Canada’s labour force is going through a period of unprecedented structural change for more than one reason.

It’s been well telegraphed that caps on temporary and permanent resident arrivals from abroad mean the population is on track to shrink for the first year on record in 2026. And with a rising share of the population hitting retirement age, the size of the available workforce will decline more than the population, and for the first time on record outside of the pandemic.

The unemployment rate remains high following the Bank of Canada’s 2023-24 tightening cycle and disruptions from U.S. tariffs, giving policymakers room to maintain restrictive caps on immigration for now. But under the surface, longer-run structural headwinds against labour supply are building.

We have noted this trend creates an unusual combination: Less job growth (even potentially small declines) would still be sufficient for per-worker labour market conditions to improve with the unemployment rate drifting lower—i.e. Canada’s “breakeven” employment rate has declined sharply.

And we pointed out the growing fiscal costs of an aging population over time with a rising share of the population retired, and no longer contributing as much to the current government revenue base but still consuming and utilizing public services.

What has received less attention is the extent to which Canada (like virtually all other advanced economies) relies on immigration to fuel labour force growth.

Without immigration, Canada’s population of potential younger workers (under age 35) would outright decline into the 2030s, while retirements of older workers remain at record-highs. Current immigration restrictions are expected to ultimately be relaxed as the goals of reducing the temporary resident share of the population are approached, but it’s not likely enough to fully offset structural labour supply headwinds in the future.

That’s a good thing for workers. It means pockets of labour market weakness—particularly challenges for younger workers finding first jobs—will ease.

But, for businesses it also means that labour shortages will, eventually, return once the unusually high level of unemployment is absorbed.

Retirements are high, will remain elevated into 2030s

Retirements are at a structural high with monthly retirements climbing to roughly 0.12% of the labour force—about 25,500 workers per month. That’s nearly double two decades ago when retirements averaged closer to 14,000 per month.

This has long been expected as the large post-WWII baby boomer generation hit retirement age in greater numbers. That wave may have peaked, but it has not yet crested, and likely won’t into the 2030s.

The youngest baby boomers will turn 65 in 2029 (70 in 2034), so the current wave of retirements has further room to run.

Retirements tend to begin edging higher for workers over the age of 55, and peak between 65 and 69. But, a significant share of the population works longer—the immigrant population (which accounts for 28.4% of Canada’s workforce) has tended to retire later.

Population aging (and resulting retirements) has already reduced the labour force participation rate (share of the population aged 15 and older working or looking for work) by 4.5 percentage points from two decades ago. It will continue to push the share of the population available to work lower in the decade ahead.

