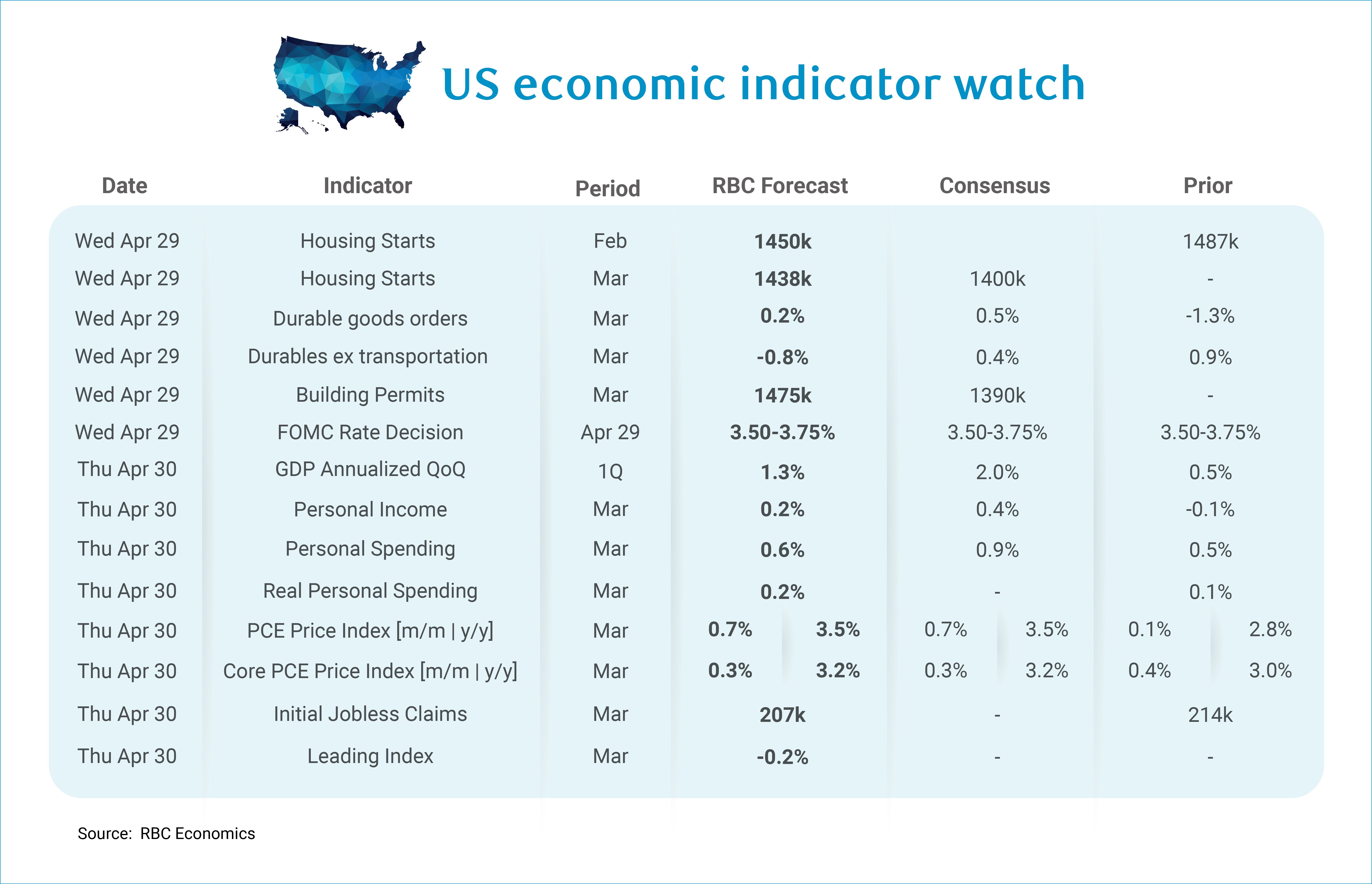

We expect a largely uneventful Fed meeting next week for a committee that is increasingly taking a backseat role – observing macroeconomic conditions and responding to them rather than steering them from the driver’s seat. In the face of compounding inflation shocks (a geopolitical event and a trade war), we expect that the Fed will stand pat and await additional data.

As a result of these shocks, we anticipate inflation will heat up in the coming months which will derail the Fed’s path towards what Chair Powell has characterized as the middle-range of neutral. At the last press conference, Chair Powell emphasized, “[…] you can characterize it (the current policy rate) as in the high end of neutral, or you can characterize it as perhaps mildly restrictive, even modestly restrictive.” Our Rates Strategists, Blake Gwinn and Izaac Brook, expect that the April 29th meeting will be a nonevent, with the Federal Funds Rate being held at 3.50-3.75% next week and for the foreseeable future.

