Travel by Canadians is not weakening—but it is being redirected.

A sustained pullback in trips to the United States is increasingly being offset by rising travel to other destinations within Canada as well as abroad.

The result is a rebalancing in the industry where Canadians are spending more travel dollars within the country, supporting domestic tourism.

The decline in travel to the U.S. has been both sharp and persistent.

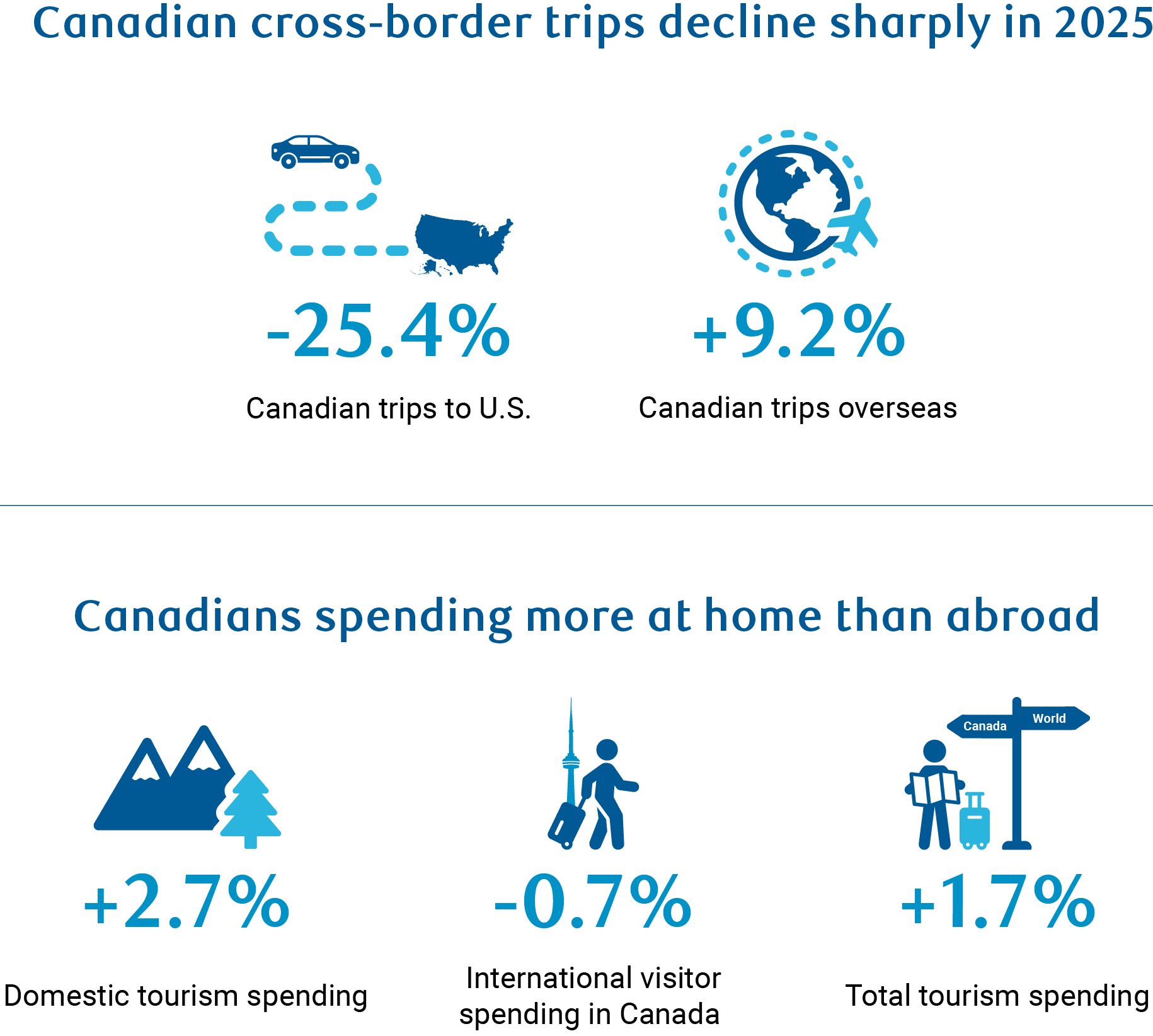

There is still significant travel between the closely linked economies—29.1 million Canadian residents returned from the U.S. in 2025. But, that was down 25.4% from 2024.

The slowdown didn’t reverse in early 2026 with January data showing a year-over-year contraction of roughly 23%.

