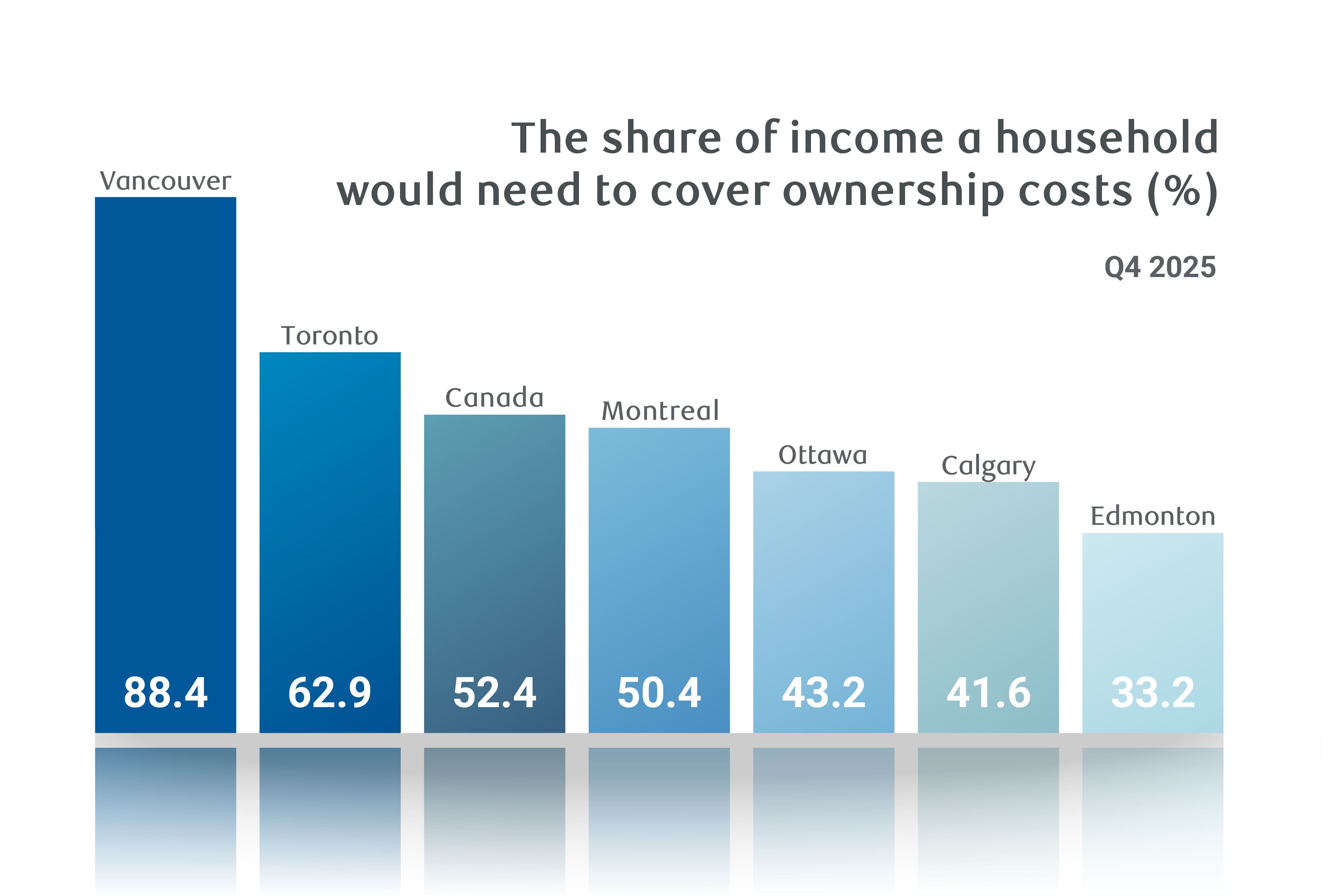

Housing affordability continues to improve in Canada. RBC’s national aggregate affordability measure eased for an eighth consecutive quarter to 52.4% in Q4 2025 from an all-time high of 63% at the end of 2023. A fall in the measure represents an increase in affordability.

Gains have slowed noticeably since the middle of 2025. Quarterly declines have moderated to -0.4 percentage point in the past two quarters from an average -1.6 ppts in the prior year and a half.

But, many local markets buck the improving trend. Montreal, Quebec City, Edmonton, Calgary and Winnipeg have seen back-to-back deteriorations in affordability. Vancouver and Toronto—where prices have been falling this past year—account for most of the national measure’s decline.

Gains look set to taper off further this year. With the Bank of Canada expected to be on hold through 2026, only price drops in certain markets and sustained household income growth can be counted on to lighten the ownership cost load.

A more varied picture has emerged—but it’s not unusual

What was nearly an across the board improvement in affordability conditions in 2024 has become sparser in Canada.

