The dust is settling after favorable headlines on discussions between US and Iran knocked oil prices down notably this week. Still, the reality remains that oil prices above $80/barrel are still a meaningful departure from our price expectations earlier this year. And with additional data reporting in the coming weeks for March, we expect that crosscurrents will continue to be the prevailing theme in the near term.

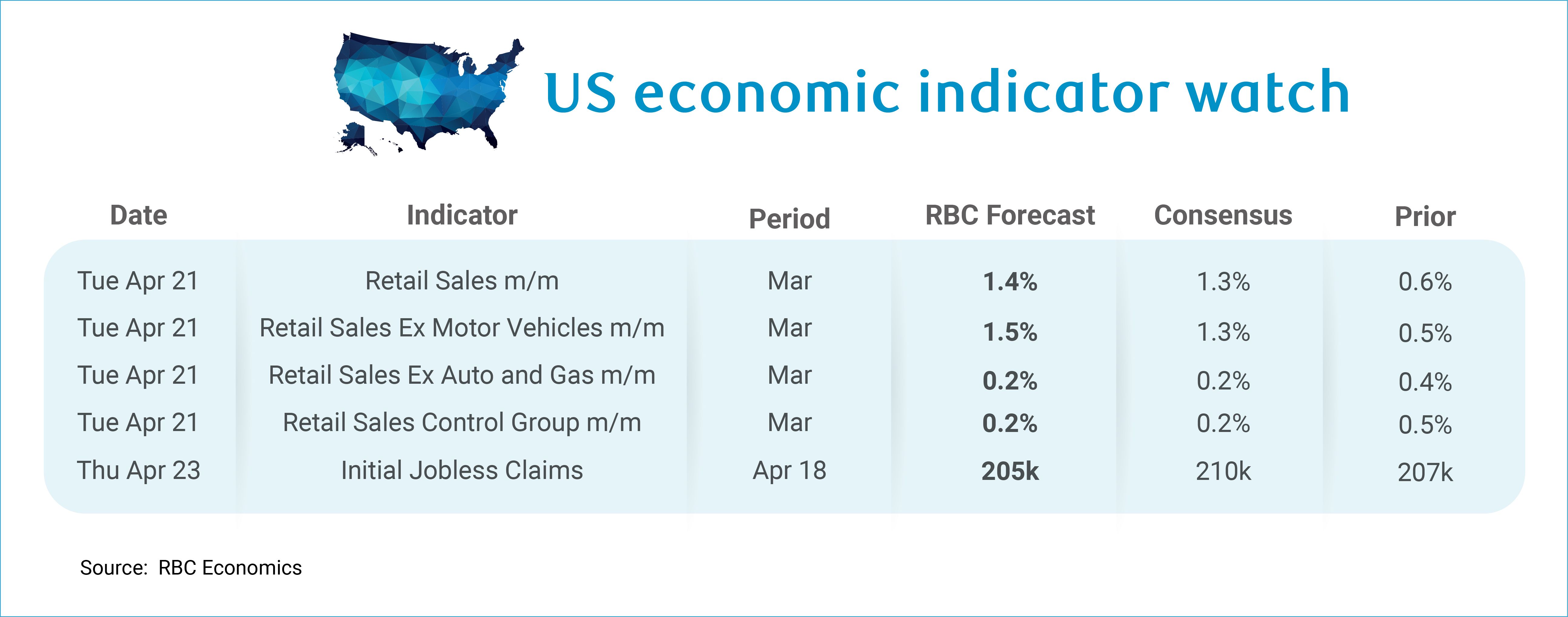

Next week the focus will be on retail sales for March. Headline retail sales are expected to be boosted by higher gasoline prices—regular gasoline prices spiked 26% in March, and since retail sales report nominal spending, we expect spending likely rose by 1.4% relative to February. Light motor vehicle sales posted another strong month, which will also lift the headline. But excluding both motor vehicles and gas, we expect retail spending was more subdued (+0.2% m/m). Spending growth in the retail control group is expected to slow to +0.2% because we anticipate softer discretionary goods spending, after sizeable pre-tariff front-running last year. Specifically, spending on clothing and sporting goods are expected to slow after having posted continuously strong year-over-year growth. We expect the pace of year-over-year spending in these categories will remain elevated but below the highs witnessed in recent months.

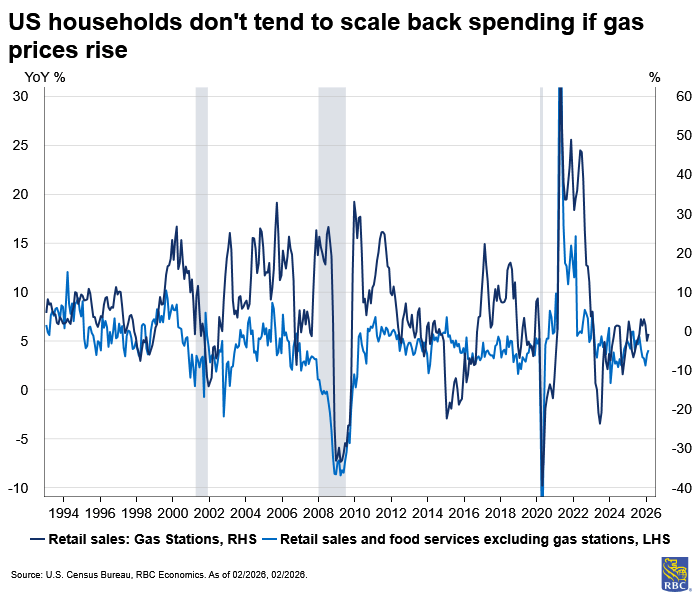

Still, we do not expect the spike in gasoline prices to lead to a reduction in nominal retail sales for two reasons. First, households have historically drawn down savings to compensate for higher gasoline prices. And second, households do not appear to offset higher gasoline consumption with weaker spending in other areas, based on what we have witnessed during prior gas price spikes.

