Key findings

-

Modern Methods of Construction (MMC) refers to innovative homebuilding approaches to improve the efficiency, sustainability and quality of construction. It includes of off-site construction, including 3D volumetric modules, 2D panels and pre-fabricated components, as well as innovative on-site approaches, such as robotics and digital tools.

-

It can help build homes up to 50% faster and 40% cheaper than traditional methods. Yet current conditions actively prevent adoption at scale—leaving Canada’s housing crisis unresolved.

-

MMC currently makes up 7.5% of the Canadian construction market. Forecasts show it’s set to grow at a compounded annual growth rate of 5% by 2029.1

-

Deploying these new methods could meaningfully contribute towards Canada’s housing needs. Raising MMC ‘s contribution to 15% of annual supply needs (about 72,000 units a year), would require developing dozens of new factories at current production capacities.2

-

Canadian policy, market, and financing conditions are hindering wider MMC adoption. Reshaping policy and regulatory frameworks and financing mechanisms to support off-site construction can unlock the market commitment needed for MMC to scale

-

Proven methods exist globally. Several international examples—Sweden’s industrialized housing sector, Japan’s engineered modular homes and the U.K.’s MMC agenda—provide valuable lessons for Canada.

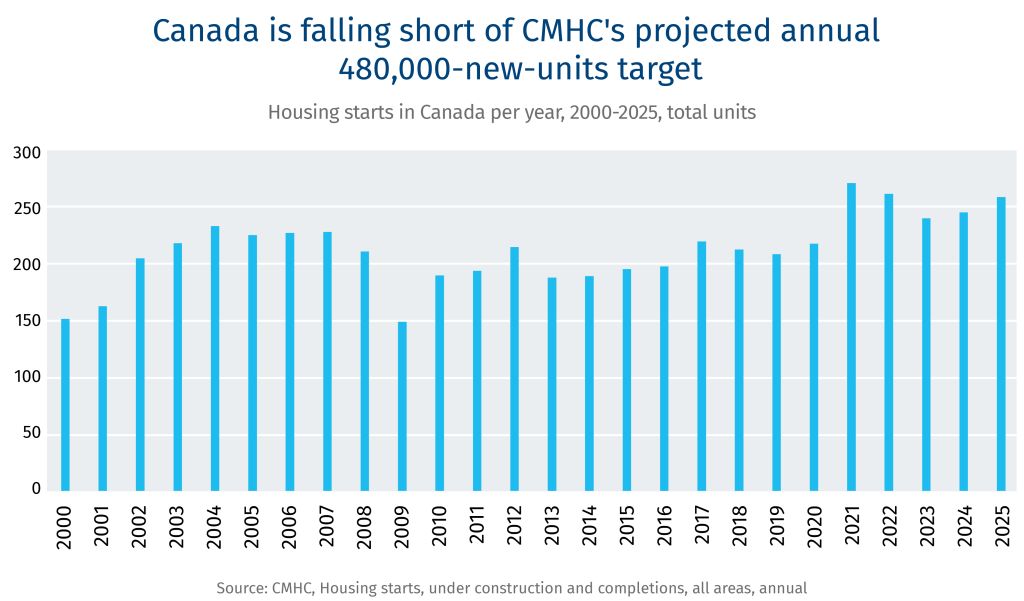

Home prices in virtually every major Canadian city, and many smaller communities, have soared out of reach for many people. While the causes of Canada’s housing crisis are varied, all point back to a foundational issue: Canada is not building enough affordable homes fast enough.

To restore affordability and meet projected demand, Canada needs upwards of 480,000 new units a year between now and 2035.3 Over the past quarter century, the country hasn’t come close to that number of housing starts in a single year, let alone at the sustained pace required. A fragmented regulatory environment, stagnant productivity growth, and labour challenges in the construction sector compound the problem. What’s needed, and fast, are new approaches to increase supply, reduce costs, improve delivery times and decrease emissions.

