on assumptions, estimates and judgements. For cautionary statements relating to the information on this website, refer to the “Caution regarding forward-looking statements” and the “Important notice regarding this document” sections in our latest climate report or sustainability report, available at: https://www.rbc.com/community-social-impact/reporting-performance/index.html. Except as required by law, none of RBC nor any of its affiliates undertake to update any information in this document.