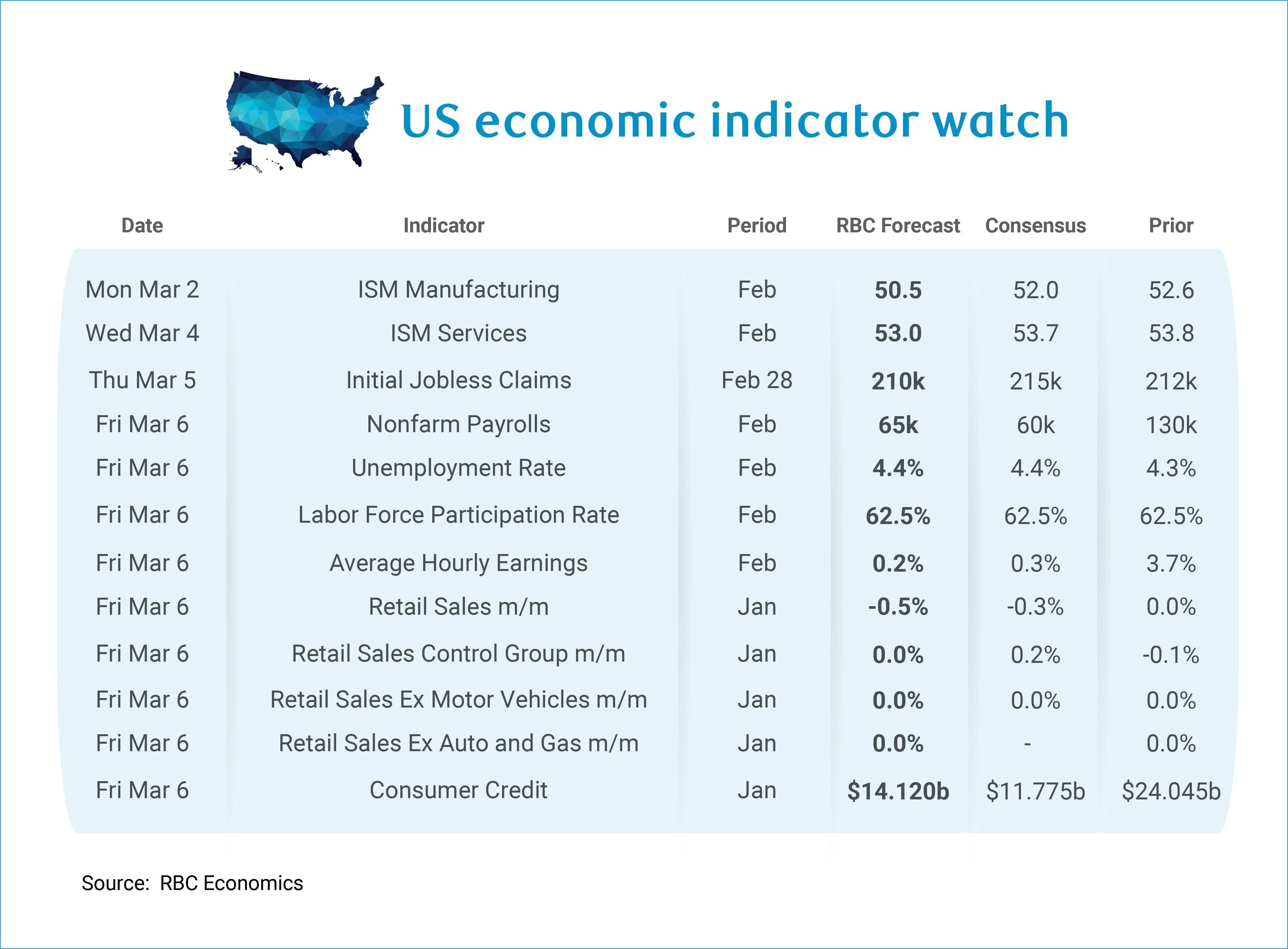

Next week will be data heavy for economists and market participants alike. The highlights will be the February employment report and January retail sales report, which will be released concurrently on March 6. In terms of job growth, we expect to see January’s surge was a one-off. Still, we are forecasting a healthy +65k uptick in employment for the month of February. We also expect to see the unemployment rate retrace January’s improvement, ticking up to 4.4% in February.

