Key Takeaways

Roughly $1 in $10 in Canada’s mining sector has been directed towards pure-play critical mineral development over the past 25 years. The majority of the $700+ billion raised in Canadian mining equity and M&A has poured into other metals, with gold and precious metals accounting for 70% alone. In contrast, Australia directed twice that amount over the same period.

Critical minerals are finally attracting a bigger share of mining investment. Around 67 critical minerals projects—representing about half of all active mining proposals—are currently planned, proposed, or under construction, with a potential investment of $72.4 billion by 2034, according to the Major Projects Inventory.

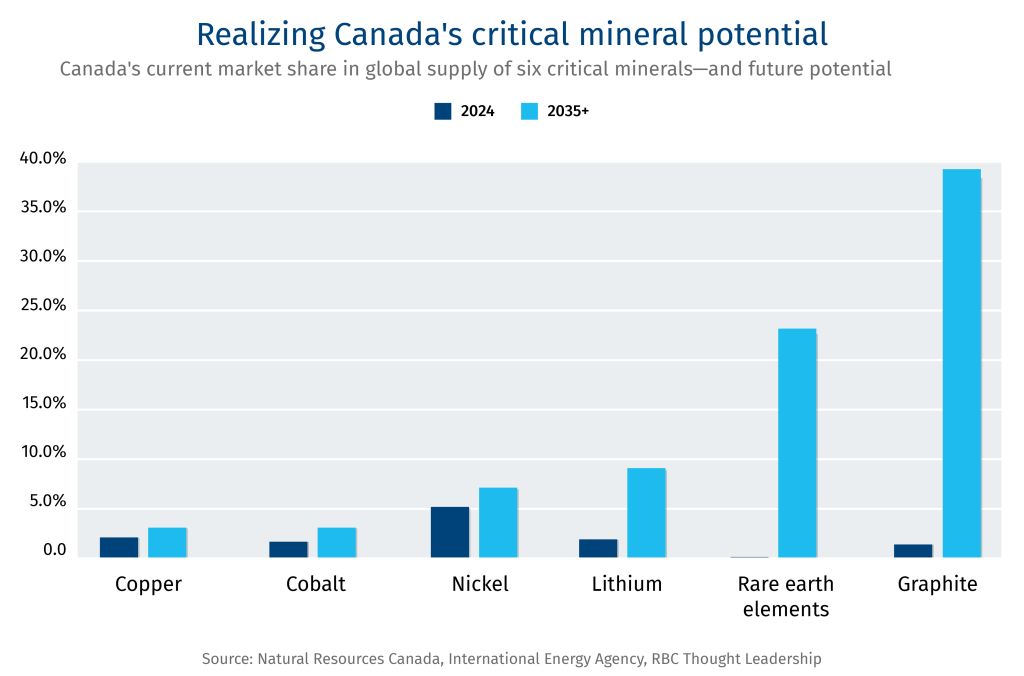

Canada could account for 14% of the global supply across the six key critical minerals by 2040. Current Canadian production of six core critical minerals, cobalt, nickel, lithium, copper, graphite and rare earth, is on average 2% of global supply. It could rise to 14%, on average, at full capacity if identified projects come on stream, the Canadian government estimates.

However, Canada lacks a strong base of well-capitalized domestic players. Only 19% of Canada’s publicly listed S&P/TSX Composite mining firms are diversified miners, compared to two-thirds of Australia’s S&P/ASX 300 mining index. To reach its goals, Canada will likely need to continue relying on international mining companies and foreign investors.

Two decades of capital allocation decisions have stunted critical minerals’ growth. Canada remains largely a “mine-and-ship” jurisdiction when it comes to critical minerals—with much of the value add and refining picked up by China and other players who have captured the refining segment, and further developed ancillary supply chains, such as electric vehicle, electronics and defence industries.

Despite trade tensions, there are still signs of U.S.-Canada capital alignment. Under President Donald Trump, the U.S. has invested an estimated US$135 million in direct equity stakes in Vancouver-based companies Trilogy Metals and Lithium Americas Corp., in addition to a US$2.3 billion bridge loan for Lithium Americas. It will be unlikely the U.S. can (or wishes to) completely phase out Canada from North America’s critical mineral ecosystem.