The weakness has been broad-based across different types of travel, though land crossings drove the majority of the decline, accounting for 20.3% of the total contraction against air travel’s modest 3.5% share.

The outsized drop in vehicle crossings suggests shorter, discretionary cross-border trips have been particularly affected. Same day vehicle trips typically account for almost half of total travel by Canadians to the U.S.

Spending shifts inward as outbound demand softens

At the same time, Canadians are travelling differently.

Part of the shift is travel to non-U.S. destinations. About 14.2 million Canadians returned from overseas destinations in 2025, up 9.2% from 2024.

But, the larger offset has been increased spending on travel and tourism within Canada, helping to support the domestic sector.

Spending by international visitors within Canada declined 0.7% on average in 2025, while domestic tourism spending increased 2.7%, driving total tourism spending up 1.7% in 2025 from 2024.

This divergence reflects a gradual rotation toward domestic consumption. The trend appears consistent with the broader “buy Canadian” dynamics observed in other spending categories.

It’s helped improve Canadian international trade in services as a result. Canada has traditionally been a net importer of travel services with more Canadians travelling and spending abroad than foreign travellers spending in Canada.

That changed during the pandemic while the border closed, and Canada was, again, a net exporter of travel services in 2025 as softening import growth, which captures Canadian spending abroad, was larger than a pullback in spending from foreign visitors in Canada.

Tourism supports services as spending stays onshore

This shift in travel demand is helping to underpin activity in Canada’s service sector.

Tourism gross domestic product grew an annualized 4.8% in Q4, significantly outpacing an overall contraction of -0.6%. This marked the third consecutive quarter in which tourism activity outperformed the broader economy.

Dollars that might have been spent abroad are being recycled domestically, supporting accommodation, food services, transportation, and retail.

Accommodation and dining spending rose 5.6% in 2025. It’s a sharp contrast to international visitor accommodation spending declining by 2.2% over the year.

Vehicle rental showed a similar pattern. Domestic spending increased 4.9% for 2025, while international visitor spending declined 0.5% for the full year.

There are also second-round effects as increased domestic travel tends to boost discretionary spending in categories such as entertainment and recreation—amplifying the overall impact on consumer-facing sectors.

Travel rotation persists but growth remains modest

Looking ahead, the reallocation in travel patterns is likely to persist in the near term, but not indefinitely.

More broadly, domestic tourism spending remains elevated from pre-pandemic benchmarks with activity about 11% above 2019 averages. Growth has moderated from earlier post-pandemic surges, but still reflects steady resilience.

Our base case forecast remains one of a Canadian economy navigating headwinds, but staying on stable footing. Growth is expected to remain modest with domestic demand supported by easing monetary policy already in the system, and stabilizing labour market conditions.

For travel, this suggests a mixed outlook. On one hand, lower interest rates from recent peaks, and a lower unemployment rate should help sustain overall spending, including on travel. On the other hand, slower population growth, elevated uncertainty around trade policy, and the increase in fuel costs due to the Middle East conflict will limit upside.

Importantly, the current shift toward domestic travel does not require strong growth to continue. Domestic travel is no longer accelerating rapidly, but it continues to edge higher even as outbound travel softens.

Even in a subdued economic environment, Canadians may continue to favour domestic or alternative international destinations over U.S. travel, particularly if cross-border frictions or cost considerations persist.

About the author:

Abbey Xu is an economist at RBC. She is a member of the macroeconomic analysis group, focusing on macroeconomic forecasting models and providing timely analysis and updates on economic trends.

Nathan Janzen is an Assistant Chief Economist, leading the macroeconomic analysis group. His focus is on analysis and forecasting macroeconomic developments in Canada and the United States.

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. The reader is solely liable for any use of the information contained in this document and Royal Bank of Canada (“RBC”) nor any of its affiliates nor any of their respective directors, officers, employees or agents shall be held responsible for any direct or indirect damages arising from the use of this document by the reader. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.

This document may contain forward-looking statements within the meaning of certain securities laws, which are subject to RBC’s caution regarding forward-looking statements. ESG (including climate) metrics, data and other information contained on this website are or may be based on assumptions, estimates and judgements. For cautionary statements relating to the information on this website, refer to the “Caution regarding forward-looking statements” and the “Important notice regarding this document” sections in our latest climate report or sustainability report, available at: https://www.rbc.com/community-social-impact/reporting-performance/index.html. Except as required by law, none of RBC nor any of its affiliates undertake to update any information in this document.