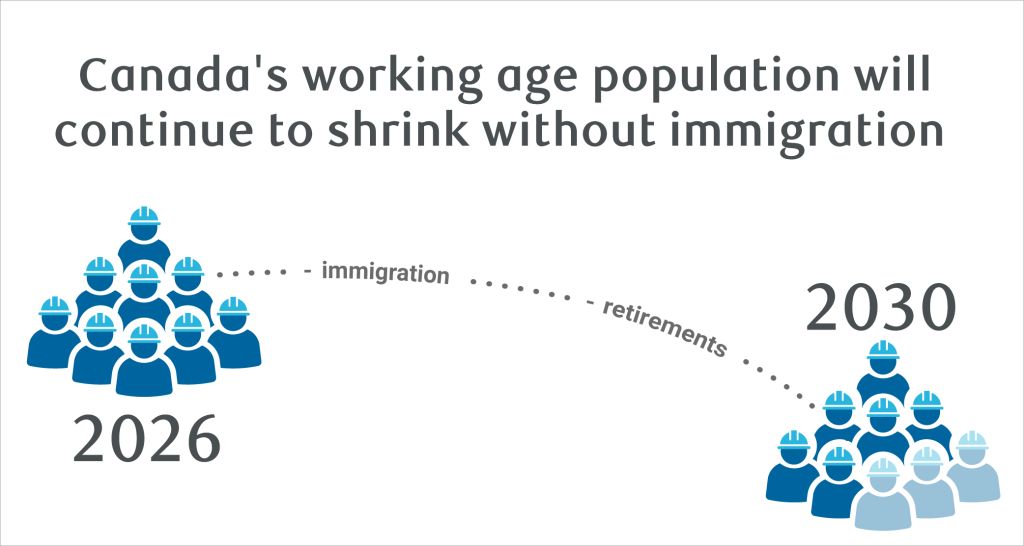

Labour force would continue to decline without immigration

The reality is, like virtually all other advanced economies, Canada’s “working age” population will decline in the absence of immigration.

The number of children per woman fell sharply following the post WWII baby boom, and has been below typical population replacement rates for decades.

The population in each age cohort up to age 35 is smaller than the next. In other words, the supply of potential new younger workers will shrink without immigration at the same time a historically high share of the workforce leaves for retirement.

This is already happening now. The population under the age of 35 declined by a record 120,500 from a year ago in April. The available workforce under age 35 is down 76,000 despite a small increase in the share of younger people working or actively looking for work (unemployed).

Part of that more recent decline in the younger workforce is tied to a net outflow of temporary residents, but without any impact from immigration, the population aged 15-34 would decline by roughly 186,000 per year over the next five years (roughly 15,500 per month), according to our estimates.

Without significant changes in age-specific labour force participation rates, available workers under-35 would fall by about 139,000 per year (roughly 11,600 per month on average) over the next five years.

This is all while workers continue to retire in record numbers at the other end of the age distribution.

Not enough workers ahead

With youth unemployment rates still in the double-digits, declines in the size of the labour force shouldn’t create a significant challenge for businesses looking to hire in the near term, and that’s a good thing for new job searchers who have struggled to find work in recent years.

But, challenges tied to a shrinking supply of new workers will build as per-worker labour markets improve (ie. the unemployment rate declines). Ultimately, current caps on immigration may need to be eased after the temporary resident population approaches the federal government’s target of 5% of the total population. We expect this will be reached around mid-2027.

Indeed, there have been early signs of some pockets of labour shortages that either never went away or are emerging again.

About 17% of firms in Canadian Federation of Independent Business surveys still report shortages of un/semi-skilled workers. That sits well below 40% plus peaks in 2022, but is already tracking around pre-pandemic norms—and doing so while the unemployment rate is still elevated.

About a fifth of businesses in the Bank of Canada’s Business Outlook Survey also reported labour shortages, and they expect the intensity of those shortages to edge higher.

Labour shortages are not (and won’t be) evenly distributed across the economy, but some sectors—including accommodation, food services and construction—still report labour shortages more frequently as an obstacle to growth near term over demand for their products.

About the authors:

Nathan Janzen is an Assistant Chief Economist, leading the macroeconomic analysis group. His focus is on analysis and forecasting macroeconomic developments in Canada and the United States.

Annie Zheng is an economist at RBC. She is a member of the macroeconomic analysis group, focusing on macroeconomic modeling.

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. The reader is solely liable for any use of the information contained in this document and Royal Bank of Canada (“RBC”) nor any of its affiliates nor any of their respective directors, officers, employees or agents shall be held responsible for any direct or indirect damages arising from the use of this document by the reader. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.

This document may contain forward-looking statements within the meaning of certain securities laws, which are subject to RBC’s caution regarding forward-looking statements. ESG (including climate) metrics, data and other information contained on this website are or may be based on assumptions, estimates and judgements. For cautionary statements relating to the information on this website, refer to the “Caution regarding forward-looking statements” and the “Important notice regarding this document” sections in our latest climate report or sustainability report, available at: https://www.rbc.com/community-social-impact/reporting-performance/index.html. Except as required by law, none of RBC nor any of its affiliates undertake to update any information in this document.