Canada faces a critical minerals capital crunch. The absence of patient, risk capital severely impedes the country’s ability to support both Canada and other Western nations in their efforts to move their critical mineral supply chains away from China.

That capital is needed for Canada to take advantage of the critical minerals industry that’s projected to grow between two to three times globally with a capital requirement of US$500-600 billion by 2040, according to an International Energy Agency forecast. Global demand for six core commodities—cobalt, copper, graphite, lithium, nickel and rare earth elements—will be driven by several growth sectors, including electric vehicles, clean energy infrastructure and space. As well as strategic sectors such as defence, manufacturing and electronics.

Canada holds world-class geology across all six metals but remains a relatively marginal player, accounting for roughly 2% of the global supply of the six metals. If identified projects proceed at full capacity, it could climb to 14% of total supply over the next 15 years, on average, according to Canadian government estimates. The development of vertical supply chains such as an expanded advanced manufacturing base, could have an exponential impact on Canadian supply to meet domestic and international demand.

Yet, Canada remains largely a “mine-and-ship” jurisdiction. Raw metals are shipped mostly to China where they are refined and transformed into high-value components. It’s the result of two decades of capital allocation decisions and the lack of a robust national strategy, but also China’s ability to depress metal prices to crush competitors.

There’s considerable global momentum to propel the Canadian critical minerals industry forward. The U.S. is leveraging its funding, market mechanisms and guarantees to build out a critical minerals market that excludes China. Meanwhile, Europe and several G20 allies are eager to diversify their critical minerals supply chain as they fear the Chinese industrial machine will crush their domestic economies and leave them ever more beholden to Beijing.

China’s recent export controls on key minerals—including rare earths, graphite, gallium, germanium—over the past year are a clarion call for Western countries to act.

Among its G7 allies, Canada is best equipped to take advantage: it’s home to high-grade lithium belts and graphite deposits in Quebec and Ontario, globally significant nickel resources in Manitoba, formidable copper reserves in British Columbia, and rare earth elements in pockets across Canada, including Newfoundland and Labrador. Few countries can claim this breadth across all six critical minerals at scale.

We have identified five structural pressure points that explain why Canada’s critical minerals sector remains undercapitalized, and why market forces alone will not correct the imbalance. Closing the gap requires a coordinated public-private agenda anchored in sovereign co-investment, infrastructure financing, miner-driven shared processing corridors and integration into Western supply chains.

Structural Pressure Points

1. The loss of national champions

Between 2005 and 2012, more than $119 billion in Canadian base metals and steel assets transferred to foreign ownership.

The transactions were part of a wider globalization trend: foreign capital was expected to unlock value faster than our limited domestic capital markets, and nationality of ownership mattered less than the resulting economic uplift from mineral production and job creation. What that consensus underestimated was the long-term cost of losing domestic companies capable of anchoring new project developments—for a future era.

As Canada’s domestic giants were subsumed into global majors, the domestic capital-raising ecosystem was also disrupted. Boutique mining dealers shrank from around 60% of deal flow in 2010 to effectively 20% today, according to S&P Capital IQ. A similar trend is seen across capital holders as well, with resource-specialist funds now making up only 1-2% of domestic equity mutual fund assets under management today, compared to 6-8% in the early years following the global financial crisis, according to ISS MI MarketSage.

Many of the national champions that could have spearheaded Canada’s lithium, graphite and rare-earth projects largely no longer exist. Meanwhile, global majors allocate capital across their global portfolios that may not align with Canada’s strategic, sovereign objectives. This dynamic stands in marked contrast to the oilsands, which is the predominant operating asset controlled by large domestic players with large domestic ownership.

2. Capital consolidation around gold took the shine off other metals

Of the $700 billion raised in Canada in mining equity and mergers and acquisitions over the past 25 years, only 11% of capital was channelled to pure-play critical minerals development, according to S&P Capital IQ and LSEG. In contrast, Australia directed over twice as much capital to critical minerals during the same period. This was partly due to geology (Australia’s copper deposits are larger and less associated with gold), and partly to a closer proximity to Chinese and East Asian smelters.

