The Bottom Line:

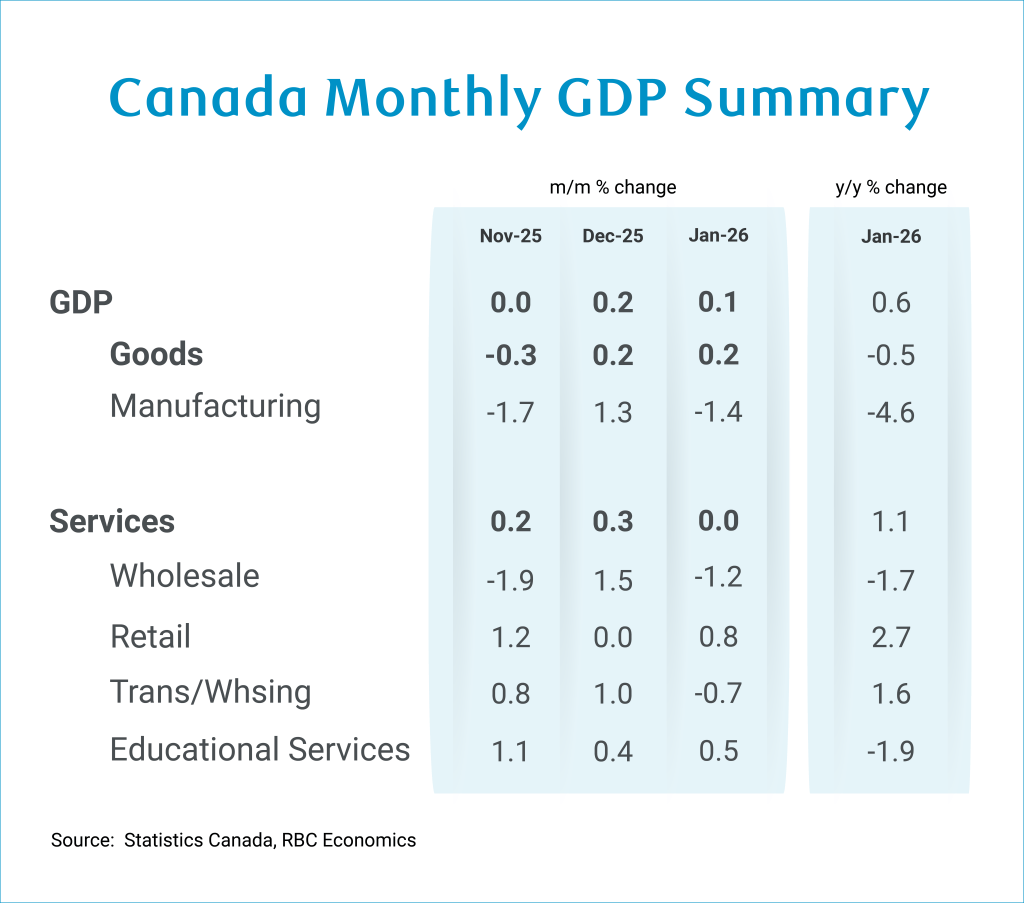

Canada’s GDP growth increased by 0.1% in January, marking a deceleration from the 0.2% gain in December but slightly higher than Statistics Canada’s advance estimate a month ago and our own expectations of flat performance. Goods-producing industries delivered upside surprises while services activity remained essentially flat and aligned with forecasts. Temporary factors influenced results, particularly in manufacturing, where auto plant shutdowns linked to longer than usual model changeovers weighed on output.

Weak spots in January were concentrated in manufacturing, wholesale trade, and housing-related sectors. These pullbacks were offset by stronger energy production, construction sector output, and a modest rebound in mining excluding oil and gas. Retail volumes also rose, pointing to continued resilience in consumer spending at the start of the year.

Looking ahead, advance GDP estimate suggests continued expansion in February (+0.2%) as temporary drags begin to fade. This aligns with early industry indicators. Manufacturing sales rebounded, supported by stronger transportation equipment and food production, while retail and wholesale metrics also point to positive momentum.

On a quarterly basis, activity remains broadly consistent with our base case for moderate expansion following negative Q4 performance with the early monthly data tracking between our own 1.3% (annualized rate) Q1 GDP growth forecast and the Bank of Canada’s 1.8% projection. With slowing population, per-capita improvement is expected to continue. For the Bank of Canada, we expect the policy rate to remain on hold, as officials await greater clarity on elevated oil prices due to the ongoing conflict in the Middle East and the impacts on inflation.

The Details:

-

Real GDP edged up 0.1% in January, following a 0.2% gain in December, slightly exceeding the flat advance estimate from Statistics Canada and our own pre-release expectations.

-

With the advance estimate for February GDP pointing to continued expansion of 0.2%, Q1 performance is tracking between our base case of 1.3% (quarter-over-quarter annualized rate) and the Bank of Canada’s 1.8% projection in the January Monetary Policy Report.

-

January’s headline growth was mainly driven by goods-producing industries (+0.2%), while service sector output remained essentially flat.

Manufacturing acted as a key drag within goods-producing industries due to shutdowns at several major auto plants in Ontario related to model changeovers. However, advance February manufacturing sales rose 3.8% in nominal terms, according to Statistics Canada, driven by strength in transportation equipment and food product manufacturing. -

Offsetting those drags, oil and gas extraction posted a notable rebound of 1.6%, which Statistics Canada attributed to increased crude petroleum and natural gas production. Mining excluding oil and gas also advanced 0.4%, partially recovering from the 1.4% contraction in December.

-

Additionally, the construction sector saw its third consecutive monthly advance, with January activity jumping 1.1%. All sub-sectors showed improvement, reflecting increased residential renovations and multi-unit housing development, while non-residential building construction extended its winning streak, supported by institutional and commercial projects.

-

Within services-providing industries, the wholesale sector declined and reversed most of its prior month’s gain, due to auto production disruptions. Housing-related activity remained soft, consistent with weaker home resales in January.

-

Transportation and warehousing sector output experienced pullbacks in January, following two consecutive monthly gains. This was attributed to severe winter storms during the latter portion of the month.

-

Offsetting these declines, retail GDP rebounded 0.8%, and the advance retail indicator for February pointed to another 0.9% increase in nominal sales. This aligns with our own tracking of cardholder spending. Additionally, finance and insurance sector output also ticked higher by 0.5% in January.

About the Author

Abbey Xu is an economist at RBC. She is a member of the macroeconomic analysis group, focusing on macroeconomic forecasting models and providing timely analysis and updates on economic trends.

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. The reader is solely liable for any use of the information contained in this document and Royal Bank of Canada (“RBC”) nor any of its affiliates nor any of their respective directors, officers, employees or agents shall be held responsible for any direct or indirect damages arising from the use of this document by the reader. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.

This document may contain forward-looking statements within the meaning of certain securities laws, which are subject to RBC’s caution regarding forward-looking statements. ESG (including climate) metrics, data and other information contained on this website are or may be based on assumptions, estimates and judgements. For cautionary statements relating to the information on this website, refer to the “Caution regarding forward-looking statements” and the “Important notice regarding this document” sections in our latest climate report or sustainability report, available at: https://www.rbc.com/community-social-impact/reporting-performance/index.html. Except as required by law, none of RBC nor any of its affiliates undertake to update any information in this document.