Against this backdrop, Modern Methods of Construction (MMC) has emerged. MMC, proponents claim, offer several advantages over traditional “stick-frame,” on-site building methods. Factory production can compress overall project timelines by 20-50%4, which not only accelerates housing delivery but lowers financing costs. Controlled conditions allow home builders to deliver a higher quality product with better thermal efficiency and airtightness, which is increasingly valuable as energy prices rise and climate competitiveness intensifies. Off-site work also requires fewer workers and eliminates the scheduling complexity of coordinating skilled trades on-site.

While a growing ecosystem of manufacturers and developers are experimenting with various prefabrication techniques, MMC accounts for as little as 2% of housing starts in Canada.5 That’s largely because factory efficiencies are often offset by transportation costs, overheads, and premiums from lower production volumes. At Canada’s current scale, MMC is not always cheaper than conventional construction on a straightforward unit-cost comparison basis.6 Savings of 20- 40% are possible7 but only with volume and standardization, which is precisely why scale is

so central to MMC’s value proposition.

So, what’s holding MMC back from becoming a cornerstone in Canada’s housing strategy?

What are Modern Methods of Construction?

Developed by the University of New Brunswick’s Off-site Construction Research Centre, MMC revolves around seven distinct categories spanning off-site construction, on-site innovation and emerging technologies.

Category 1: Volumetric (3D) modular construction involves fully enclosed units fabricated in controlled factory environments and assembled on-site.

Category 2: Panelized (2D) structural systems utilize flat structural elements like walls, floors and roofs that are prefabricated and then delivered for assembly.

Category 3: Prefabricated components support portions of the primary structure without constituting a complete system, such as foundation elements and staircases.

Category 4: Non-structural assemblies and sub-assemblies, including prefabricated building service components like bathroom pods, façade assemblies and mechanical and electrical systems that simplify on-site installation.

Category 5: Additive manufacturing represents the emerging field of 3D printing for construction to enable layer-by-layer fabrication either on-site or remotely.

Category 6: Building product-led site productivity improvements, including developing materials in larger formats or with simplified connections to accelerate installation.

Category 7: Building process-led site productivity improvements, leveraging digital tools, automation, robotics and lean management practices to optimize on-site efficiency and workflow.

Costs, timelines, regulatory treatment, financing and workforce requirements vary considerably across these different categories. Volumetric modular construction, for example, offers the most dramatic time savings (units can be stacked in days once the factory work is complete), but requires the largest upfront capital investment and faces the most financing and regulatory hurdles. Panelized systems are more familiar to regulators and financiers, but offer more modest efficiency gains. This framework is valuable as it allows regulators, financiers, and developers to navigate these trade-offs—moving beyond treating modular construction as an outlier to managing it as a coherent set of delivery methods.

MMC’s challenges in Canada

Canada’s construction sector faces a fundamental productivity problem that predates today’s affordability crisis. Between 2001-2023, labour productivity in the construction sector declined 37.3%.8 The sector is highly fragmented, with many small firms lacking the scale to invest in technology or training. Work is seasonal and project-based, making it difficult to develop durable workforce pipelines. And the traditional model of site-based, trade-coordinated construction is inherently resistant to the standardization and optimization that drives productivity.

Canada’s skilled trades shortage compounds these problems. This drives up labour costs and, in some markets, prevents projects from moving ahead. The business model is also materially different. Unlike conventional builders who typically operate on a project basis with variable costs, MMC manufacturers require substantial upfront capital investment in factory facilities and equipment. Factories then need consistent, high-volume orders to achieve economies of scale. Furthermore, traditional construction financing is not well-suited to the MMC model, as lenders typically release funds based on on-site construction milestones rather than factory production phases.