The higher gold concentration in Canada reflects a historical M&A wave, with the S&P/TSX Composite mining complex becoming increasingly dominated by a smaller pool of large gold producers. In essence, Canada’s public mining equities evolved into a precious metals financing platform—a result of structural choices made over two decades across Canada’s critical minerals companies.

It doesn’t have to be a zero-sum game between gold and critical minerals—there is room to grow both mining sectors and even create ecosystems that feed off each other.

However, in Canada excellence in gold did not necessarily extend to critical minerals for two reasons:

-

The composition of Canada’s gold endowment made it efficient at producing the yellow metal, but relatively less so for other associated minerals like copper, nickel, cobalt as by-products. Australia’s mix of iron oxide-copper-gold deposits provide a more diverse commodity portfolio.

-

Gold mining skills and infrastructure do not inherently transfer to critical minerals. Gold smelting and refining are mature and standardized, whereas critical minerals processing, which is oriented towards specific end-uses (especially on battery metals) that require complex hydrometallurgy and chemical conversion..

3. Junior miners continue to face a financing cliff

Canada’s flow-through share financings—a tax incentive that allows investors to deduct 100% of their investment against their taxable income—works exceptionally well for early-stage exploration. It aggregates retail capital, reduces the effective cost of capital, and has successfully supported mineral exploration.

However, once a company completes the first assessment hurdle, these tax incentives expire (until construction begins). What follows is a $20-30 million financing gap: feasibility studies, engineering, permitting, and technical validation are required for ultimate final investment decision. These costs are often too large for high net-worth investors and too risky for institutional investors and lenders. Delays in permitting compound this challenge, as the companies remain pre-revenue with a stretched balance sheet.

For niche commodities such as graphite, rare earths and lithium, the problem is worsened by lack of market diversity. China often remains the sole buyer of mineral concentrates. Chinese lithium converters buy spodumene ore and process it into battery-grade lithium, while rare earth concentrates must be converted into a Mixed Rate Earth Carbonate—a processing step Canada largely lacks.

Few institutional investors have historically backed a Canadian junior whose only offtake market is a Chinese refiner, leading to a structural financing gap that has stalled viable projects for years.

4. Refining and processing face a structural deficit

Over the past three decades, Western countries effectively outsourced lower-margin, energy-intensive refining to China. Backed by state-backed capital, lax environmental regulations and lower labor costs, China now controls 70% of global refining market share for 19 of the world’s 20 most critical minerals.

China also builds overcapacity to squeeze competitors. Global copper smelting utilization was only 70% last year, and has played a role in Canada closing the Flin Flon, Gaspe and Kidd Creek copper smelters over the years. Today, only one Canadian copper smelter/refinery remains active: Glencore’s Horne smelter in in Rouyn-Noranda, Que., and its associated Canadian Copper Refinery.

Competing head-to-head in pure-play downstream processing against subsidized overcapacity is economically difficult. However, Canada’s advantage lies in pairing upstream mineral exposure—where margins are structurally higher—with selective downstream integration in “mineral corridors” that offer durable cost advantages, such as low-cost, zero-emitting hydro power in Quebec.

5. Limited domestic demand has constrained value chain growth

Refining investment follows demand—a capital-intensive smelter is hard to build in Canada where local demand is limited. Battery cell manufacturing is nascent and defence procurement operates at a fraction of U.S. scale. Magnet manufacturing, rare earth processing, and cathode precursor production are largely absent. The result is that shipping concentrates are shipped to where the customers are: primarily China.

The paradox is that Canada committed up to $55 billion to attract electric vehicle and battery manufacturers over the next 15 years without attaching domestic sourcing conditions that peer jurisdictions demanded. Germany and France implemented strict, minimum E.U. content and local supply-chain requirements into their electric vehicle subsidy schemes. South Korea similarly tied support to the use of Korean-source battery materials and components. The absence of such commitments in Canada, means the subsidies have not yet catalyzed ancillary industries.

How to Close the Capital Gap

1. Scale sovereign capital across the full value chain

Ottawa’s $2-billion Critical Minerals Sovereign Wealth Fund requires more heft to match the significant capital requirements. The Korea Zinc joint venture, for example, is developing a refinery in Tennessee for US$7.4 billion alone, demonstrating the substantial capital-intensity of downstream investments. A full build-out of mining, refining and processing critical minerals require an order of magnitude of patient capital that’s willing to persevere over years of construction and commercial validation.