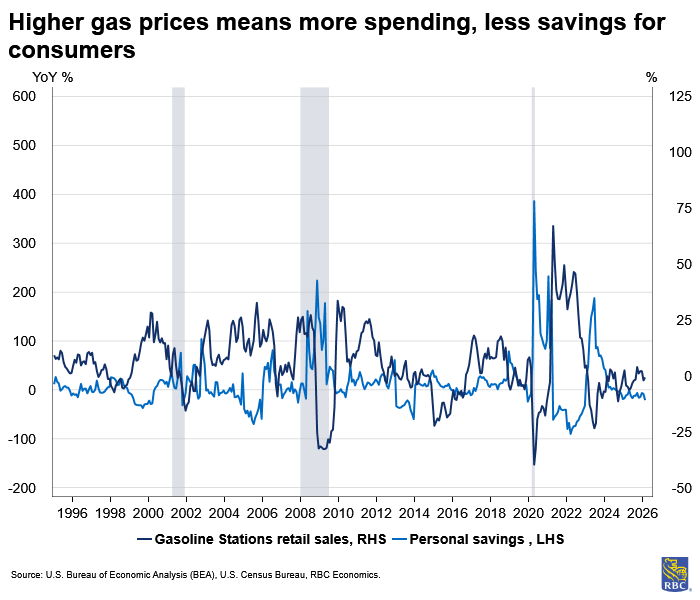

This applies beyond March. We previously estimated a range of scenarios from $75/barrel to $100/barrel. A $100/barrel scenario would represent roughly $150 billion in additional nominal gasoline spending, since each $10/barrel increase in WTI typically translates to a 30-cent increase in gasoline prices. Over the past 30 years, the change in oil prices has been more strongly correlated with personal savings than consumption excluding gasoline. This suggests consumer spending will likely remain broadly intact, with households tapping into savings instead. Our $100/barrel scenario would translate to a 0.7 percentage point hit to the savings rate, bringing it down to 3.3%—the lowest since 2022, when Russia’s invasion of Ukraine coincided with the post-pandemic spending boom. And a $75/barrel scenario would knock the personal savings rate down by 0.3 percentage point. We are likely to see a result somewhere in between these two scenarios, with the personal savings rate falling between 0.3 and 0.7 percentage point.

But some of the pain is being masked. The savings rate is reflective of all consumers on aggregate, with higher earners – who have notably higher savings rates – skewing the savings rate higher. Lower income households will have fewer savings to draw down and are expected to rely increasingly on credit in the face of higher gasoline prices. With this in mind, the dip into savings will not be sustainable in the long run, especially since lower income consumers are already showing signs of stress (for example, higher rates of delinquency) and are now starting to feel the pinch of tariff passthrough. The key determinant of consumers’ ability to manage the shock will be duration and magnitude. While consumers can likely manage a $100/barrel scenario in the short run, if prices settle materially higher for an extended period of time, this could become problematic.

Aside from retail data, here’s what else we’re watching:

-

Initial jobless claims will likely settle sideways at 205k for the week of April 18th after a downside the prior week. Continuing claims (for the week of April 11th) will be important to watch this coming week, since the week containing the 12th of the month is the reference week for the household survey. Initial claims have held largely steady in the April reference week relative to March. This continues to support our view that the unemployment rate will settle sideways against a continued low net new hire, low fire backdrop.

-

Next week we will get the final data from U-Michigan for both consumer sentiment and inflation expectations. Given the recent volatility in energy prices, we would not be surprised if the 1-year inflation expectations are more revision prone than usual. Interestingly, 5-to-10-year inflation expectations have remained relatively well anchored despite a full percentage point uptick in the 1-year expectations preliminary print relative to the March final.

About the Authors:

Mike Reid is Head of US Economics at RBC. He is responsible for generating RBC’s US economic outlook, providing commentary on macro indicators, and producing written analysis around the economic backdrop.

Carrie Freestone is a Senior US Economist at RBC. Carrie is responsible for projecting key US indicators including GDP, employment, consumer spending and inflation for the US. She also contributes to commentary surrounding the US economic backdrop which she delivers to clients through publications, presentations, and the media.

Imri Haggin is an US Economist at RBC, where he focuses on thematic research. His prior work has centered on consumer credit dynamics and treasury modeling, with an emphasis on leveraging data to understand behavior.

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. The reader is solely liable for any use of the information contained in this document and Royal Bank of Canada (“RBC”) nor any of its affiliates nor any of their respective directors, officers, employees or agents shall be held responsible for any direct or indirect damages arising from the use of this document by the reader. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.

This document may contain forward-looking statements within the meaning of certain securities laws, which are subject to RBC’s caution regarding forward-looking statements. ESG (including climate) metrics, data and other information contained on this website are or may be based on assumptions, estimates and judgements. For cautionary statements relating to the information on this website, refer to the “Caution regarding forward-looking statements” and the “Important notice regarding this document” sections in our latest climate report or sustainability report, available at: https://www.rbc.com/community-social-impact/reporting-performance/index.html. Except as required by law, none of RBC nor any of its affiliates undertake to update any information in this document.