Regulations present another obstacle. Canada’s building codes, while harmonized at a base level through the National Building Code, are administered provincially and adopted municipally. A manufacturer, specializing in MMC, that wants to sell into multiple provinces faces a patchwork of code requirements, inspection regimes and approval processes, which can increase delivery complexity and costs. This fragmentation and regulatory friction are among the most frequently cited barriers by MMC practitioners in Canada.9

The country’s vast geography means that the economics of factory-to-site transportation are more demanding than in markets like Japan or the Netherlands. A local factory can serve the Greater Toronto Area or metropolitan Vancouver area well, but the costs of delivering housing more than a few hours away can erode the economic case for off-site production. Strategic factory placement represents a critical lever for unlocking MMC’s potential. This is particularly critical in remote and underserved regions, including northern Canada and Indigenous communities, where persistent supply chain gaps constrain development.

Canada’s climate adds an additional complication. Extreme cold affects the performance of certain building materials and systems, as well as the logistics of construction. While prefabricated and modular approaches are a great opportunity to build housing more quickly in harsh climates and remote regions, designing for standardization requires manufacturers to develop multiple climate-specific standards (reducing economies of scale) or focus on regional markets (limiting national scalability).

All the factors above continue to slow broader uptake. Many builders already incorporate forms of prefabrication, such as manufactured wall panels or trusses, but full modular construction is a relatively small share of overall housing built. Today, modular construction accounts for an estimated 7.5% of the overall Canadian construction market, representing $5.1 billion in annual value.10 If MMC were to capture even 10-15% of Canada’s annual housing need (about 43,000 to 72,000 units per year), it would need dozens of new factories at current production capacities.11 Simply put, large investments and coordinated action is required for MMC to materially change housing delivery output.

MMC in practice

Caivan

Ottawa-based Caivan, one of Canada’s largest developers, uses off-site manufacturing facilities to build four to seven houses daily, with plans to increase production to up to 5,000 a year. It’s also working in partnership with federal and territorial governments, and Inuit organizations, to build 750 modular homes in Nunavut, modified to accommodate specific needs in the north.

Habitat for Humanity Greater Toronto Area

Habitat for Humanity GTA is using modular technology in the construction of its new building in the east end of Toronto. Emerging from the $1.2 billion New Deal partnership between Ontario and the City of Toronto to increase the supply of below market, attainable modular homes, 33 affordable units will be available when the project completes in 2027, with most units large enough to accommodate families.

Bonville Industries

A fourth-generation family business, Bonville has been manufacturing prefabricated housing components for decades, mostly for the Québec and Ontario markets. It has developed over 45,000 homes to date, producing everything from large custom homes to multi-unit affordable housing projects, including the ‘missing middle’ buildings between 4-12 units.

How to scale MMC

1. Recalibrate policy and regulatory frameworks to capture substantial opportunities

All levels of government in Canada are responsible for getting housing built, making policy central to wider MMC adoption.

Building code harmonization is perhaps the most important policy lever and one that MMC manufacturers, industry associations and sector researchers have cited as a significant barrier.12 13 A manufacturer today must navigate different code interpretations, inspection requirements and warranty regimes across jurisdictions, creating real costs that are potentially prohibitive for smaller firms. In the U.S., a uniform national building code for manufactured homes (the “HUD” Code) is in place, and Australia is planning to implement a National Voluntary Certification Scheme for MMC manufacturers that will make meeting code requirements more straightforward. In the 2026 Spring Economic Update, the federal government committed to updating the National Model Codes to better support factory-built housing, including by accelerating the review and approval processes of innovative and prefabricated construction products and expanding the codes to

support more flexible building options (such as engineered wood).14 But this requires coordination and consensus across levels of government and industry stakeholders, alongside rigorous technical reviews.

Municipal permitting and approvals processes can present another critical bottleneck for MMC adoption, reflecting a tension between legitimate regulatory oversight and the need for systems that can accommodate industrialized construction timelines. Current frameworks were designed around traditional stick-built construction and require manual review of projects as a unique design, even when modular units are repetitive and factory-certified. For MMC to achieve its potential, municipal processes need to be fundamentally expedited to reduce approval times, including through mechanisms like pre-approved typologies, use of digital platforms and streamlined review tracks for certified manufacturers. The federal government has indicated that it intends to work with provinces and territories to reduce regulatory friction and provide clearer and more predictable pathways for factory-built housing, but this will take time to materialize. Without such modernization—supported by both regulatory reform and capacity-building for planning departments—the apparatus designed to protect public interests paradoxically undermines Canada’s ability to create housing supply at the speed and scale needed.