Only roughly half the markets we track remained on an easing trajectory by the second half of last year. Among them were the country’s priciest—and least affordable—markets of Vancouver, Victoria and Toronto.

These cities have been mired in slumps that drove property values and ownership costs lower. They were also among those that recorded more significant deterioration earlier during the pandemic, and thus, had more to reverse.

The half that is now seeing rising ownership costs generally boast of relatively tight supply, which is sustaining steady price appreciation.

Winnipeg, Montreal, Quebec City and St. John’s are prime examples. In these markets, affordability ceased to recover when interest rates stabilized in the fall.

Diverging trends across the country isn’t unusual. In fact, it’s a return to the norm after local market cycles were uncharacteristically synchronized during and immediately after the pandemic.

Little improvement in store

More varied outcomes will work to temper affordability gains in the year ahead.

Ongoing price corrections in some of Canada’s largest markets (including Toronto and Vancouver), and sustained (albeit slowing) income growth will continue to restore purchasing power. However, the pace of improvement will increasingly be contained by home price appreciation in many other markets (including parts of the Prairies and Quebec).

This means we’re likely approaching the end of the recuperation phase for housing affordability in Canada.

Further meaningful advancement would require steeper price declines or more robust income increases—neither seem likely under our base case forecasts, and housing scenarios for 2026 and 2027.

Victoria – Buyers still face major hurdles

Costs of owning a home fell further in Victoria with RBC’s aggregate affordability measure declining for the seventh time in the past eight quarters, down 1.5 percentage points to 66% in Q4.

Yet, it’s still nearly 36 ppts above where it was before the pandemic and more than 20 ppts above the long-run average, indicating prospective buyers still face major hurdles.

Unsurprisingly, home sales remain weak, and increased inventory heats up competition between sellers, causing prices to fall. We expect further depreciation ahead.

Vancouver – Slump in full force

Vancouver’s downtrend continues despite material easing in ownership costs in the past year.

RBC’s aggregate measure fell another 0.7 ppts last quarter, extending the decline to -7.2 ppts since Q4 2024—the steepest drop among markets we track. Truth is, Vancouver remains by far the least affordable market in Canada with a measure of 88.2%, and is still only about halfway into reversing the spike in costs during the pandemic.

It’s no wonder many would-be buyers are waiting for prices to fall further before entering the market. We think more abundant inventory will keep property values declining.

Calgary – Affordability has largely normalized

Calgary does feel some of the effects of the broader headwinds hampering other markets, but still maintains a solid pace of resales—some 30% above pre-pandemic levels.

Part of this resilience, no doubt, has to do with the fact that affordability has largely normalized near historical levels. At 41.5%, RBC’s aggregate measure is just slightly higher than its long-term average (39.2%).

Strong homebuilding has increased supply in the past year, contributing to cooling prices. This appears to be sustaining buyers’ interest.

Edmonton – Buyers active despite softer activity

The situation is similar in Edmonton where affordability is back within historical norms, and transactions continue to hover at strong levels despite softening in the past year.

RBC’s aggregate measure stood at 33.1% in Q4, just 0.7 ppts above its long-run average. Home resales fell 5.8% last year, but still stood close to 50% above pre-pandemic levels at the start of 2026.

The outlook for buyers appears more positive as earlier supply-demand tightness has eased materially, and price appreciation moderates.

Saskatoon – Showing some volatility

Overall, the tone remains one of vigour in Saskatoon. Home resales are still more than 40% above levels just before the pandemic—rising a further 2.4% in the past year—though there’s more volatility of late.

Economic and geopolitical turbulence could be taking a toll on confidence. Home values have levelled off after steadily appreciating since 2023 despite still-tight supply and demand.

Affordability is unlikely to be an issue for most buyers. RBC’s aggregate measure was 32% in Q4, just marginally worse than the 31% long-term average. We think constructive affordability will prove a powerful counterweight to any confidence blow from external factors.

Regina – Most affordable market

Regina has seen strong resales become more variable in recent months. However, it may be more attributable to fewer homes up for sale than any notable erosion in sentiment.

A decline in new listings since late 2025 has limited options for buyers, and kept supply and demand historically tight.

Buyers enjoy the best ownership affordability among the markets we track—a situation that further improved in Q4. RBC’s aggregate measure eased 0.3 ppts to 26.3%. We see this continuing to fuel solid demand.

Winnipeg – Increasing stress at the margin

The two-year-long market rally in Winnipeg has hit some bumps with residential transactions softening since fall.

Supply factors are partly to blame. The number of sellers entering the market has dropped. However, rising ownership costs could be curbing buyers’ enthusiasm as well.

Winnipeg is one of only four markets we track where the RBC aggregate affordability measure has deteriorated in the past year, including a 0.4 ppt increase in Q4. While 32.6% would suggest conditions remain manageable for most buyers, the widening divergence from the historical average (29.4%) points to increasing stress at the margin.