The Canada Growth Fund (CGF) has made three mineral investments to address the gap. Its recent co-investment in Thompson Nickel Mines in Manitoba alongside U.S.-based Orion Resource Partners LP and Brazil’s Vale SA anchored the project, attracting credible corporate capital, and signalling strong sovereign commitment. This follows investments by the CGF in Quebec’s Nouveau Monde Graphite facility and the Foran Mining Corp. copper-zinc project in Saskatchewan.

Internationally, the Brazilian Development Bank also offers a template: a US$1-billion blended fund structured with government and private capital (including national mining champion Vale), managed at arm’s length and deployed across extraction, refining and processing. The structure, backed by government funding, instills commercial discipline, and makes strategic projects financeable.

2. Deploy infrastructure capital to unlock regions

Co-investing in enabling infrastructure—such as roads, transmission, grid connections to remote mining regions—reduces a project’s required break-even price by around 22-24%, the single largest lever of any individual policy measure, according to a recent Canada Infrastructure Bank (CIB) analysis.

The build-out of accompanying infrastructure is ideal for pension funds and long-duration institutional investors who are best suited to participate: lower risk than equity in a junior miner, contractual cash flows, and infrastructure-style returns. Ontario’s metal-rich Ring of Fire region alone requires as much as $2.4 billion in road and transmission investment before a single mine becomes commercially viable. For pension funds, it’s an opportunity to finance infrastructure, provided there’s surety of the facility being built, and the new infrastructure can be put to multiple uses and even serve as a springboard for new developments.

Investment in remote communities, many of which are on First Nations territories, presents another opportunity. However, unlike Alberta and British Columbia where oil and gas commercial precedents are well-established between First Nations communities and corporations, these mining jurisdictions require nurturing local governance and technical readiness to ensure long-term commercial success.

3. Build mineral corridors around Canada’s best clusters

Shared processing infrastructure solves multiple problems simultaneously. For instance, Quebec’s six high-grade, high-tonnage lithium projects can complement a regional refining hub. A similar logic applies to the lithium belt running from Thunder Bay to Winnipeg, and to the Sudbury nickel cluster, which already boasts world-class refining infrastructure that could expand to serve new critical minerals projects across Northern Ontario.

Such centralized refiners would give junior and mid-sized miners credible non-Chinese buyers, reinforcing their business and investment case. Corridor economics could also have a cascading economic effect, extending to logistic, transport, commercial and residential housing, and other amenities.

A shared Central Lithium Refinery—potentially structured with government loan guarantees and anchor offtake agreements with battery producers in Europe, Korea, Japan, and emerging Canadian manufacturers.

This offtake, in turn, makes projects financeable on Canadian equity markets and eventually eligible for project financing. The infrastructure economics improve further if the Plan Nord railway extension in Quebec proceeds—an initiative championed by the Cree Development Corporation that would materially reduce both the environmental footprint and capital costs of the Quebec lithium cluster.

4. Draw in global majors to improve project economics

The Canada Growth Fund is well-positioned to co-invest alongside global majors, provide offtake agreements that de-risk revenues, and leverage investment tax credits (ITC) to improve project economics. CGF’s partnership with Strathcona Resources Ltd., to build a $2-billion carbon capture and sequestration facility is a case in point: the government underwrote half the capital and allowed full ITC value to flow to private investors. Revenue de-risking tools, such as offtake agreements and contracts for difference, could reduce a project’s required break-even by approximately 18-19%, CIB analysis shows. The combination of infrastructure investment, revenue de-risking, and co-equity could move Canadian projects to the top of a global major’s priority list.

5. Forge closer ties with U.S. supply chains—but diversify

Few governments are doing more to reshape the global minerals order than the United States. The U.S. Office of Strategic Capital is authorized to deploy US$100-200 billion to bolster defence and industrial supply chains—roughly 15-20 times Canada’s federal funding. Washington’s Project Vault, a US$12-billion critical minerals stockpile, is already operational and striking deals with other countries.

Developing closer ties with U.S. supply chains is Canada’s greatest structural advantage other jurisdictions would struggle to replicate. Strategic deals under the Project Vault umbrella, would ensure Canadian minerals flow into U.S. rules of origin for batteries and EVs. Guaranteed offtake commitments would also give Canada both the demand signal and the financing certainty that mine-refine-process economics require.