Public procurement is a powerful and under-utilized tool. Governments at all levels support the development of both market and non-market housing. When procurement requires or incentivizes MMC techniques, it creates the demand that manufacturers need to justify factory investments.

Build Canada Homes, the federal housing agency launched in September 2025, is mandated to galvanize the implementation of MMC and accelerate the delivery of affordable housing. Canada Mortgage and Housing Corporation (CMHC) is also starting to promote greater use of MMC by incorporating provisions for MMC into their programming. Other government homebuilding initiatives offer noteworthy opportunities, including increasing the supply of housing in the north and on military bases.

The variation in provincial and municipal building codes matters. Federal collaboration across levels of government to align policy and regulatory levers—not just in building codes, but with procurement, planning rules, and approval processes—can meaningfully reduce the fragmentation that limits developers’ and manufacturers’ ability to successfully deploy MMC.

2. Solve scale, standardization and skills challenges

Policy sets the framework, but market conditions determine whether private actors have the ability and motivation to operate within it.

Typically, MMC manufacturers work with developers to bring these technologies into the homebuilding process. Appetite for using MMC in projects is growing and those most likely to embrace off-site construction—large market housing developers, non-profit housing providers with extensive pipelines and institutional landlords creating purpose-built rentals—are building in volume. Other players remain less convinced due to the higher upfront costs, uncertainty about demand and delivery, and the complexity of managing an unfamiliar supply chain. Consumer interest, on the other hand, may be less of a barrier than is sometimes assumed, though there is little data on Canadian preferences and perceptions. Survey data from other jurisdictions suggests that consumers (especially renters) have few objections to factory-built homes when they are well-designed.15 16

Supply faces more structural constraints. Factory capacity is currently limited and geographically uneven. Small-scale developers can face higher barriers to adopting MMC, such as absorbing up-front costs and managing complex procurement. The economics of factory operation are also challenging; a modular facility needs to produce between 500 and 1,000 units a year to make modular construction cost competitive.17

Standardization is the key to unlocking efficiencies. When building types, dimensional systems and connection details are standardized, manufacturers can invest in tooling and processes that dramatically reduce unit costs. But it requires coordination across developers, manufacturers, designers and regulators that is difficult to find in a fragmented industry. Countries that have adopted MMC have done so either with strong public developer mandates (Sweden) or through large vertically integrated manufacturers that have sufficient market power to drive standardization (Japan). Canada has neither. Creating anchor demand through public procurement, and facilitating industry integration across the value chain, are the two most direct ways to create market conditions that could generate a tipping point.

Workforce development also tends to be overlooked, though the tide may be about to turn with the federal government’s recent $6 billion investment in skilled trades. The shift to factory-based production requires a different labour profile, with more emphasis on manufacturing process skills, digital design literacy, and quality systems management. Canada’s existing apprenticeship and trades training is not well-aligned to these requirements, but construction workers typically have many of the core skills needed for modular factory work, making re-skilling possible. A workforce strategy for industrialized building—incorporating provincial colleges, sector councils and manufacturers—will be central in building human capital.

3. Adapt financing mechanisms to boost investing environment

Even with supportive policy and favourable market conditions, financing remains a decisive barrier. The financing of off-site construction does not fit traditional financing frameworks developed over decades, as financing needs to be provided for materials and work outside of standard security frameworks.

Conventional construction financing is built around the draw structure, where lenders advance funds progressively as on-site milestones are achieved and the partially completed building acts as security, via land title. For volumetric modular construction, the largest costs are incurred in the factory, often before a single module arrives on site. At the point of maximum factory expenditure, there is little on the ground to serve as security, leaving developers to typically finance the production phase from equity or working capital. This front-loading of equity requirements increases the effective cost of capital for MMC projects, partially or fully offsetting efficiency gains. Particularly for smaller developers or non-profit providers, it can be a difficult barrier to overcome.