Toronto – Notable affordability relief still comes short

Falling home values in the Toronto area are helping restore ownership affordability at one of the fastest paces in the country.

Not only is RBC’s aggregate measure down a hefty 6.9 ppts in the past year—including an eighth straight decline of 1.8 ppts in Q4—it’s the furthest along in reversing the massive pandemic increase among markets we track.

Declines since early-2024 have now offset some 80% of the earlier spike, which compares to a 52% overall average in Canada.

Yet, Toronto buyers still face difficult hurdles with 62.9% of a typical household’s income needed to cover the costs of owning an average home at current prices. This makes many prospective buyers reluctant to enter the market at a time of elevated economic uncertainty, and while prices look likely to drop further amid abundant inventory.

Ottawa – Affordability strains persist despite improvement

Cooling signs have emerged in Ottawa since fall as broader headwinds reach the nation’s capital.

Resales and values have broken from years-long rising trends, moderating slightly so far. Affordability remains strained despite easing materially the last two years.

RBC’s aggregate affordability measure (43.2%) is 6.7 ppts above its long-run average, and more than 8 ppts higher than it was before the pandemic. We think such strains will keep buyers cautious and determined to extract price concessions from sellers.

Montreal – Harder to afford a home

Montreal has displayed much resilience in the past year with resale transactions off only slightly, and prices maintaining their upward trajectory in the face of economic turbulence.

The flipside is it’s become harder to afford a home. RBC’s aggregate measure (50.4%) increased 1.1 ppts since Q4 2024 with most of the deterioration taking place in Q4 2025 (up 1.3 ppts). This has stunted the restoration process that began in 2023, and kept the measure near its worst level.

We think it will increasingly hold back buyers. For now, tight inventory maintains upward pressure on home values, though we’d expect gradual easing ahead.

Quebec City – Ownership costs at decades high

Quebec City has been one of Canada’s hotter markets with double-digit price gains in 2025.

Activity has become uneven lately, but inventory remains historically low and buyer competition intense. Affordability hasn’t improved at all this cycle.

RBC’s aggregate measure stands at its worst level in more than three decades. Still, at 35.9%, it compares favourably to Montreal and other major Canadian centres, keeping buyers engaged.

We expect low supply to demand continuing to sustain solid home value gains.

Saint John – Recovery running out of steam?

Saint John stayed on a recovery track last year with resales rising 7.6%, and home prices consolidating earlier gains.

Results have been more variable in early-2026, though. Home values have recently come under downward pressure as previously tight supply-demand conditions eased. The upside is it’s helping to further restore affordability.

RBC’s aggregate measure edged 0.3 ppts lower to 30.9% in Q4, the fifth drop in the past six quarters. More progress is needed to reset conditions to pre-pandemic levels, but Saint John continues to rank among the most affordable markets we track.

Halifax – Challenging environment holds back buyers

Affording a home in Halifax remains challenging despite ownership costs easing in the past couple of years.

RBC’s affordability measure was a hefty 41.2% in Q4 or still more than 11 ppts above its long-run average. Cost declines since early 2024 have reversed only one-third of steep pandemic increases.

Persistent strains have contributed to stalling resales in 2025, though the impact on prices was largely muted through most of the year. Still tight supply relative to demand, and low—albeit rising—inventory have maintained support for home values.

That said, some price softness has emerged more recently, and could develop further.

St. John’s – Affordable conditions keep buyers motivated

St. John’s continues to operate at a high level with home resales up a solid 8% last year, exceeding pre-pandemic levels by more than 50%.

Highly affordable conditions are keeping buyers motivated. RBC’s aggregate measure for St. John’s (29.3%) is the second best among tracked markets. The fact that it deteriorated modestly in the past year did little to dampen enthusiasm.

Strong demand relative to supply has sustained steady price increases. We expect further gains near term.

Read the full report for extensive market-by-market analysis

Robert Hogue is an Assistant Chief Economist, responsible for providing analysis and forecasts on the Canadian housing market and provincial economies.

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. The reader is solely liable for any use of the information contained in this document and Royal Bank of Canada (“RBC”) nor any of its affiliates nor any of their respective directors, officers, employees or agents shall be held responsible for any direct or indirect damages arising from the use of this document by the reader. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.

This document may contain forward-looking statements within the meaning of certain securities laws, which are subject to RBC’s caution regarding forward-looking statements. ESG (including climate) metrics, data and other information contained on this website are or may be based on assumptions, estimates and judgements. For cautionary statements relating to the information on this website, refer to the “Caution regarding forward-looking statements” and the “Important notice regarding this document” sections in our latest climate report or sustainability report, available at: https://www.rbc.com/community-social-impact/reporting-performance/index.html. Except as required by law, none of RBC nor any of its affiliates undertake to update any information in this document.