The Bank of Canada held the overnight rate at 2.25% at its second meeting of 2026, and conveyed three key messages through its interest rate announcement and press conference opening statement.

First, there are downside risks to economic growth in early 2026 relative to the BoC’s January forecast. Second, it is too early to assess the overall growth impact from the Middle East conflict and elevated oil prices. Third, energy prices will rise immediately and be looked through by the central bank, but only if the increase remains contained—not if it broadens and persists.

With recent CPI readings showing persistent easing in underlying price pressure (core BoC measures averaged 1% on a three-month annualized basis in February), the BoC has plenty of room to wait for additional clarity on the impact of recent conflict rather than rushing to respond.

“Risks to growth look tilted to the downside” relative to the January forecast

Early in 2026, employment growth in Canada was soft, and the unemployment rate has not improved meaningfully from the end of last year, standing at 6.7% in February compared to 6.8% on average in Q4 2025.

Consumer spending momentum, according to our tracking of RBC card spending data appeared to have stalled in January though February showed a moderate rebound. Governor Macklem highlighted tightened financial conditions—rising bond yields, falling equity markets, and widening credit spreads—in recent weeks as a result of the Iran conflict.

Overall, data suggests downside risks relative to the BoC’s January forecast of a 1.8% quarterly annualized GDP growth for Q1, though expectations for modest overall growth in 2026 were largely retained.

“It’s too early to assess the impact of the conflict in the Middle East on growth in Canada.”

The recent Middle East conflict was the key focus heading into this meeting. As expected, Governor Macklem did not commit to a particular view on the net growth impact for Canada.

The BoC did explore different transmission channels, largely consistent with our own analysis: income from energy exports will rise alongside elevated oil prices, but higher energy costs will hurt consumer purchasing power. Crucially, we also expect little investment response—historically where most of the positive growth from higher oil prices has stemmed from.

Concerns about U.S. tariffs and trade headwinds remain, with the review of the Canada-United States-Mexico Agreement noted as “a big unknown.”

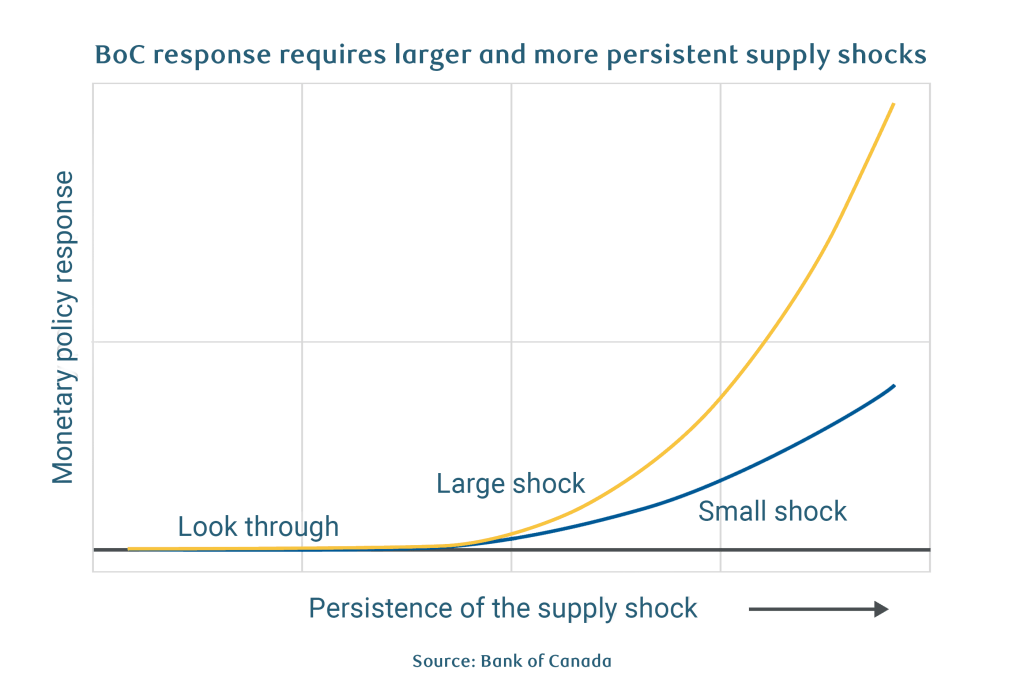

“Governing Council will look through the war’s immediate impact on inflation.”

In line with Governor Kozicki’s recent speech, Governor Macklem reiterated in today’s press conference that the immediete impact on higher energy infaltion will be “looked-through” by the central bank.

With the Canadian economy operating in excess supply and recent inflation readings showing continued progress in easing underlying price pressure, the BoC deemed the risks of higher energy inflation spreading to other goods and services as “contained.” but cautioned that contagion risks will increase the longer the conflict persists.

Overall, this represents another supply shock—following concerns over U.S. tariffs—that presents the BoC with competing priorities between supporting growth and maintaining at-target inflation. Amid a fluid and constantly evolving situation, we expect the BoC to remain prudent, maintaining the overnight rate at 2.25% while awaiting additional clarity.

About the author:

Claire Fan is a Senior Economist at RBC. She focuses on macroeconomic analysis and is responsible for projecting key indicators including GDP, employment and inflation for Canada and the US.

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. The reader is solely liable for any use of the information contained in this document and Royal Bank of Canada (“RBC”) nor any of its affiliates nor any of their respective directors, officers, employees or agents shall be held responsible for any direct or indirect damages arising from the use of this document by the reader. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.

This document may contain forward-looking statements within the meaning of certain securities laws, which are subject to RBC’s caution regarding forward-looking statements. ESG (including climate) metrics, data and other information contained on this website are or may be based on assumptions, estimates and judgements. For cautionary statements relating to the information on this website, refer to the “Caution regarding forward-looking statements” and the “Important notice regarding this document” sections in our latest climate report or sustainability report, available at: https://www.rbc.com/community-social-impact/reporting-performance/index.html. Except as required by law, none of RBC nor any of its affiliates undertake to update any information in this document.