Financing Comparison: Traditional Construction and MMC

| Traditional Construction | MMC (Modular/Prefab) | |

|---|---|---|

| Risk assessment | Established risk models | Unclear/less established risk |

| Valuation approach | Comparable sales and valuation data readily available Appraisers understand consistent methods | Few comparable sales Inconsistent appraisal methodology |

| Draw schedule | Stage-based inspections Foundation -> Framing -> Finish | Upfront factory payments Not aligned with traditional stages or lender security |

| Insurance and warranties | Standard insurance and warranty products with risks well-understood | Coverage gaps during transport Limited warranty options Lack of data regarding claims |

CMHC has begun to adapt programs for modular construction, and, as federal policies and frameworks evolve, there is opportunity to go further. Build Canada Homes could also play a complementary catalytic role by effectively de-risking the model. Both agencies could also address the capital gap that prevents manufacturers from expanding at scale, potentially working with other public or private partners.

For MMC to reach scale, Canada’s banks and private lenders need to be active participants. At present, a lack of familiarity with large-scale MMC projects can make them difficult to assess from a risk perspective. A recent U.K. government inquiry on MMC reported that real barriers exist in the form of risk aversion on the part of warranty providers, insurance companies and banks,18 which speaks to lenders, even experienced ones, being constrained in their ability to assess and approve each building system, material type, component and construction method.19

The most immediate impactful change would be a re-thinking of the construction draw schedule. Banks could adapt protocols that allow advances against verified factory production milestones, which is how MMC loans are secured in Australia and the UK.

Security valuation could be considered along with lending schedule changes. Modules in a factory are considered personal property, not yet attached to real estate, and their value in a default scenario is uncertain. Lenders could overcome this by creating security frameworks tied to factory-built components; industries like shipping and aircraft manufacturing involve lending against high-value assets in production and similar approaches could translate to modular construction.

Beyond loan mechanics, banks can invest in improving institutional knowledge. Effective lenders elsewhere have created specialist teams with expertise in MMC, relationships with manufacturers and insurers, and tailored risk frameworks. Lenders with specialist capacity have an edge in a market that could grow substantially—some estimates indicate that modular construction in Canada is expected to reach $6.4 billion by 2029 (compared to $5.1 billion in 2024).20

Banks can also play a constructive role in shaping the standards infrastructure. In markets where MMC has achieved greater scale, third-party certification and inspection frameworks have been critical in giving lenders the assurance needed to advance funds against factory production. The U.K.’s Buildoffsite Property Assurance Scheme (BOPAS), developed jointly by industry participants and the Royal Institution of Chartered Surveyors, offers an interesting model that has been broadly adopted by U.K. mortgage lenders. Canadian banks could work with industry bodies to help define these standards.

Finally, financial institutions could make financing for MMC-based homes more accessible for buyers, ideally treating factory-built homes that meet all standards like site-built homes for mortgage qualification and insurance purposes. This is not currently the case among most lenders in Canada. Uncertainty in the end-buyer mortgage market suppresses developer appetite for MMC, even when construction financing is available.

MMC is not a suite of products that can be dropped into the existing homebuilding system. It represents a fundamentally different approach to production, one that requires a correspondingly different system of policy, market and financing support. The existing system has been shaped by decades of site-based construction norms and transforming it requires simultaneous and coordinated action across multiple fronts.

The preceding sections are not an exhaustive checklist—first streamline regulations, then grow the market and fix the financing. Progress on one dimension, without simultaneous progress on others, is likely to produce limited results or stall altogether.

Consider the financing gap. Even if financial institutions and governments fully reformed their draw-schedule frameworks tomorrow, developers would still face a thin and immature supply chain, manufacturers would still be operating below efficient scale and regulatory environments would continue to vary significantly across jurisdictions. Financing reform, in isolation, would help at the margins but would not produce a step change in MMC adoption.