There are a few reasons why we do not expect the January job surge will be sustained. First, the centerpiece of the report was a health care and social assistance story which came in well-above trend and is unlikely to be repeated. Notably, the sector saw below-trend hiring from August to December and we suspect January made up for the hiring lull. Second, construction has been volatile in recent months and the late January snowstorm that blanketed the Midwest and Northeast likely weighed on hiring. Third, there is limited prospect of a meaningful ramp up in services activity outside of health care in February, as trade-exposed sectors continue to shed jobs. Real retail sales were notably weak in December, and we expect results some layoffs. Additionally, any ramp-up in hiring to beat the new section 122 tariffs would not show up in February’s employment report since this was announced after the reference week. Overall jobless claims largely moved sideways but the January reference week was the trough for continuing claims, which means that continuing claims will look relatively higher in the February reference week. We think this adds to the unemployment rate as a result.

The February employment report will also incorporate annual adjustments to the household survey population estimates. These adjustments are typically made in the January report but was delayed this year because of the government shutdown. Census estimates indicate that population growth was likely overestimated in 2025, and we expect to see slower population growth in 2026. These changes affect labor force, employment, and unemployment levels but typically have minimal impacts on rates and ratios though we still could see a slight impact to the labor force participation rate.

January’s retail sales report should be the final delayed retail report, having faced significant disruptions since the government shutdown. We expect to see that retail sales outright declined in January (-0.5% m/m), with significantly weaker motor vehicle sales weighing on headline growth. Lower gasoline prices should also weigh on nominal sales. Excluding auto sales and gasoline, retail sales will likely hold largely flat after weak December data signaled consumer appetite for goods has likely dissipated after a significant pre-tariff pull forward earlier in 2025. Higher consumer loan delinquencies in Q4 suggests that US consumers (specifically lower-and-middle income earners) are increasingly stretched with less room for discretionary spending.

Aside from payroll employment and retail sales, here’s what else we’re watching next week:

-

ISM manufacturing is expected to come in softer for February at 50.5 – weaker yet still not in contractionary territory after the January print after we saw improvements in 3 of 5 regional Fed surveys (Texas, Kansas City, and Empire). The Philly Fed Survey, on the other hand, posted its weakest diffusion index since April which will likely temper the improvements in other regions.

-

ISM Services will also likely come in a bit softer in February at 53.0 as Texas, Philly, and Richmond Fed all pointed to weaker services activity. Perhaps more interesting than the headline prints for both ISM surveys will be the employment and price indices. We expect to see still-weak hiring and a price trajectory that is heating up.

-

Initial claims are likely to come in on the cooler side again for the week ending February 28th – our forecast calls for 210k. Major storms in the Northeast do pose downside as they could have delayed the filing of claims this past week. In general, claims have been in-line with our view that the US labor market continues to operate in a low firing backdrop.

-

Consumer credit will close out the week and we expect it will be less jarring in January but will still move notably higher by +$14.1b. As of late, we have seen both revolving and nonrevolving credit move higher, but the bulk of the uptick will likely come from nonrevolving credit (i.e. auto loans, student loans, and mortgages).

About the Authors

Mike Reid is Head of U.S. Economics at RBC. He is responsible for generating RBC’s U.S. economic outlook, providing commentary on macro indicators, and producing written analysis around the economic backdrop.

Carrie Freestone is a Senior US Economist at RBC Capital Markets. Carrie is responsible for projecting key US indicators including GDP, employment, consumer spending and inflation for the US. She also contributes to commentary surrounding the US economic backdrop which she delivers to clients through publications, presentations, and the media.

Imri Haggin is an Economist at RBC Capital Markets, where he focuses on thematic research. His prior work has centered on consumer credit dynamics and treasury modeling, with an emphasis on leveraging data to understand behavior.

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. The reader is solely liable for any use of the information contained in this document and Royal Bank of Canada (“RBC”) nor any of its affiliates nor any of their respective directors, officers, employees or agents shall be held responsible for any direct or indirect damages arising from the use of this document by the reader. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.

This document may contain forward-looking statements within the meaning of certain securities laws, which are subject to RBC’s caution regarding forward-looking statements. ESG (including climate) metrics, data and other information contained on this website are or may be based on assumptions, estimates and judgements. For cautionary statements relating to the information on this website, refer to the “Caution regarding forward-looking statements” and the “Important notice regarding this document” sections in our latest climate report or sustainability report, available at: https://www.rbc.com/community-social-impact/reporting-performance/index.html. Except as required by law, none of RBC nor any of its affiliates undertake to update any information in this document.