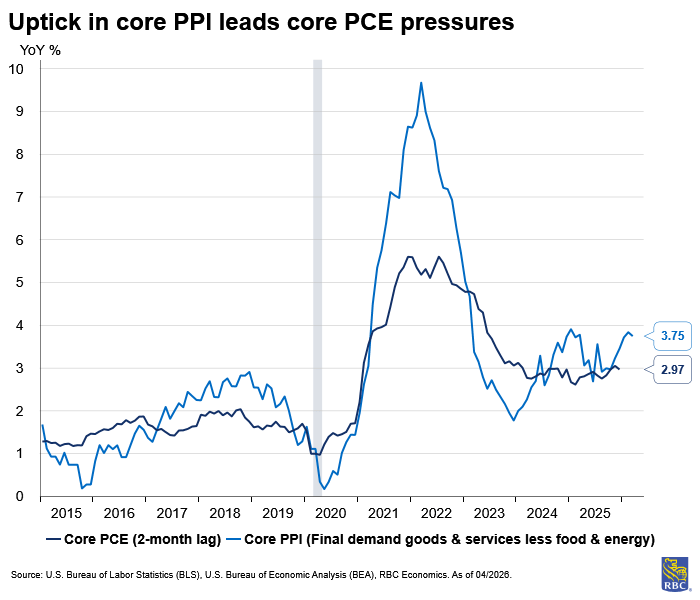

To date, headline prices have been driven significantly higher by gasoline price surges resulting from the Middle East Conflict. And while the Fed is more concerned with core inflation than headline, inflation expectations closely track gasoline prices, which could be problematic for the Fed. Zooming in on core inflation, core PCE, which is the Fed’s preferred measure of inflation, is still sitting at 3.0% y/y and we anticipate it continued to heat up in March (our forecast calls for an uptick in the year-over-year measure of core PCE to 3.2%). For March, we expect core PCE rose +0.3% m/m. While both core CPI and PPI came in below expectations in March, we do not expect to see the same reprieve in core PCE, since sectors that matter relatively more for PCE (like outpatient services and hospitals and nursing home services within health care PPI) were elevated in March. Higher jet fuel prices have also pushed airfares higher which drove up public transportation PPI, a subset of PPI that also matters for PCE.

We continue to anticipate that tariffs pressures will build in the months to come. PPI has been running hot in trade-exposed sectors. Core goods CPI is being helped by used motor vehicle prices, which are not subject to tariffs. But prices for new, imported goods within the CPI basket have risen since Liberation Day.

And the labor side of the Fed’s mandate is still healthy enough that cuts are unlikely this year. The unemployment rate has largely moved sideways as jobless claims data has stabilized at low levels. The US economy has only added an average of 15K jobs per month over the past six months (for a total of 90K jobs) – this is minimal for the US labor market. But this is largely a story of retirements. Firms are not creating new jobs on net, but they do not have to. The unemployment rate has ticked lower from 4.4% to 4.3% over the past six months, highlighting an exceptionally low breakeven rate of job growth. And we expect this will continue to be the case in 2026.

Aside from the Fed meeting and PCE, here’s what else we’re watching:

-

Personal spending is expected to rise +0.6% m/m in March but much of this is a price effect. Netting out the impact of inflation, real personal spending is expected to rise a more subdued +0.2%. We expect to see real spending on both durable goods and nondurables likely rose with services spending softer as a result of weaker financial services spending, reflecting equity market declines in the month of March (the S&P was down -3.5% relative to February).

-

Personal income is expected to rise by a modest +0.2% m/m in March. We expect wage income will be tempered by the fact that we saw a decline in weekly hours worked in March. Social security payments and Medicare payments will reflect a surge in retirements but will be at least partially offset by declines in Medicaid payments.

-

Durable goods orders likely ticked up by +0.2% m/m in March, after Boeing orders rose relative to February. However, excluding transportation, we expect to see that durable goods sales fell -0.8% m/m since activity was not strong enough to offset seasonal factors.

-

We get a slew of belated housing data next week. We expect to see housing starts trended lower in each of February and March, based on lower building permit issuance for single family units in January (and we expect the trend continued into February). We also get building permits data for March next week and anticipate that issuance picked up in the month of March.

About the Authors:

Mike Reid is Head of US Economics at RBC. He is responsible for generating RBC’s US economic outlook, providing commentary on macro indicators, and producing written analysis around the economic backdrop.

Carrie Freestone is a Senior US Economist at RBC. Carrie is responsible for projecting key US indicators including GDP, employment, consumer spending and inflation for the US. She also contributes to commentary surrounding the US economic backdrop which she delivers to clients through publications, presentations, and the media.

Imri Haggin is an US Economist at RBC, where he focuses on thematic research. His prior work has centered on consumer credit dynamics and treasury modeling, with an emphasis on leveraging data to understand behavior.

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. The reader is solely liable for any use of the information contained in this document and Royal Bank of Canada (“RBC”) nor any of its affiliates nor any of their respective directors, officers, employees or agents shall be held responsible for any direct or indirect damages arising from the use of this document by the reader. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.

This document may contain forward-looking statements within the meaning of certain securities laws, which are subject to RBC’s caution regarding forward-looking statements. ESG (including climate) metrics, data and other information contained on this website are or may be based on assumptions, estimates and judgements. For cautionary statements relating to the information on this website, refer to the “Caution regarding forward-looking statements” and the “Important notice regarding this document” sections in our latest climate report or sustainability report, available at: https://www.rbc.com/community-social-impact/reporting-performance/index.html. Except as required by law, none of RBC nor any of its affiliates undertake to update any information in this document.