Or consider a scenario in which procurement policy is transformed, with federal and provincial housing programs committing to MMC for a large share of their social housing pipelines. This could create greater demand volume, but if building codes remain inconsistent across provinces, if financing products are not widely available and if the skilled workforce for factory production does not exist, the procurement commitment will not translate into the affordable housing units that are needed.

Aligning all the levers

MMC has failed to achieve scale in countries that opted for incremental adoption. While individual projects can succeed, and manufacturers can grow to a point, this approach does not create the system shift necessary for MMC to go beyond a niche offering. Achieving systemic change requires a different kind of ambition, with policymakers willing to coordinate the suite of available levers—building code harmonization, accelerating approvals, procurement mandates, public financing support, industrial policy for factory investment—over a sustained period. It calls for private sector actors making long-term commitments to business models organized around MMC, which requires the policy and financing stability that gives those commitments a reasonable chance of success. And it requires institutions to work together to manage a complex transition.

High-priority actions should come first. National Building Code harmonization—specifically the provisions governing off-site construction—is a foundational step for unlocking action. Encouraging CMHC and Build Canada Homes frameworks to fully accommodate MMC is similarly important, given their central role in housing finance and insurance. Creating anchor demand commitments through government housing initiatives could provide the market signal that manufacturers need to invest seriously in Canadian factory capacity. This could incentivize more direct capital investment and involvement from developers and financial institutions. All the while, municipalities can seek to expedite approval and permit processes to better align with factory production timelines.

These actions would not, by themselves, produce the desired scale of MMC adoption, but they would create a solid foundation on which to build with expanded government support, market capacity, and maturing financing tools specifically geared towards the unique nature of off-site housing development.

Canada’s housing crisis is severe and MMC is an important component of a broader housing strategy. It has international precedents, demonstrated performance and clear potential to address the speed, cost, quality and labour challenges that are holding back housing delivery. The path and the technologies exist. The economic case, when properly structured, is sound. What’s missing is the coordinated, sustained commitment across government, industry and the financial sector to create the environment for MMC to flourish.

Lessons from around the world

These examples show that MMC can scale when the policy, market and financing conditions are aligned. No country has achieved this purely through the intrinsic merits of the technology alone.

Sweden offers perhaps the most instructive international example for Canadians. Swedish homebuilders produce about 45% of new housing using some form of off-site manufacturing, achieved after decades of market evolution, consistent and supportive building codes, and a cultural acceptance of standardized design.

Japan’s industrialized housing sector, led by major manufacturers like Sekisui House and Daiwa House, demonstrates how vertically integrated companies can use

MMC to quickly build high-quality, disaster-resilient housing.

The United Kingdom—through its Homes England agency, MMC definition framework and a series of policy initiatives—has made serious efforts to catalyze MMC adoption, with mixed results, but valuable lessons. The 2019 Farmer Review, for example, concluded that the U.K. construction sector must “modernize or die”.

Australia, which faces many similar housing challenges to Canada, has seen a cluster of MMC manufacturers emerge, supported by proactive state-level procurement policies. The current administration has led a targeted investment of $54 million in advanced manufacturing of prefabricated and modular home construction.

Download the report

Stephanie Shewchuk, Housing Policy Lead, RBC Thought Leadership

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. The reader is solely liable for any use of the information contained in this document and Royal Bank of Canada (“RBC”) nor any of its affiliates nor any of their respective directors, officers, employees or agents shall be held responsible for any direct or indirect damages arising from the use of this document by the reader. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.

This document may contain forward-looking statements within the meaning of certain securities laws, which are subject to RBC’s caution regarding forward-looking statements. ESG (including climate) metrics, data and other information contained on this website are or may be based on assumptions, estimates and judgements. For cautionary statements relating to the information on this website, refer to the “Caution regarding forward-looking statements” and the “Important notice regarding this document” sections in our latest climate report or sustainability report, available at: https://www.rbc.com/our-impact/sustainability-reporting/index.html. Except as required by law, none of RBC nor any of its affiliates undertake to update any information in this document.