The strategy is not without risk as deeper supply-chain alignment with Washington could mean Canadian minerals face U.S. export licencing and defence procurement priorities that serve American industrial policy first.

To avoid diminishing its resource sovereignty, Canada should pursue a strong diversification strategy targeting European and Asian allies, building on its 26 new investments and partnerships with G7 allies that unlocked $6.4 billion of critical minerals projects.

Five Lessons from the Aussie Playbook

Australia and Canada share comparable geological endowments and mining traditions, but the similarities end there. Australia has consistently outpaced Canada in diversifying its resource wealth, employing a robust strategy focused on mobilizing capital, project permitting, and underwriting infrastructure—ultimately shaping investor behaviour.

Here’s how the Australian and Canadian playbooks have deviated:

1. Anchor investors lead the way

Australia’s pension funds maintain a standing allocation to resources, supported by specialist mining investors who understand the risk profile at every stage of development. Canadian pension funds don’t have the same obligation, while its overall investor base has rotated away from resources over the past 15 years towards tech, healthcare, and global equities. This has left mining capital in Canada episodic, cycle-dependent, and increasingly risk-averse at critical stages of development. The result is a more fragile domestic funding environment for Canadian miners, a trend partly driven by the historically lower total return performance of Canadian miners relative to their Australian peers.

2. Mechanisms to manage financing troughs

While both countries successfully fund early-stage exploration, Canada’s path diverges sharply after that. Flow-through financing—which provides tax incentives at the earliest stages—is effective but limited to exploration. This leaves feasibility, construction, and first production with few funding and incentive levers. This creates a structural incentive to sell assets early rather than build and operate them. Australia’s deeper capital pool through pension funds and specialist resource investors has fostered mid-tier producers that Canada largely lacks.

3. Permitting certainty as a capital advantage

Australia’s approval frameworks include statutory timelines to prevent processes from stalling indefinitely. Canada’s multi-layered federal and provincial reviews, combined with open-ended consultation processes, can stretch five years or more with no defined endpoint. Because permitting risks directly impact project economics, these delays serve as a significant deterrent to capital.

4. The virtuous cycle of base metal wealth—and expertise

Australia’s commodity diversity is anchored in bulk and base metals—iron ore, metallurgical coal, copper, bauxite and alumina—in greater propensity than Canada and its precious metals. That mix supported the growth of BHP Group, Rio Tinto Ltd and Fortescue Ltd., which are now backing other critical minerals including the energy-transition metals like lithium and rare earths. While Canada’s geology is diverse, public markets, historical mergers and acquisitions (M&A) and resulting producer base tilted towards gold companies.

5. Market access and Asian ties facilitated demand

The rise of Asian steel manufacturing, especially China but also Japan and Korea, drove long-term contracts for Australian iron ore and metallurgical coal and anchored the rise of the Australian mining majors. These deep commercial ties now extend to copper, alumina and other emerging battery materials. Canada, by contrast, built commercial ties with North America and Europe, and became cost uncompetitive from a supply standpoint given the lower operating costs of Asian refiners but also missed out on the nexus of demand from Asian battery value chains.

Download the report

Contributors:

Shaz Merwat, Director, Energy Policy, RBC Thought Leadership

Yadullah Hussain, Managing Editor, RBC Thought Leadership

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. The reader is solely liable for any use of the information contained in this document and Royal Bank of Canada (“RBC”) nor any of its affiliates nor any of their respective directors, officers, employees or agents shall be held responsible for any direct or indirect damages arising from the use of this document by the reader. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.

This document may contain forward-looking statements within the meaning of certain securities laws, which are subject to RBC’s caution regarding forward-looking statements. ESG (including climate) metrics, data and other information contained on this website are or may be based on assumptions, estimates and judgements. For cautionary statements relating to the information on this website, refer to the “Caution regarding forward-looking statements” and the “Important notice regarding this document” sections in our latest climate report or sustainability report, available at: https://www.rbc.com/our-impact/sustainability-reporting/index.html. Except as required by law, none of RBC nor any of its affiliates undertake to update any information in this document.